THE NEXT CRISIS LOOMS: Solutions Failing for USD While the Shift to SOFR Stalls… by Lynette Zang

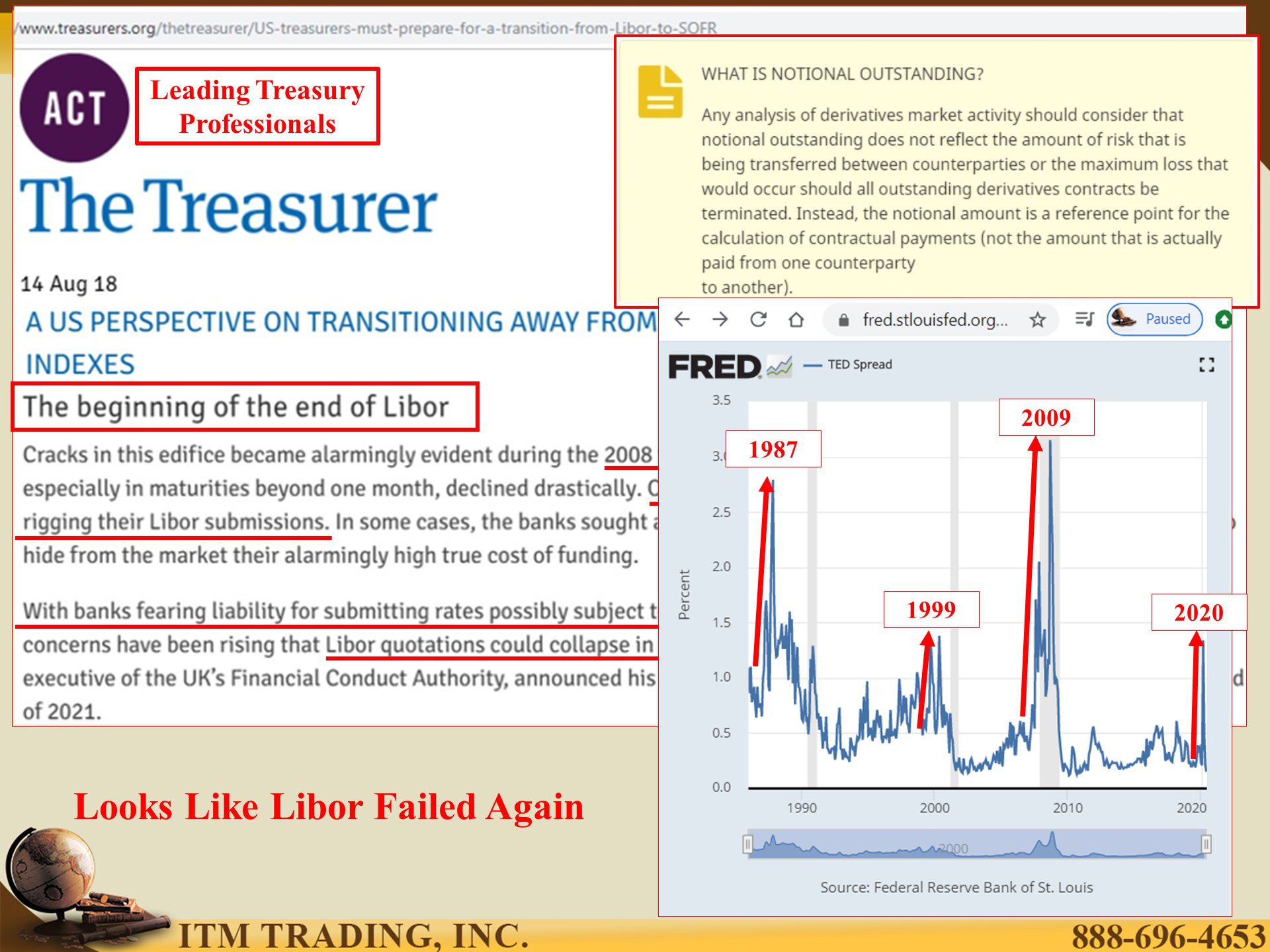

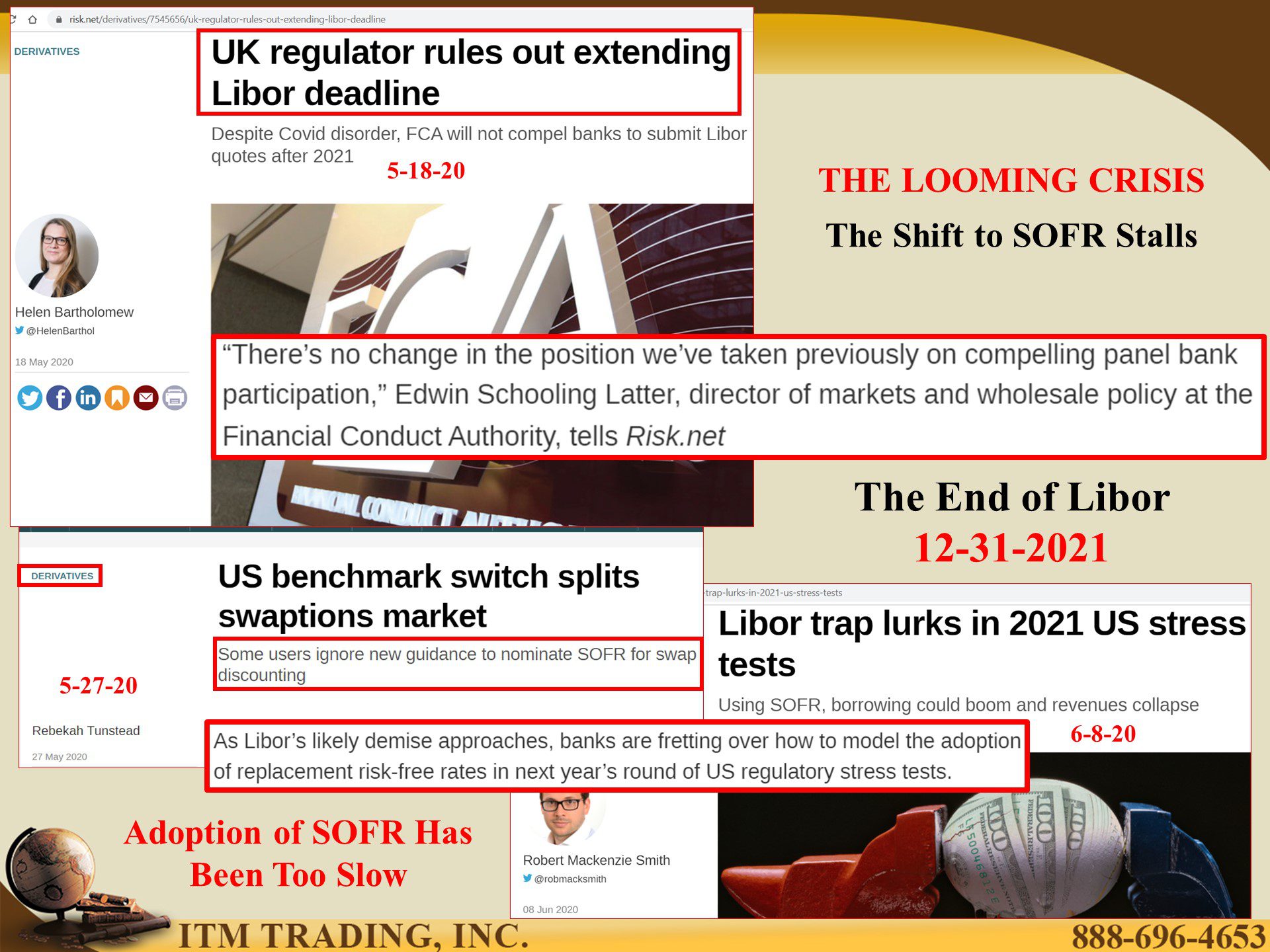

In 2012 manipulation of “THE†interest rate benchmark, known as IBOR (Inter Bank Offer Rate), was leaked to the public. The most globally used inter bank offer rate is London’s (LIBOR). Subsequently, the Bank of England (who was also implicated in the scandal), through the UK regulator, FCA (Financial Conduct Authority), announced the end of the IBORs on December 31, 2021.

