Inflation, the Fed, and the Economy: Is the Soft Landing Dream Dead?

Is the U.S. banking system truly secure, or are there lurking vulnerabilities? 🤔 Let’s expose the potential risks that could compromise capital levels, particularly concerning losses in security portfolios. 🔍💸

We unravel the concept of fire sale vulnerability— a scenario where banks might be compelled to sell underwater bonds at a loss. 😱💰 Don’t be fooled by assurances that these bonds will be held to maturity. The truth is, if a run on the bank occurs, they may be forced to liquidate, putting their financial stability at risk.

Don’t miss out on understanding the intricacies of the current banking landscape. Hit play now and stay ahead of the financial curve! 🚀📈

CHAPTERS:

0:00 Where is Inflation?

4:15 The US Banking Is Vulnerable

9:49 The System Is Out Of Control

10:51 The Economy Is Showing Cracks

13:03 Don’t Trust Stock Rally

14:01 Pattern Shift

15:53 US Money Supply Is Doing Something Odd

17:45 M2 Money Supply

23:25 China Extends Run

SLIDES FROM VIDEO:

TRANSCRIPT FROM VIDEO:

Well, we have some good news. Inflation is only running now at 3.2% over all. Well, is that really great news? Because that just means that prices are going up a little bit slower. And that’s not true with all prices. That’s only true with some prices. And let me remind you of something. Okay. This is a 2013 Venezuelan bolivar.

How many Bolivar? 20. And you could actually convert that into some things. I mean, Venezuela has been in trouble for a while. But you could actually buy something with it. Well, that’s not any money anymore, because the government says, nope, no money. Now, this is a $500 million bolivar. And you still can’t buy anything with it. Do you remember back in the day when you had a silver certificate and then silver certificate, you could convert into this silver dollar?

This was used in one place. This was used all across the globe. how about this gold certificate? What does this say? $10 in gold coin. Payable to the bearer on demand. And then this gold was used everywhere in the world. Not just one little place. We all know that this stuff does not buy you what it once does.

But this is now our largest bill. You know, there used to be $100,000 bill. And out in the public for you and me, there were 10,000, 5000, 1000, $500 bills. So all of this is indicative because what are we going to get soon? $1,000,000,000,000? Like what? Zimbabwe? Yes, Zimbabwe. $10 trillion note. And you can’t buy anything with it.

We are at the end of this cycle and there is and I’m getting chills because when I was putting this together, I saw an extremely key and significant pattern shift that I’m going to show you today. Coming up.

I’m Lynnette Zheng, chief market analyst here at ITM Trading, a full service physical gold and silver dealer. But what we really specialize Look, I have been in these markets on some level since I was ten years old and I’m 69, so 59 years. I’ve lived through a lot. But I’ve studied even more. And as a stockbroker in 87, I started to learn about currencies and I saw these repeatable patterns.

And I realized and you guys all know this, there are pattern’s for everything’s life cycle. I am not at the same point in my life cycle as my eight year old granddaughter, nor would you even think that I was. And she’s not at the same point in her life cycle that I am. And you would never think that she was.

So why would currencies and especially government based currencies. Why would that be true? That that doesn’t change? It does change. They just try and do it slowly enough that you don’t notice it. And that’s their inflation target, is to keep it low enough that you don’t demand more money. And my goodness, what has happened? But inflation was so obvious to everybody that employees started asking for more money.

And the unions have now come to become a lot more prominent. And what they don’t realize yet is that all of these wage increases still don’t keep pace with inflation. Still don’t. But we have to talk about what’s going on. And we got to talk about this pattern shift that I saw. And I mean, I’m blown away by it.

But okey dokey. So the U.S. banking system is still still vulnerable. Yes. Think losses in security portfolios risk weakening capital levels. So there are key pieces inside of this report, firesale vulnerability, meaning the that banks would be forced to sell those underwater bonds. Oops. I usually do it this way. They’re underwater bonds at a loss. That’s a fire sale.

If there is a run on the bank and they’re forced to sell those holdings that they’re telling you that, they’re not going to lose any money on it because they’re going to hold them to maturity. That’s garbage. If they are forced to. And it remains elevated. Yeah, it should remain elevated. Liquidity stress ratio has increased since early 2022, driven by a shift from liquid to less liquid assets.

