PSM Part 2 – FED ADMITS THE RESET: New Pattern Shift Revealed! by Lynette Zang

In this series, we are examining each of the four parts discussed in the recent Federal Reserve Financial Stability Report. Today we are looking at two: Excessive borrowing by businesses and households and the Impact on the economy.

Interestingly, since that report came out, Fed Chair Powell spoke at the ECB Forum on the topic of “Central banks in a shifting world”. Justifying central bank choices and referencing productivity. To be clear, productivity measures output per unit of input, such as labor and Is directly linked to corporate profits and shareholder returns. He stated that “Over a long period of time those gains tend to be shared.”

Have more questions that need to get answered? Call: 844-495-6042

While this statement was true up until 1971, when we went on the debt standard managed by central bankers, data reveals that between 1979 and 2018, productivity grew 69.6% but the average hourly pay only grew by 11.6%. The covid pandemic has exacerbated this divergence and created a bifurcated economy.

Those at the top have experienced massive nominal wealth growth because of the unlimited amount of support provided by central banks with the Fed leading the pack. While those on the bottom are falling into abject poverty as those pittance programs provided on the onset of the crisis In March, wind down.

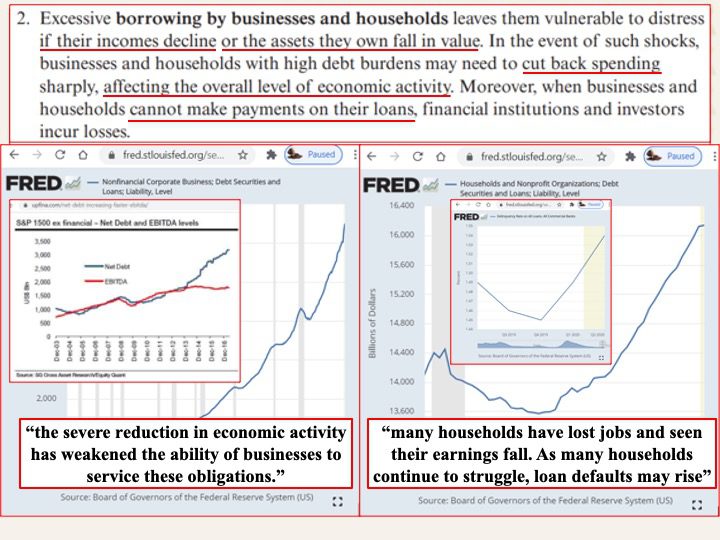

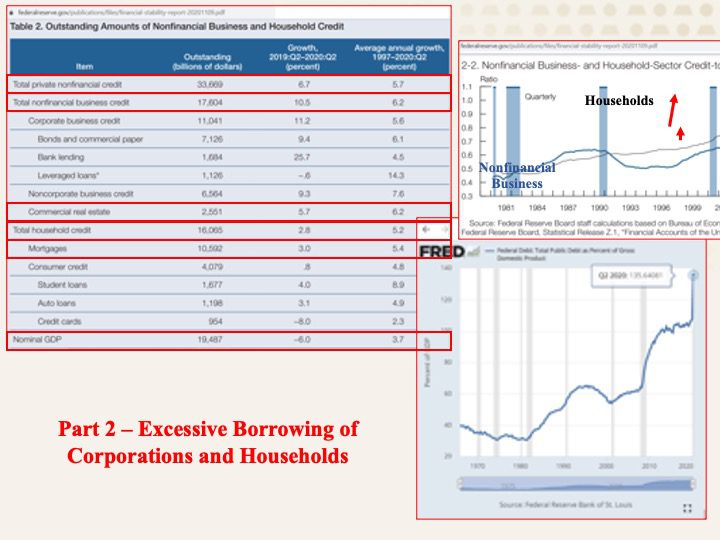

