THE LEVEL OF LIES: The Truth About Municipal Bond Investments You Thought Were Safe… By Lynette Zang

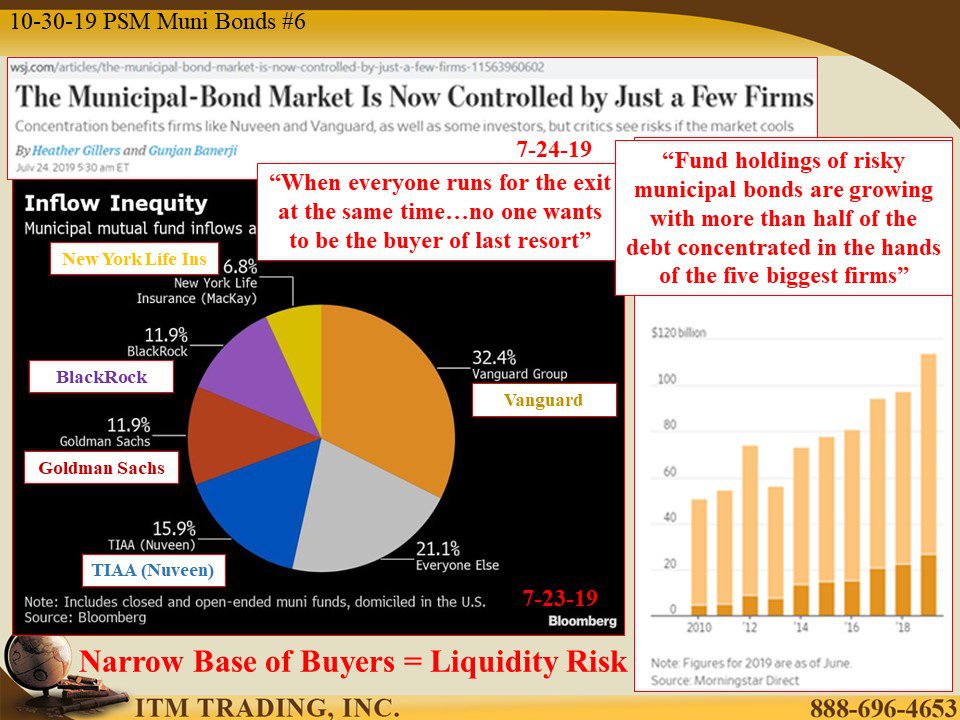

The total size of the municipal market has more than doubled since 2008 from $2.8 trillion to $6.96 trillion as of September 2019 as the base of buyer has shifted from individuals to five large fund managers (institutional investors); Vanguard, TIAA (Nuveen), Goldman Sachs, BlackRock and New York Life Insurance Company.