That means things that are harder to sell. And from stable to unstable funding. Look at what’s happening in the Treasury market. Right. This is true in in all of the banks, including the Federal Reserve Bank. So that means that it’s gone from strong hands that can hold on to it, to weaker hands. And in the banking sector, I just told you last week about their use of.

Broker deposits. Right. And I told you at that time that those can run very quickly from the banks. So the fact that the banks are still vulnerable with liquidity stress. Radia ratio this high. Yeah. Let’s liquid assets, meaning harder to sell assets, which means bigger discounts if they have to sell them.

And from stable funding deposits and other things to unstable funding, those broker deposits which can leave the system very rapidly and run vulnerability index shows an increase since early 2022 due to an increase in leverage. So debt upon debt upon debt inside of the banking system, but also due to increases in unstable funding and illiquid assets. Why do you think the markets are flying today?

Why? Because they see a crisis and they see the Fed having to that and drop those interest rates down. And that means that they get to buy and participate. Lots of free money. We do. Except that didn’t fix the problems before. It only created more, more problems. And it takes us on the verge of a hyperinflationary depression. Make no mistake about it.

I hope I’m wrong. I’m not wrong. I’m not wrong. I know it. It happens every time. And if something’s happened over 4800 times, every single time when we’re doing the same thing, is this time going to be different? No. They need a huge crisis to shift us into the next iteration of money that we work for that they control.

This is money that they don’t control. This is what you need. If you haven’t done it yet, number one, you need to subscribe. And number two, you need to click that cowardly link and get it flippin done, get it done, get it done, get it done. The March 2023 banking crisis highlighted the vulnerability of the banking sector to a sudden rise in interest rates and what happened in March and April of 2020 showed you the fragility of food, water, energy, security, barter, ability, wealth preservation, community and shelter.

So please, people get it done because shockingly, the system is falling apart. And what is the choice of the central bankers, the Fed, the BOA and the BOJ? Hold BOJ I’m sorry, Bank of Japan hold rates steady. So can you see how they’re between a rock and a hard place? They keep raising rates. You’re going to see more unemployment, which is what they want.

What they stated that they wanted from the beginning. It’s not reflation that has taken hold. It’s inflation that has taken hold. But hey, let’s have higher unemployment. Let’s have a recession. Because honestly, you guys, there is only one way to fight inflation, and that is with deflation. And only one way to fight deflation, and that is with inflation.

But when you are at the end, you have no tools to work with. And that’s why I’m talking about a hyperinflationary depression. And you can call me crazy, but I don’t know anybody else that studied this stuff the way I have. There are lots of smart people out there. I’m not saying that there aren’t or that nobody else knows this.

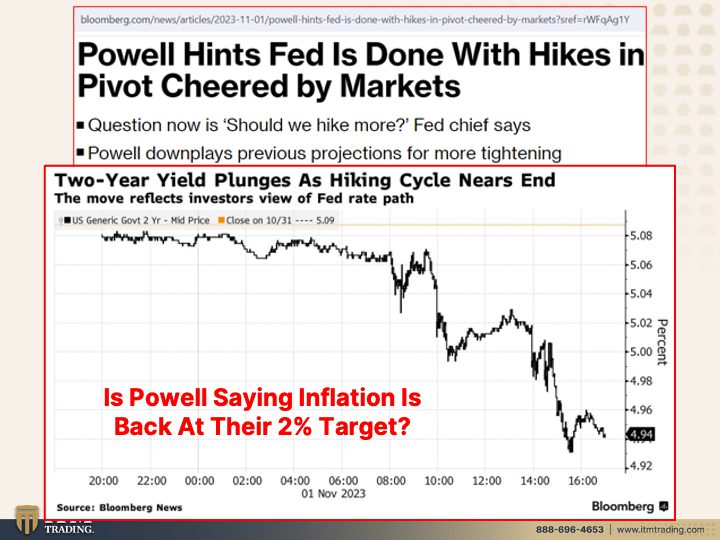

I just haven’t really met them. That’s all I’m saying. And my mother always said, If it’s true, you can say it. Powell hints it is done with hikes and pivot, cheered by markets. Really? The question now is, should we hike more? I mean, it’s a freaking joke. He knows he’s out of control. He knows the whole system is out of control.