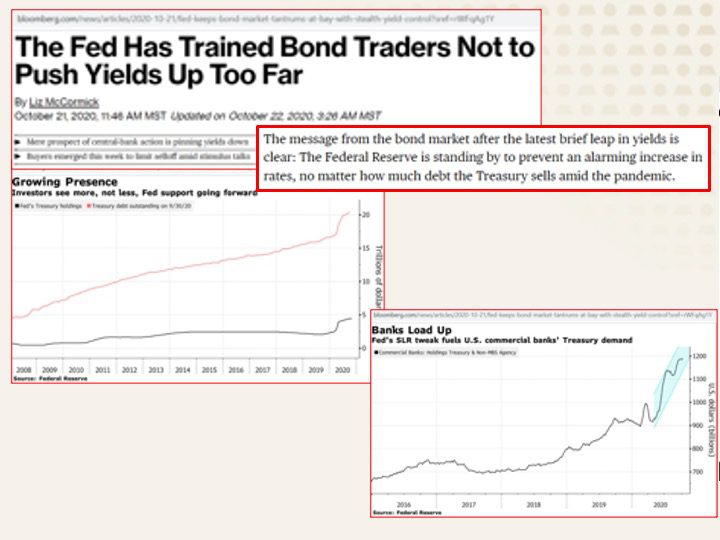

In part 1, the Fed admitted that their ZIRP (zero Interest rate policy) boosted asset prices. Well guess what, the almost 40-year trend of lowering Interest rates has allowed debt levels to grow to unfathomable levels as well, since it is easier to service and accumulate debt the lower interest rates are.

Both corporations and individuals have become addicted to this debt for different reasons.

Individual consumption is the driving engine of the economy at almost 70% of GDP. Corporate borrowings have enabled outsized top management compensation, share buybacks and dividend payouts. All of which enrich the few at the cost of the many. So sorry Mr. Powell, your statement on sharing the gains is a bold-faced lie.

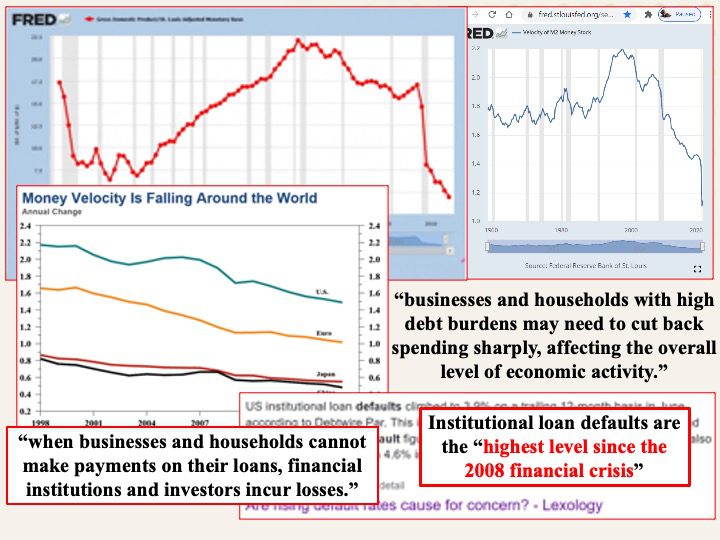

That brings us to the real central bank problem, which is deflation. Make no mistake, when a market’s nominal value falls, that is deflationary. Further, when individuals see that nominal price drop their spending may be impacted. Markets up let’s spend more, markets down we need to spend less.

But there is only one way to fight deflation and that’s with inflation and that requires more new money which, in the current system, is created from debt.

So the big question is, how to keep this debt bubble floating when interest rates are stuck at zero, (so you can’t lower them to enable more debt) and corporate and individual incomes are falling, (so you can’t service the debt you already have).