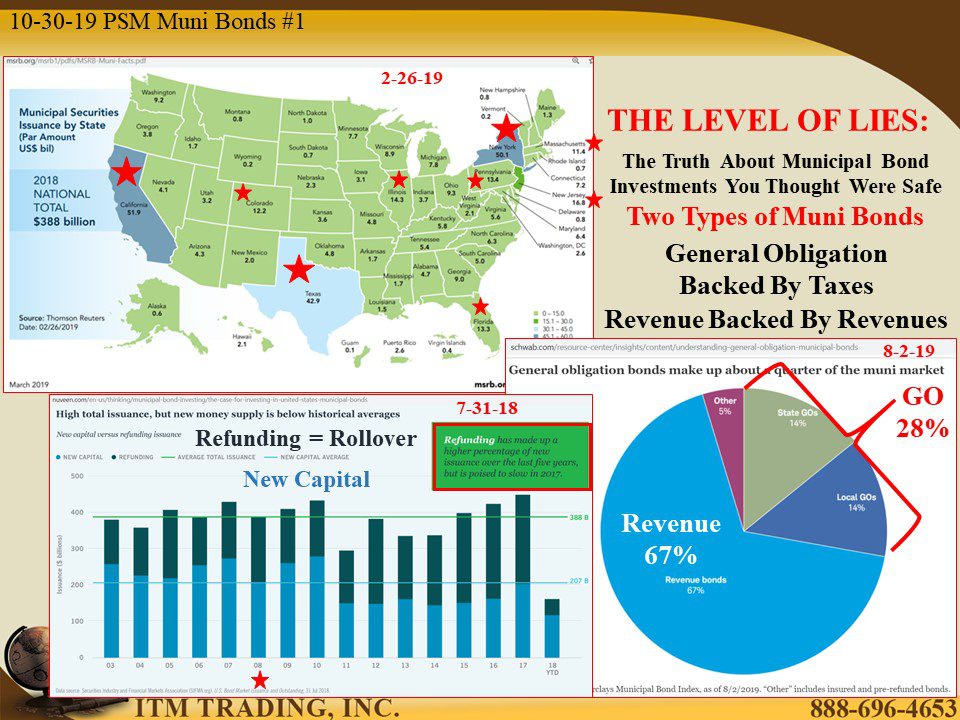

There are two types of municipal bonds; General Obligation (GO) bonds that are backed by taxes and/or assets of the state or municipality and Revenue bonds, backed by revenues of the facility that issued the bonds. Within revenue bonds, some are for essential services, like water, but some entities, like private colleges, may also be allowed to issue municipal revenue bonds. Did you know?

GO bonds are roughly a quarter of all issued muni bonds, with the lion share of issues going to revenue bonds. In addition, particularly since 2008, debt rollovers have dominated newly issued bonds, which could indicate states taking advantage of low rates to refinance and lower their borrowing costs.

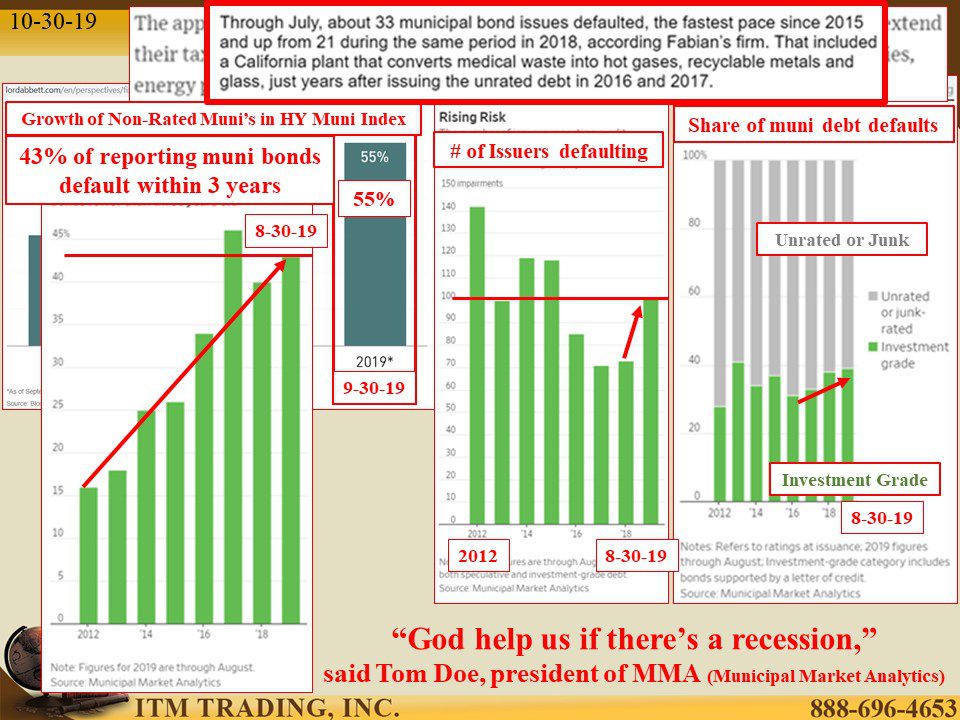

But it could also indicate that states are in financial stress, spending more than current tax revenues can support (GO bonds). Or with the rapid growth of unrated and junk municipal bonds, which as of 9-30-19 make up a full 55% in the benchmark (standard) high yield muni bond index; it could indicate that entities that would not have access to the markets, now do, thanks to the reach for yield and current flight to safety.