Have more questions that need to get answered? Call: 844-495-6042

It is estimated that over $300 trillion contracts are tied to LIBOR, most mature AFTER that deadline. So several global central banks attempted to create a new benchmark, which required the development of a new market, so they could restructure all those debt contracts and tie them to the new benchmark.

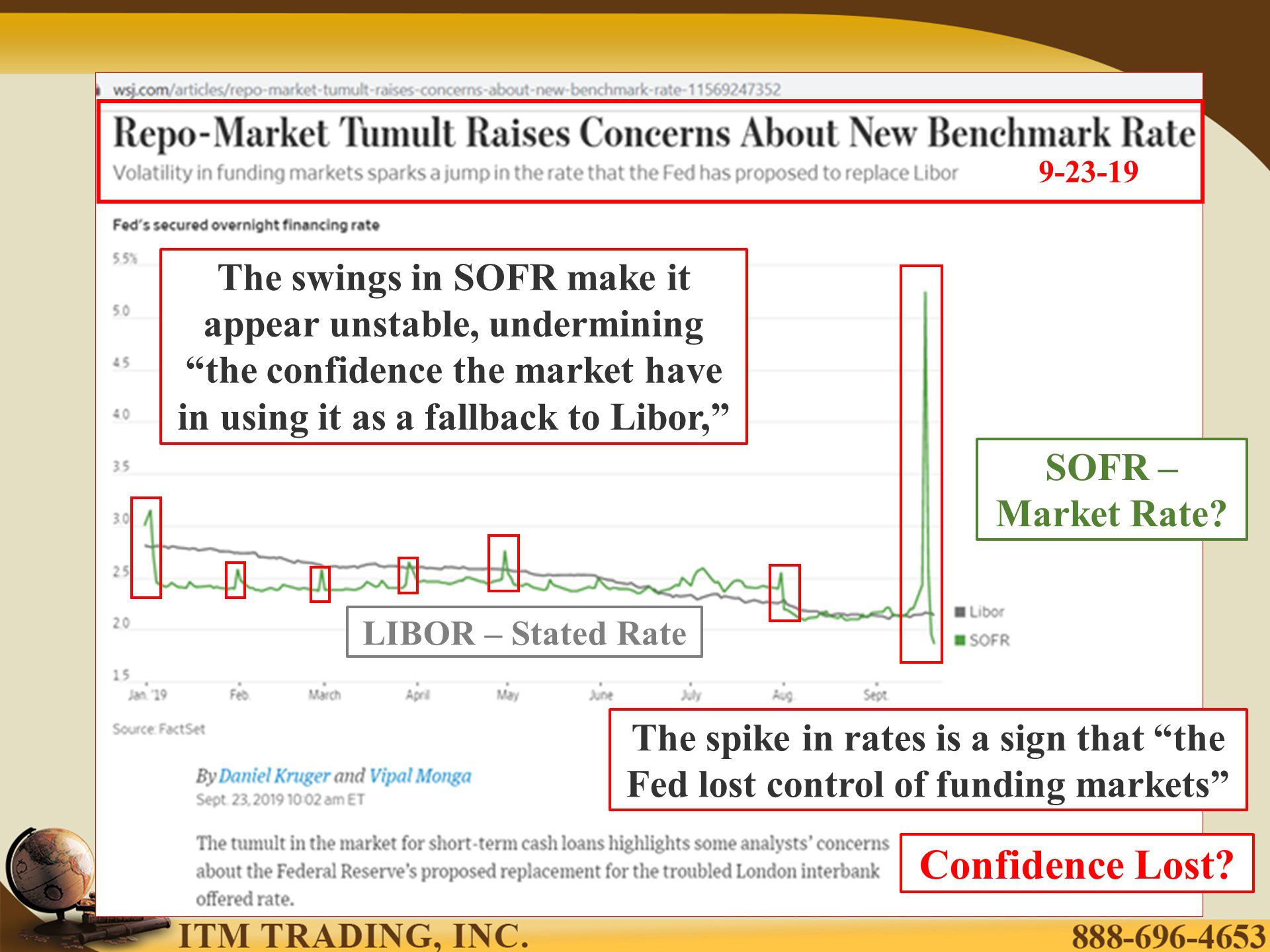

In the US the new benchmark is SOFR (Secured Overnight Financing Rate), and unlike IBOR which is merely a stated rate, SOFR is supposed to be based on actual transactions.

The Fed began publishing the rates for SOFR, along with LIBOR in the hopes that debt issuers would adopt SOFR as the benchmark in all the new contracts. The problem was that market adoption was too slow and new contracts continued to have LIBOR embedded in them.

SOFR was tested last September when the REPO market froze (short term corporate loans typically funded by money market mutual funds). It failed the test, money markets froze and the Federal Reserve was forced to inject trillions of newly created dollars to hide the truth from the retail public in order to prevent a repeat of 2008, when there was a run on money markets.

Enter the Coronavirus with unlimited central bank new money debt contracts.