And when the markets hear that the two year year plunges as hiking cycle nears an end and Wall Street cheers. What do you do? But are they really saying that they’re headed back to that 2% target? And what does that really mean? That just means that the loss of purchasing power happens more slowly, but it still happens. I mean, let us not forget, 2020, leave our bill to a 500 million bolivar bill and you can’t buy crap with it has more value as an empanada wrapper than it does as money.

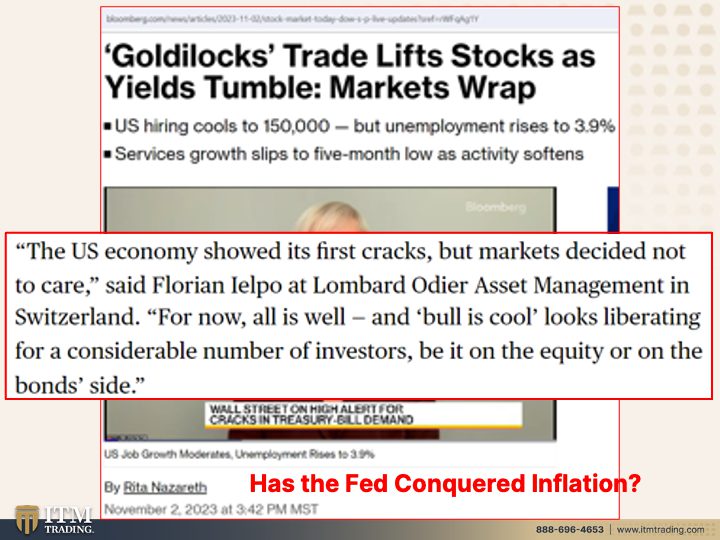

Shocker Goldilocks Trade list stocks as yields tumble market wrap. U.S. hiring cools to 150,000, but unemployment rises to 3.9. The US economy showed its first cracks. Well, that’s because they don’t know how to look because it’s been showing a lot of cracks. La la la la la. For now, all is well and bull oil is cool. Looks liberating for a considerable number of investors.

These are not investors. These are traders. Because everything. Everything. Everything has been turned into a trading market. Wall Street is too big to fail. You and I were just about the right size. So you need to become your own central banker. That is what I’ve done. Have they conquered inflation? No, they have not. Have they positioned for massive deflation?

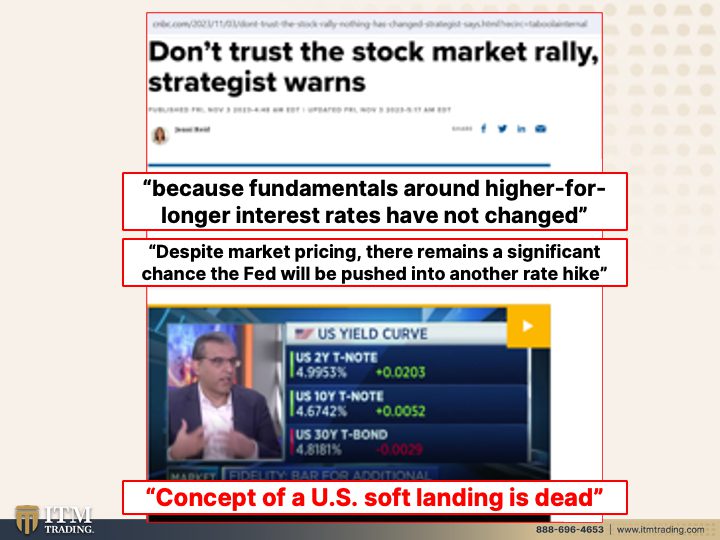

Yes, they have. I’m going to show you that in a few minutes. And some are saying don’t trust the stock market rally. And I would have to absolutely agree, because fundamentals around higher for longer interest rates have not changed. Now, he’s not saying that they won’t keep it higher for longer. But the fundamentals have not changed. We are at the end of this currency’s life cycle.

And in order to shift into the new reset currency, the CBD sees the full surveillance economy and the absolutely controlled individual loss of all of your personal freedoms. All of your rights, not just for you, but for your children and your grandchildren and your great grandchildren. You really want us to go back to feudal times when you just have a handful of people that own everything and everybody else leases?

Because frankly, I love my family. That’s not okay. And by the way, I consider you my family. You are who I work for. Make no mistake about that. And I am pissed off. Despite market pricing, there remains a significant chance the Fed will be pushed into another rate hike. Because if they keep it here, if they lower the rates down, which now the markets are going, what do you do?