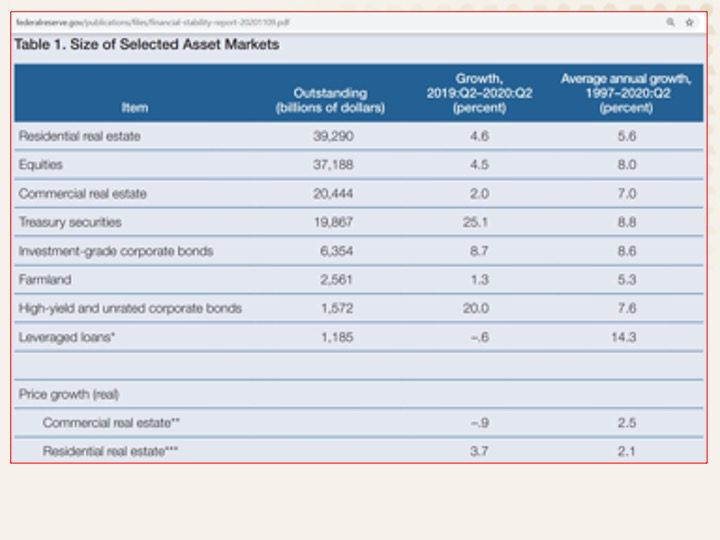

In part 1, the Fed admitted that their ZIRP (zero Interest rate policy) boosted asset prices and strong evidence suggests that almost all markets are in extreme bubble territory. Well guess what, the almost 40-year trend of lowering Interest rates has also created an insurmountable debt bubble that is already popping as witnessed by global inverted yield curves and the inability of any country to raise rates since 2009.

As these bubbles are popping the global central bankers, led by the Fed, are hyperinflating the money supply to keep this ponzi scheme going until new digital systems are in place. This is not lost on gold.

A new pattern shift is emerging! The M1 money stock and spot gold are now correlated. Not a surprise since the real battle is fake fiat money versus real gold money. But what is not as apparent in these graphs is that while spot gold is merely a contract, and can be created in unlimited amounts, real gold is finite with supply diminishing.

And while I always viewed physical gold and silver as key portfolio diversifiers, never has it been as important as it is now to hold real wealth out of this crumbling financial system.

Slides and Links:

Slide 1:

https://www.cnn.com/2020/11/12/economy/economy-after-covid-powell/index.html

Slide 2:

https://fred.stlouisfed.org/series/DRALACBS

https://fred.stlouisfed.org/series/HDTGPDUSQ163N

https://fred.stlouisfed.org/series/BCNSDODNS

https://fred.stlouisfed.org/series/M2V

Slide 3:

https://fred.stlouisfed.org/series/GFDEGDQ188S

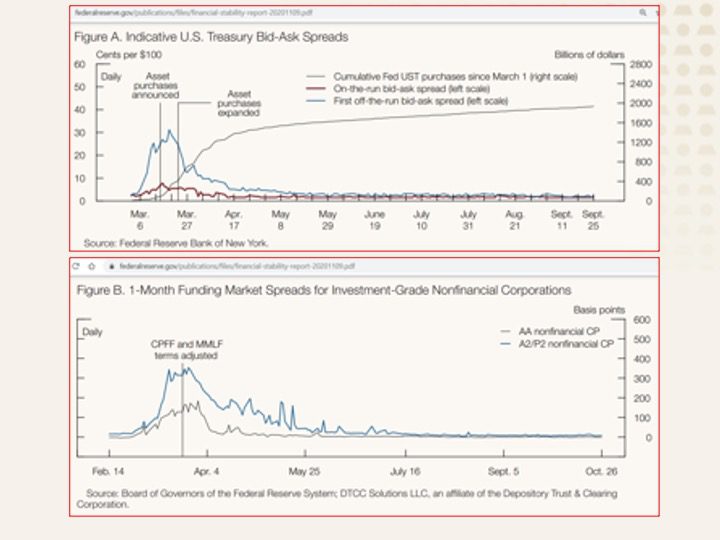

https://www.federalreserve.gov/publications/files/financial-stability-report-20201109.pdf

Slide 4:

https://www.federalreserve.gov/publications/files/financial-stability-report-20201109.pdf

Slide 5:

https://www.epi.org/productivity-pay-gap/

Slide 6:

https://fred.stlouisfed.org/series/M2V

Slide 7:

Slide 8:

https://www.federalreserve.gov/publications/files/financial-stability-report-20201109.pdf