THE RETIREMENT RISK SPECTRUM: (Pt-1) 99% Bond Losses & New Erra of US Bankruptcies… by Lynette Zang

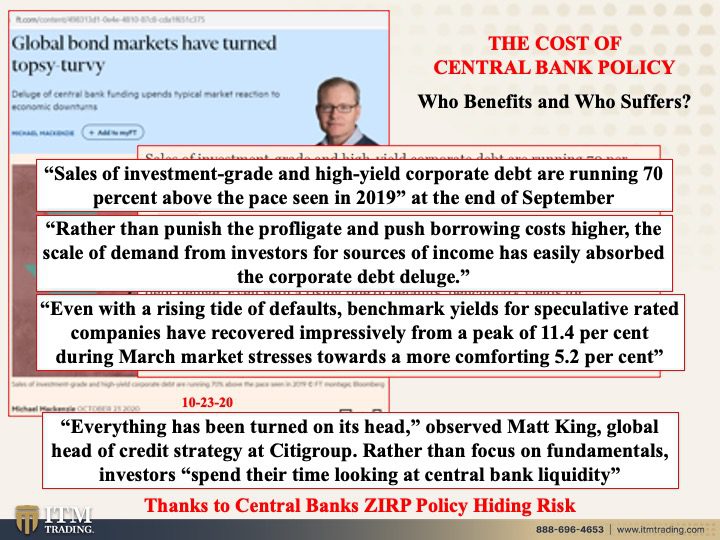

“Global bond markets have turned topsy-turvy†according to a recent article in the Financial Times. The same could be said for the stock markets and the real estate markets as well. In fact, in reaction to the 2008 financial crisis, when the global central bankers announced that they would overtly “manage†the markets, this fact has been true, the real value of all markets has been hidden from investors thanks to the flood of new central bank fiat money. This is something that should be clear to all, but if not, then I hope it is clear to you now because we are clearly running out of time.

Have more questions that need to get answered? Call: 844-495-6042

“Everything has been turned on its head,†observed Matt King, global head of credit strategy at Citigroup. Rather than focus on fundamentals, investors “spend their time looking at central bank liquidity†which works until it doesn’t. Kind of like a game of musical chairs, everyone seems fine until the music stops and someone is left without a chair. Unfortunately, in this game the average guy that dutifully puts money into their retirement plan or investment account is always without a chair when the music stops.

Of course, many people think this game can go on forever and it can certainly go on a lot longer than anyone would think possible, but in any Jenga economy, one little piece can be enough to topple everything.

Since the real foundation of any Ponzi fiat money scheme relies on confidence, when confidence ends, so does the scheme. So, the real question is, when will confidence evaporate? And the most likely answer is when people have lost everything and believe everything is lost.

I’m certain that you’ve heard that central bankers are out of tools, though they might deny this fact, every experiment since 1999, has merely bought time and every next crisis has been more violent and costly, weakening the real economy and creating a widening chasm of wealth inequality. So, what is the most critical tool? Interest rates, which have been anchored near zero since 2008.

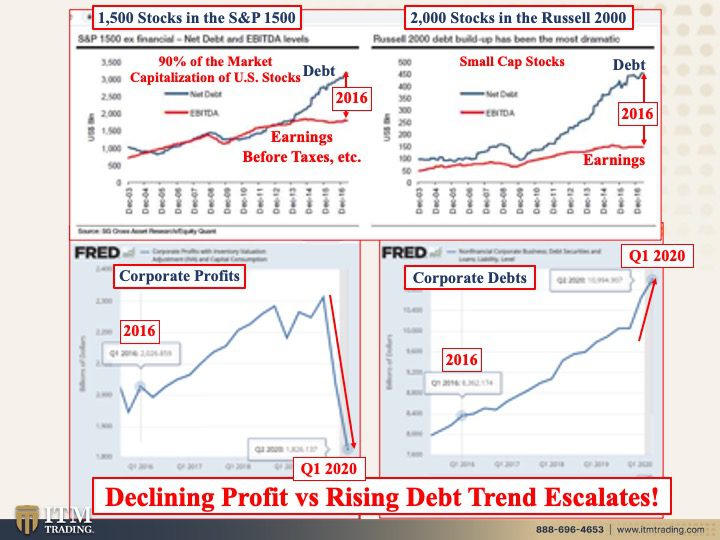

The cheap money debt binge made a too much debt problem even worse with trillions in both government and corporate negative yielding bonds now exploding well past the highs hit in 2016. Additionally, the cheap money inspired an explosion in leveraged loans, compounding the risk in the financial system at the same time that savers and those needing to generate income from their fiat money investments, were intentionally forced to take on more risk.

So desperate is this need for income, that investor protections have been allowed to diminish. Today roughly 80% of all leverage loans are covenant lite, meaning with almost no investor protections. If someone else is investing for you inside a retirement plan or through a mutual fund or ETP (Exchange Traded Product), it is likely that you are exposed. If I were you, I would read every prospectus on what you hold. Don’t take anyone’s word, do your own due diligence since perception does not hold up in a court of law.