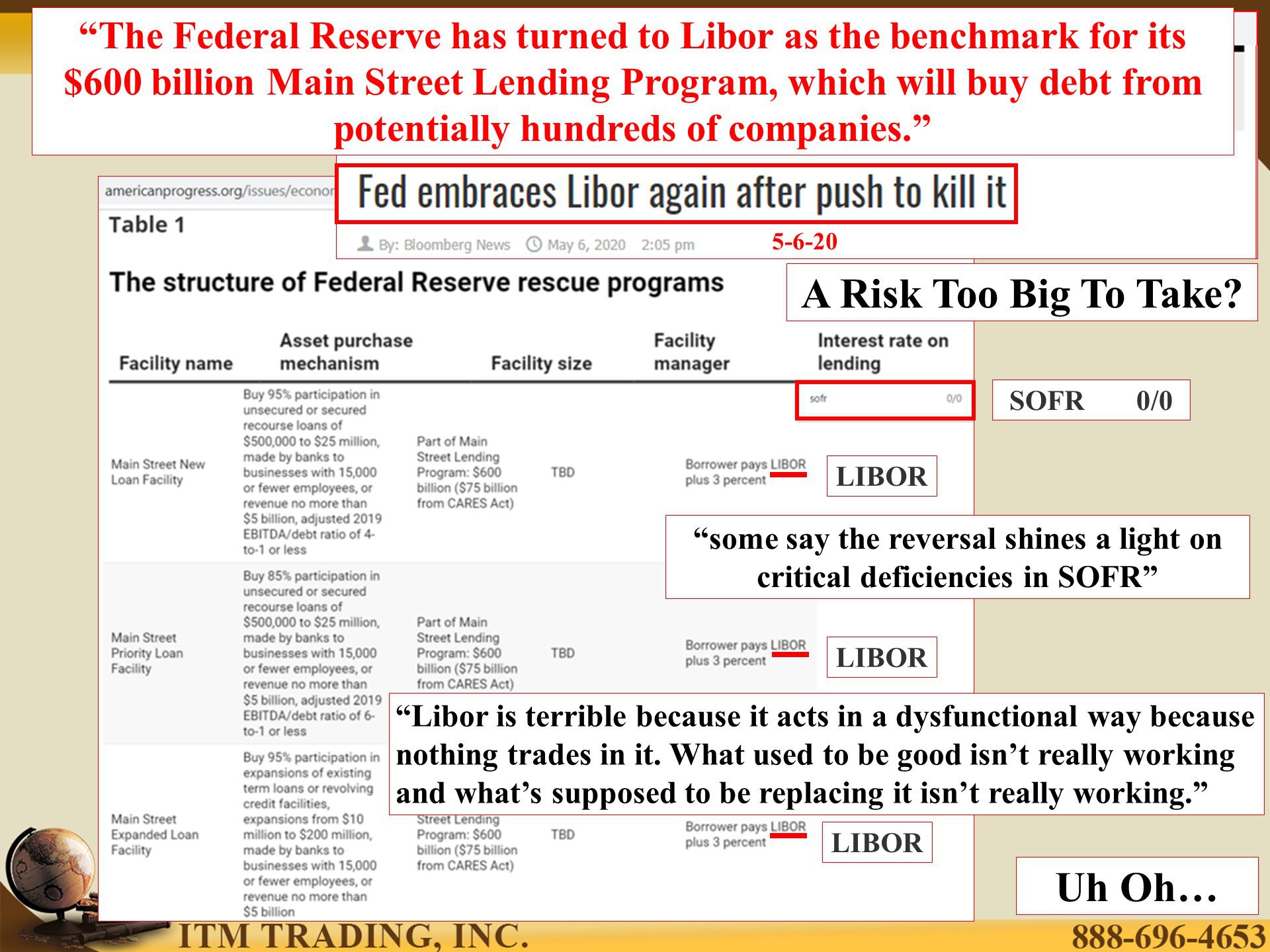

Now one might think that this would be a perfect opportunity for the Fed to solidify the position of SOFR into all these new contracts, but when the Fed set up the three “Main Street Lending Facilities†ALL NEW CONTRACTS ARE TIED TO LIBOR!!!

In fact, upon examining the structure of all the Federal Reserve “rescue†programs, SOFR is not mentioned even once. Even though the FCA came out recently and reiterated the end of IBORs, including LIBOR on December 31, 2021.