By July, we’re going to have lower rates. But that also means that we are in deep doo doo in the economy. And I’m going to tell you, I personally believe that the hyperinflation has already begun. And I’m going to show you why. I’m going to show you why in this major key pattern shift. I’m going to show you why I say that.

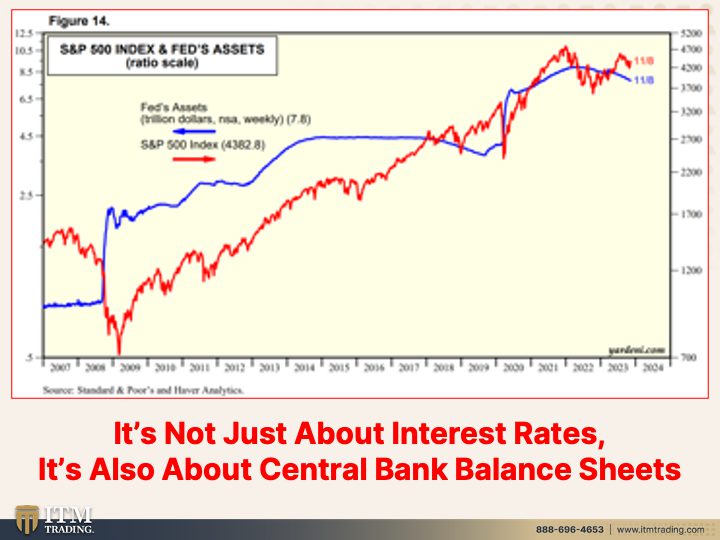

Well, at least he admits the concept of U.S. soft landing is dead. No crap, Sherlock. It’s been dead. There is no such thing as a soft landing. Maybe for some, because they’re properly positioned, but not for most. For most, it is always a very hard landing. So let’s compare the stock market index and the Fed’s assets, which are all the garbage that they bought and put on their balance sheet.

And you can see how coordinated it is up until 2018. And there was a pattern shift there where that blue line, which is the Fed’s balance sheet, went below the red line, which is the S&P 500. Okay, we got that shift again, Right. So can you see that there was a pattern shift here? Look, I can’t tell you timing.

No technician can. I can tell you what is most likely to happen, but I can’t say it’s going to be Tuesday morning at 835. But if it is Tuesday morning at 835, I will be as shocked as everybody else. Maybe not shocked. Maybe surprised is a better word because I’m prepared. So how much that’s going to impact me?

Actually, it’s going to impact me in a positive way. I want it to impact you in a positive way, too. So let’s move on with this. Where’s my mouse? Right here? Because frankly, it’s not just about the interest rates, it’s also about the balance sheets. And so you can see this little bit. Let me grab that. You can see this little bit when they try to run off the balance sheet.

And that kind of screwed everything up. And guess what? They’re trying to run off the balance sheet again and that’s going to screw it. Between a rock and a hard place. There is no way out of the next obvious financial crisis because we’re already in it. And I’m trying to show it to you. And I’m sorry. I’ll try and calm down, but I’m telling you, I don’t like what I’m seeing.

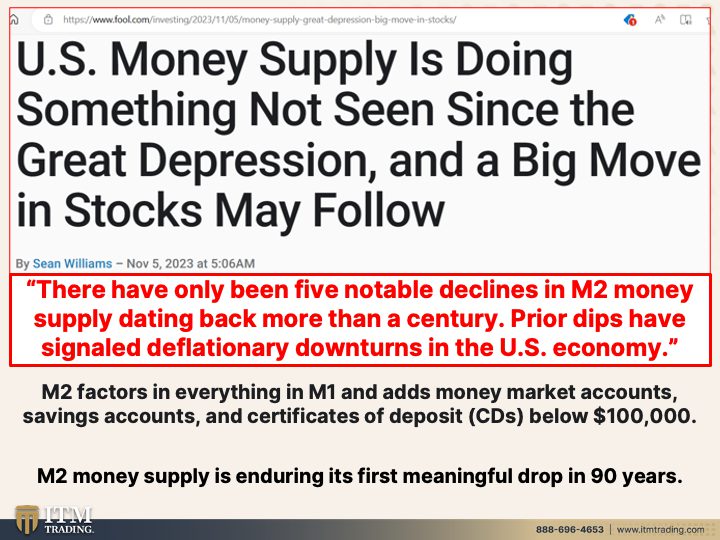

I don’t like it at all. I don’t like it. And here the US money supply is doing something not seen since the Great Depression and a big move in stocks by who cares about the stock market? I mean, honestly, it’s a shell game. You you’ve got just a handful of entities that dominate everything. And I’m going to be talking more about that next week.