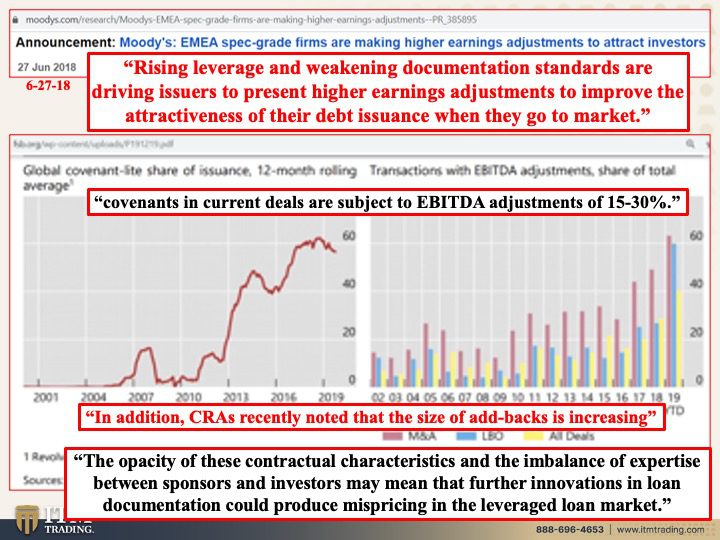

At the same time that our “protectors†at the SEC (Securities Exchange Commission), the DOL (Department of Labor) and the CFTC (Commodity Futures Trading Commission) have “relaxed†the laws put into place after the 2008 crisis. We’ve seen that the grading services, who are paid by debt issuers, have been more “flexible†in grading corporate debt, even as they admit that “Rising leverage and weakening documentation standards are driving issuers to present higher earnings adjustments to improve the attractiveness of their debt issuance when they go to market.†And that “covenants in current deals are subject to EBITDA adjustments of 15 – 30%â€. In other words, the investor has no real way of knowing if a company will be able to repay the debt they are issuing.

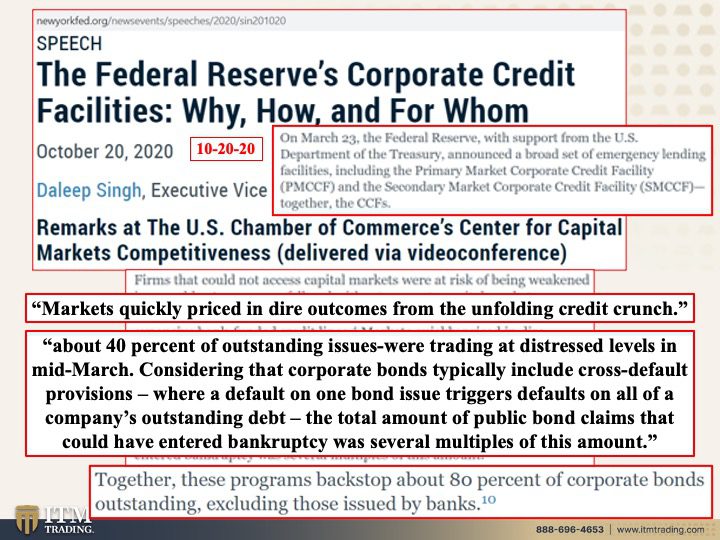

That brings us to today and the giant debt bubble, that already has lots of tiny air holes that require constant and massive money injections to hide the bankruptcy truth. On March 23rd, using the Coronavirus pandemic as an excuse, the Federal Reserve (private bank) created a “Corporate Credit Facility†big enough to “backstop about 80 percent of corporate bonds outstandingâ€. Just keep in mind that the taxpayer, you and me, are ultimately responsible for the central banks’ balance sheet.

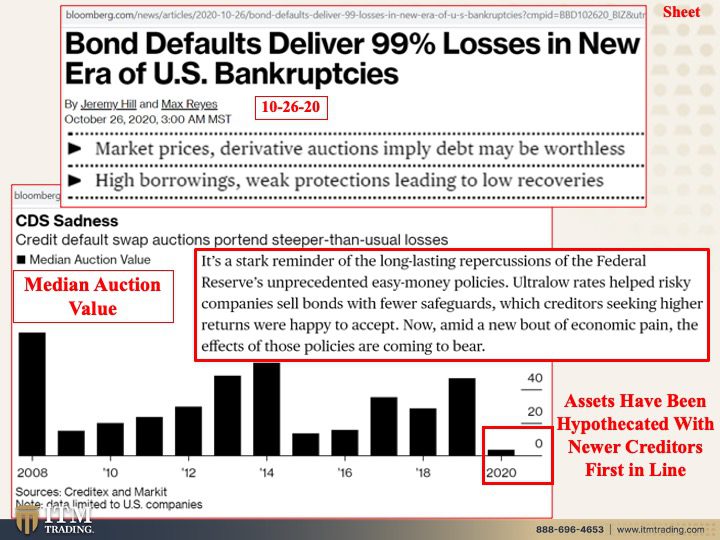

But what that also did, was inspire EVEN MORE RISKY DEBT at a time when default rates are rising globally. According to a recent Bloomberg article “Bond Defaults Deliver 99% Losses in New Era of U.S.