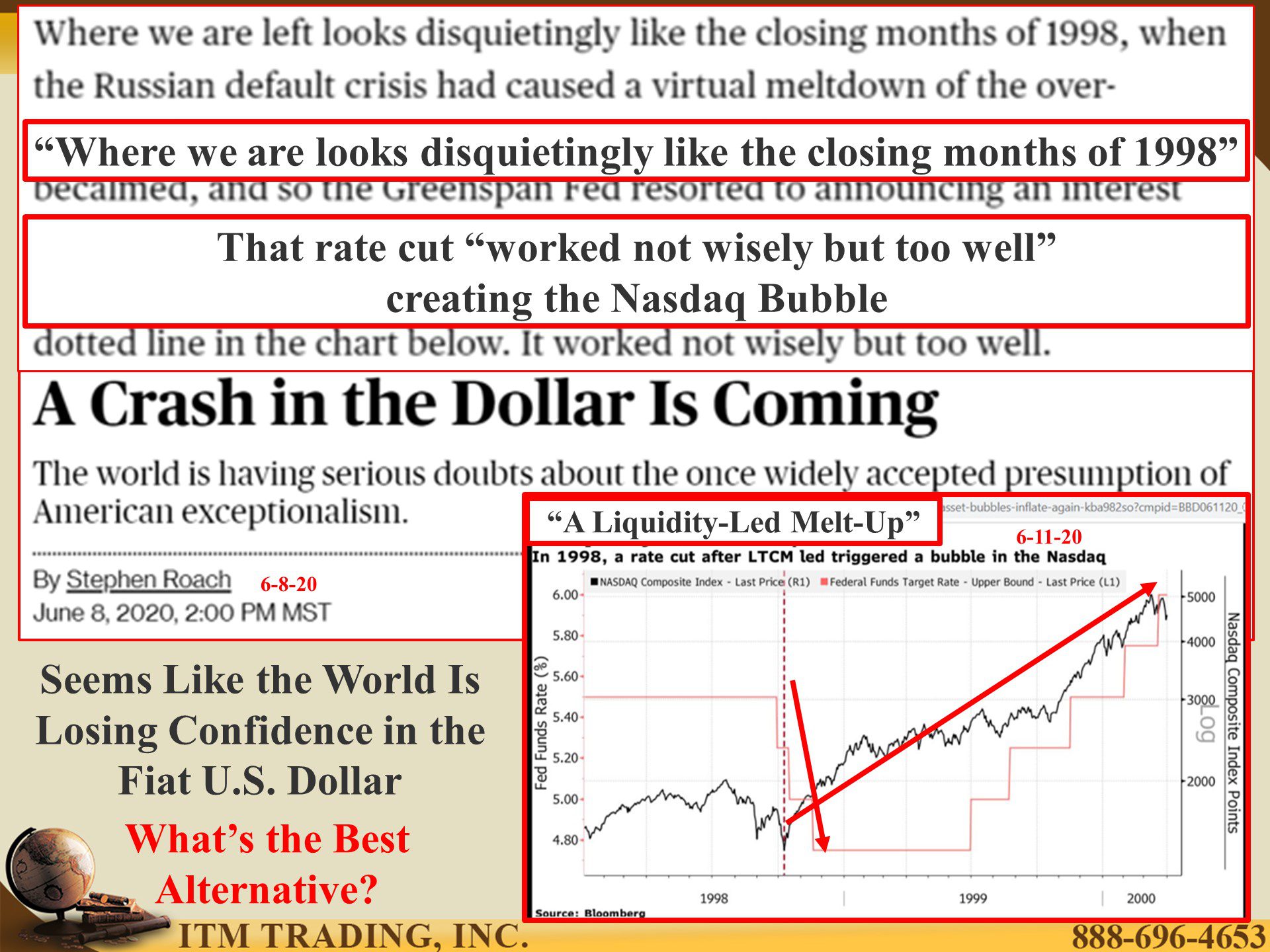

What does this mean to us here in the US? Most likely the obvious end to the USDs global position as “The†World Reserve Currency because, as Stephen Roach, PhD writes in a Bloomberg article on June 8th “A Crash in the Dollar Is Coming†because the “world is having serious doubts about the once widely accepted presumption of American exceptionalismâ€. In other words, as the world loses trust in the dollar, they will stop using it in global trade and send those dollars home and voila, hyperinflation.

Now you might think of this as a random opinion, and I can say that I don’t always agree with what he writes, but he serves as senior fellow at Yale University’s Jackson Institute for Global Affairs and a senior lecturer at Yale School of Management. He was formerly chairman of Morgan Stanley Asia and chief economist at Morgan Stanley, the New York-based investment bank and participates in many IMF (International Monetary Fund) Global Economic Forums, so I’d say he is an “Insider†and I do agree with him on this because I’ve been watching the USDs demise as “The†World Reserve Currency since December 2002, when the Fed first began buying US Government debt.