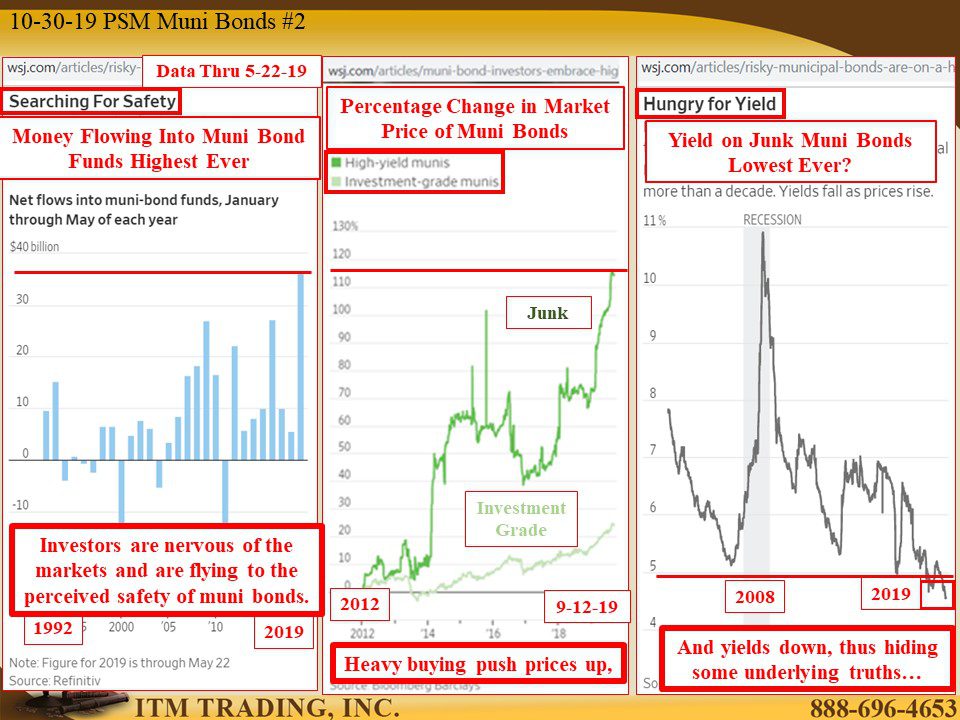

But the question must be asked, “Are municipal bonds as safe as we’re led to believe?†Because as investors seek safety, net money flows into muni-bond funds is at the highest level ever. As this money has flowed into funds, most have gone into junk and driven yields down to the lowest level ever. But what’s the risk?

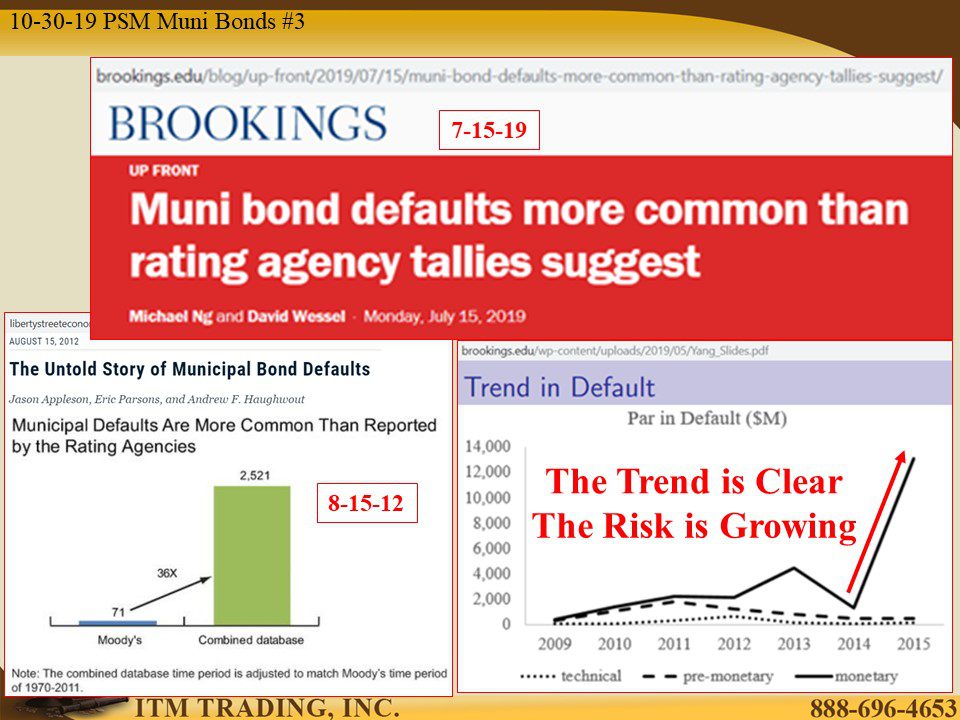

If you look to the grading services, they say the risk is small, but studies conducted by the New York Fed in 2012, as well as a 2019 study by the Brookings Institute, tell a very different story because rating agencies only report on those bonds THEY have graded, which leaves out a huge swath of the market.

In fact, according to the WSJ, as of 8-30-19, 43% of reporting muni bond issuers default within 3 years! And while most are unrated or junk, the number of investment grade muni bond defaults has been growing since 2016 and is now escalating at a rapid rate as compared to 2018. “Through July, about 33 municipal bond issues defaulted, the fastest pace since 2015 and up from 21 during the same period in 2018.†Why didn’t holders of these funds know? Because as yields fall, bond prices rise and hide the default trend. But for how long?