Bankruptcies†with many well-known names, like JC Penny and Neiman Marcus returning 2 to 3 cents on the dollar. Typically, a distressed bond in bankruptcy would have returned an average of 40 cents on the dollar so what has changed? Were you holding these bonds in any of your investment portfolios?

The rules. Remember that in 2005 bankruptcy laws were changed to put derivative holders at the front of the line ahead of other creditors.

Additional rule changes now allow pledged assets to be rehypothecated and used to back new debt. These new bond contracts give priority to new investors and push the old investors to the back of the line.

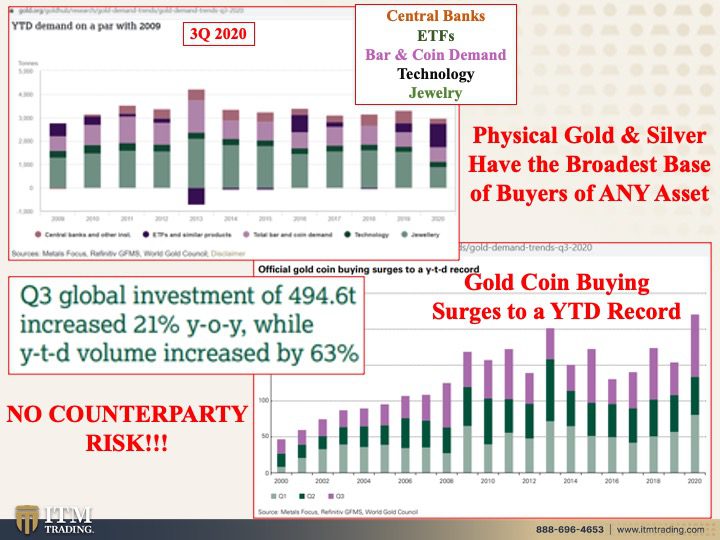

There are so many reasons I hold physical gold and silver, but primarily because they are the only real assets that run zero counterparty risks. I hold it and I own it. Got Gold?

Slides and Links:

Slide 1:

https://www.ft.com/content/498313d1-0e4e-4810-87c8-cda1f651c375

Slide 2:

https://www.bis.org/publ/qtrpdf/r_qt1909.pdf

https://www.fsb.org/wp-content/uploads/P191219.pd

https://inthelongrun.co.uk/2019/11/29/leveraged-loans-history-rhyming/

Slide 3:

https://fred.stlouisfed.org/series/CP

https://fred.stlouisfed.org/series/BCNSDODNS

https://upfina.com/net-debt-increasing-faster-ebitda/

Slide 4:

https://www.bis.org/publ/qtrpdf/r_qt1909.pdf

https://www.fsb.org/wp-content/uploads/P191219.pdf

https://inthelongrun.co.uk/2019/11/29/leveraged-loans-history-rhyming/

Slide 5:

https://www.newyorkfed.org/newsevents/speeches/2020/sin201020

Slide 6:

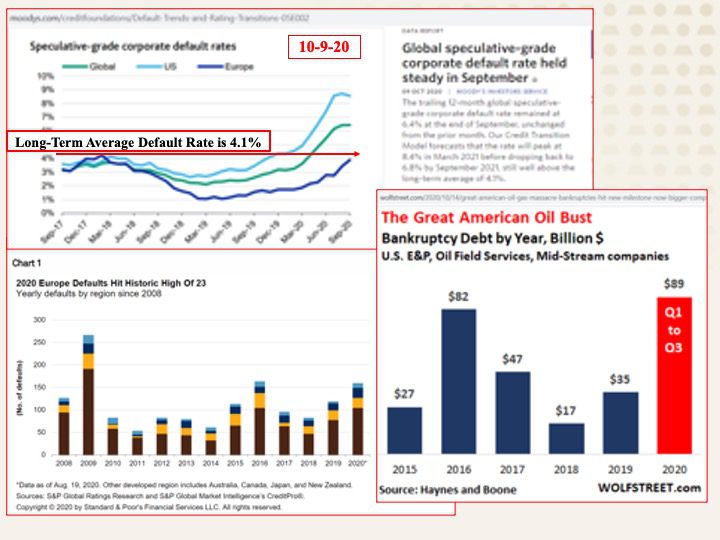

https://www.moodys.com/creditfoundations/Default-Trends-and-Rating-Transitions-05E002

Slide 7:

Slide 8:

https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q3-2020