But my God, there have only been five five notable declines in the M2 money supply dating back more than a century prior. Dips had signaled deflationary downturns in the US economy. Yes, Think M2 factors in everything in M1. So that’s all of your savings accounts, your checking accounts, your cash, all of that and adds money market accounts, savings accounts and certificates of deposit below $100,000,

M2 Money supply is enduring its first meaningful drop in 90 years. Do you think that it’s a coincidence that you got to go all the way back to the Depression? And what was that? Depression? Frankly, it was a hyperinflationary depression because they reset the dollar against gold and that’s how they do it. They take something that’s all intrinsic value globally accepted, globally used in every sector of the global financial system.

And they take this that’s used in one sector and they do that reevaluation. They did it in 33. They’re going to do it again. I don’t know whether it’ll be 24 or 25, maybe even 26. I don’t think we can go that long. But you need to be in place now. Let me show you what that looks like, because here is the key pattern shift.

Probably the most significant pattern shift that I have shown you to date. And you all know I like to show those pattern shifts. This is the M2 money supply and it is enduring the first meaningful drop in 90 years. 90 years. That’s a pretty meaningful drop. This goes back to 1960. Do you see anything like that? No, you do not.

It’s based on debt. The system since 71 is based purely on debt and even before that it was only quasi because they kept shifting the backing of gold. And how much that backed. Well, let’s let me show you this, because I told you, I’ve been telling you right along that this is when I’m going to tell you when I see this move in a very pervasive way.

That’s what I’m going to tell you, that the hyperinflation has begun, whether you see it or it’s obvious to you or not. Make no mistake about it, it has begun because this is the velocity of M2, too, and it is spiking at the fastest rate ever. It is spiking faster than it did back here in the nineties. Can you see that this is faster?

So what is the velocity of money and why does that matter? The velocity is the number of times that money changes hands. Right? So let’s say I have a good week and I go out to I decide, okay, I can afford that new card that I wanted to buy and I go out and I buy that new car, I’ll take on some debt to do it, but I’m going to put a down payment.

Now, the person at the car dealership makes a commission on that. So my money went from my hands to their hands and they go, now I can take Bobby, you know, or Suzy on that great vacation we’ve been talking about. And they go and they take a vacation and they’re feeling very flush. So they go to fancy restaurants.

They’re big tippers. And now that wait, staff can go, Tony needs a new pair of sneakers. Now I can afford those new pair of sneakers. So you can you see how the velocity of money registers, how quickly money changes hands during inflationary and hyperinflationary events. People get rid of money as quickly as possible. We did have a little blip up right there, but I said at that time it needs to be in a pervasive way.

This is pervasive. This is pervasive. So this is a critical and key pattern shift that’s indicating to all of us that we have entered the for most people, the worst part of this trend cycle. Things are going to get nasty, nasty, nasty, nasty. I said this in 2007 after the dollar fell to its lowest level ever against its trade weighted basket, I said something nasty.

This way comes. I’m telling you right now, something very nasty is on its way. Are you ready for it? This is where community is so critically important because we don’t have the time. I mean, you know, I’ve been buying gold and silver well for a long time, but in earnest since 2002, because I knew that that’s when this transition signal the end.

The technical data told me this is the end of this life cycle. So you made a walk and it’s taken another 22 years. I don’t care how early I am. That gave me time to accumulate it and using the strategy based upon my studies. Since 1987 on currencies and currency life cycles, I was able to get myself with gold and silver first into the right position.

Then in 2008, the system died and I knew the system died. So we went from a little two bedroom condo to I couldn’t go too far out at that point because of my children. But this is a half an acre. That’s all it is. It’s a half an acre. And I have a house and I have a pool on it.

But I converted it into an urban garden and developed my mantra because there was no doubt in my mind of where we were in this cycle and what I needed to do. I would rather be 20 to 4500 years. I don’t care than one second too late

SOURCES:

https://www.yardeni.com/pub/balsheetwk.pdf

https://fred.stlouisfed.org/series/M2REAL