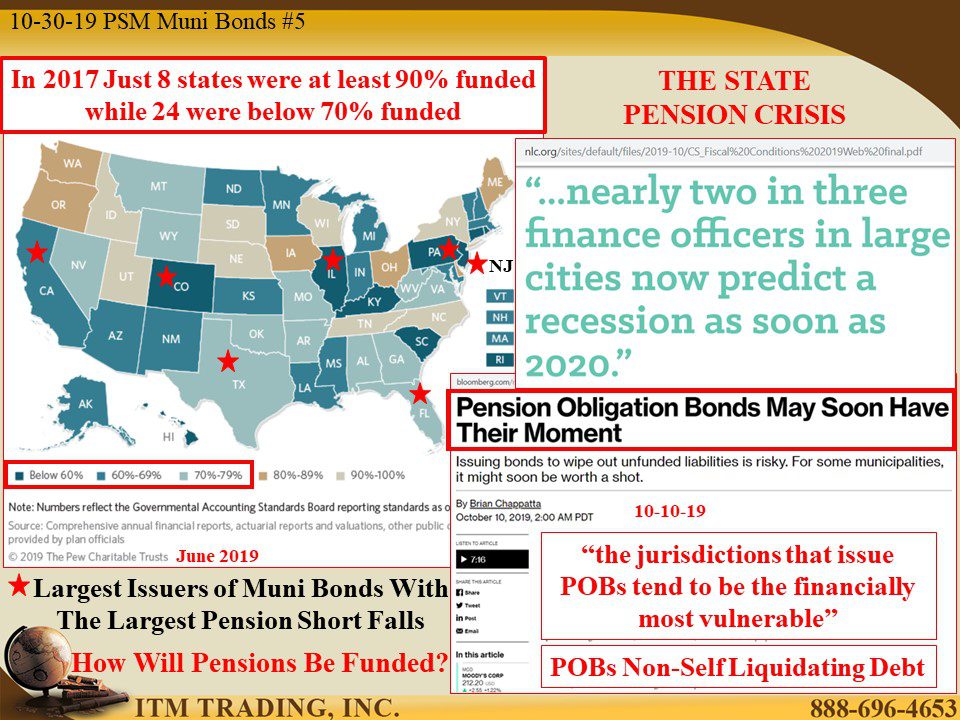

With “nearly two in three finance officers in large cities now predict a recession as soon as 2020,†which could create a crisis in funding day-to-day operations, almost half of US states have pension obligations that are below 70% funded. How will all this “required spending†be funded? Keep in mind that any debt issued for these purposes is non-self-liquidating debt, meaning that once the money is spent, it is gone and will require higher taxes and/or benefit cuts to keep the state going.

At the same time, the base of buyer in the muni market is concentrated in just a few hands (as mentioned above), so what do you think will happen when investor head for the door? “When everyone runs for the exit at the same time…no one wants to be the buyer of last resortâ€. Goldman Sachs is the third largest holder of muni bonds and is also a G-SIB (Globally Systemically Important Bank) and therefore a threat to the global financial system.

So far, eleven states have moved to protect their citizens by passing legal tender laws that put sound money (gold and silver) as a fiat money alternative, which I think, is a very good thing. Is your state one of them? If not, you might want to see what you can do to help. In the meantime, you can create that protection for yourself and your family, which I think, is a very good idea.

Slides and Links:

http://www.msrb.org/msrb1/pdfs/MSRB-Muni-Facts.pdf

https://www.wsj.com/articles/muni-bond-investors-embrace-higher-risk-issuers-11569073815

https://www.brookings.edu/wp-content/uploads/2019/05/Yang_Slides.pdf

https://wsj.com/articles/muni-bond-investors-embrace-higher-risk-issuers-11569073815

https://www.nlc.org/sites/default/files/2019-10/CS_fiscal%20Conditions%202019Web%20final.pdf.pdf

YouTube Short Description:

The total size of the municipal market has more than doubled since 2008 from $2.8 trillion to $6.96 trillion as of September 2019.

If you look to the grading services, they say the risk is small, but studies conducted by the New York Fed in 2012, as well as a 2019 study by the Brookings Institute, tell a very different story because rating agencies only report on those bonds THEY have graded, which leaves out a huge swatch of the market.

In fact, according to the WSJ, as of 8-30-19, 43% of reporting muni bond issuers default within 3 years!

So far, eleven states have moved to protect their citizens by passing legal tender laws that put sound money (gold and silver) as a fiat money alternative, which I think, is a very good thing. Is your state one of them? If not, you might want to see what you can do to help. In the meantime, you can create that protection for yourself and your family, which I think, is a very good idea.