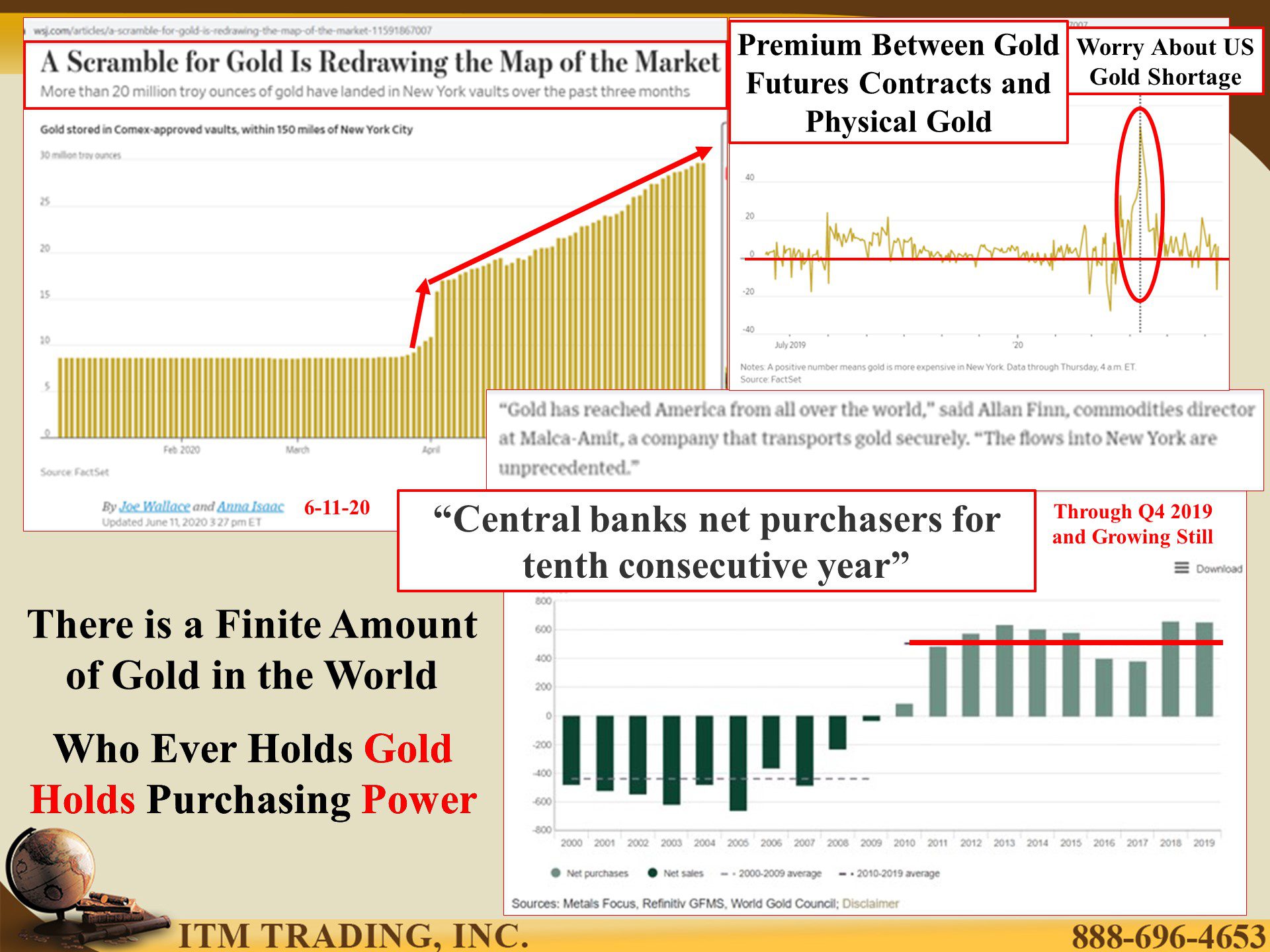

What is the best shield to protect the individual from the looming hyperinflationary depression? Real money gold. Now you might say that I only say that because we at ITM Trading sell gold (and silver) but think back to March and April. There were shortages and premium spikes. Plus, this is not our first rodeo and we experienced similar shortages and premium spikes in 2008 as well. But 2020’s experience made 2008’s look tame by comparison.

Additionally, central banks have been net buyers of gold since 2008 as well, with the most gold accumulation in history happening right now. Why? Because they know the end is very near for not just the USD but for all government fiat money. They know and talk about the need for a global financial system “resetâ€. They want to be holding as much real money gold as possible when the reset occurs because they know that whoever holds gold, holds real value and therefore, holds power. And now you know that too.

Slides and Links:

https://www.risk.net/derivatives/7550061/us-benchmark-switch-splits-swaptions-market

https://www.risk.net/derivatives/7545656/uk-regulator-rules-out-extending-libor-deadline

- https://www.wsj.com/articles/repo-market-tumult-raises-concerns-about-new-benchmark-rate-11569247352

- https://www.wsj.com/articles/fed-makes-terms-more-favorable-for-main-street-lending-program-11591644678?mod=cxrecs_join#cxrecs_s

https://finance-commerce.com/2020/05/fed-embraces-libor-again-after-push-to-kill-it/

https://finance-commerce.com/2020/05/fed-embraces-libor-again-after-push-to-kill-it/

https://www.bloomberg.com/opinion/articles/2020-06-08/a-crash-in-the-dollar-is-coming?sref=rWFqAg1Y