NEW IMF RISK REPORT: Your Risk Increases By the Day!

TRANSCRIPT FROM VIDEO:

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, a full service, physical gold and silver dealer, specializing in custom strategies to help all of us, frankly, get through the reset that should be pretty darn obvious to everybody that we’re already walking through. And over the weekend, the IMF came out with their global financial stability report. Well, I think it’s pretty important to know how stable things are and also how the risk is really hidden from you. So that’s what we’re going to talk about today. And as always, if you want to be the first to get notified, when I do these really urgent videos, you know, now look did crisis erupt over the weekend. No, but this is a really key report because it shows you where the vulnerabilities lie and how the risk has been transferred to you. Don’t you want to know that? So let’s just dive right in.

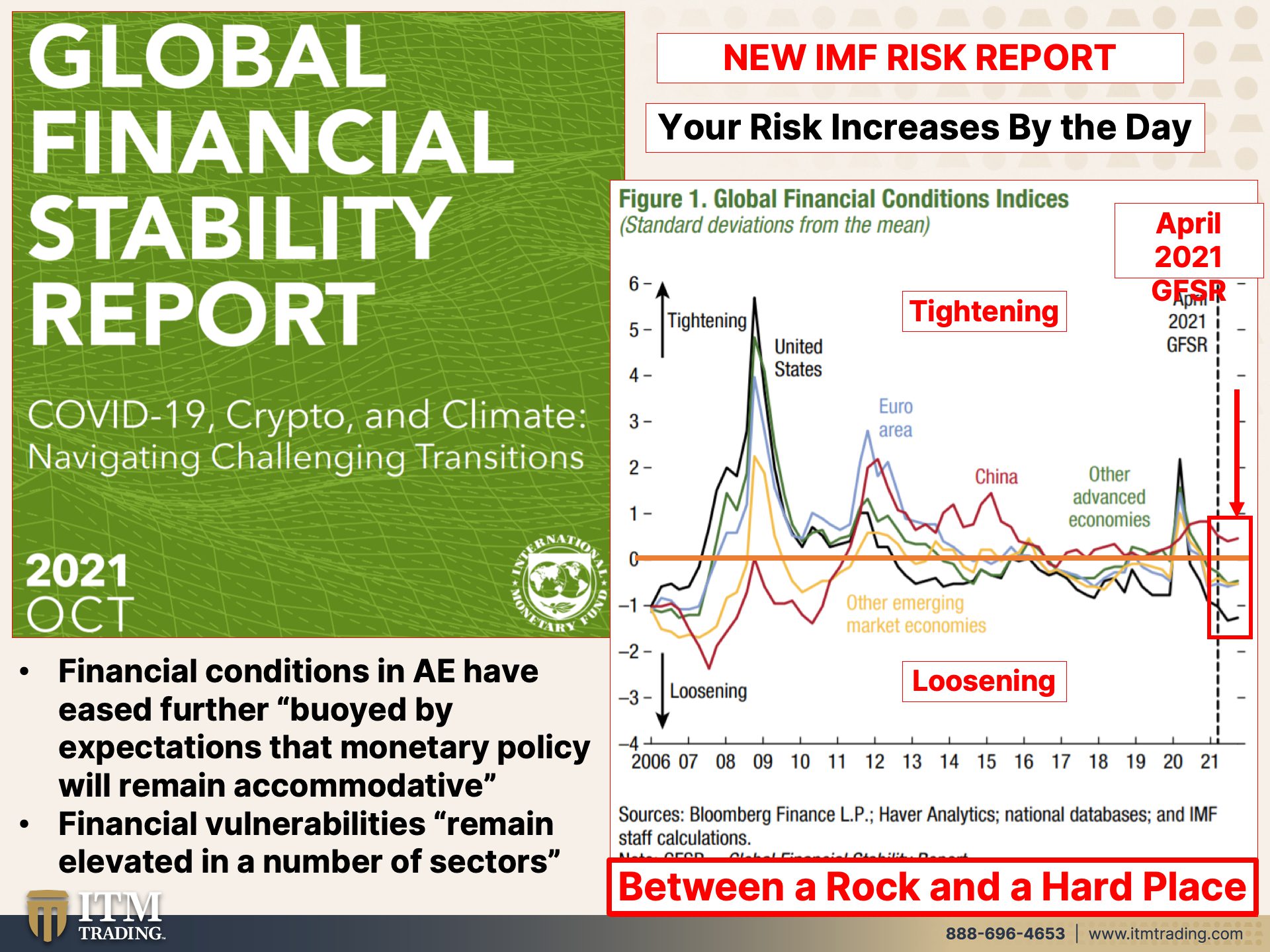

Okay. Your risks are increasing every single day. Do you know that? Do you realize it? It’s really why we need to make sure that we are protected and as self-sufficient as possible, I love the title, global financial stability report. COVID-19 crypto and climate navigating, challenging transitions. We have an awful lot of transitions that we need to navigate, and what’s been the central banker global answer? Well, easier credit, more debt, because that’s what the system is based on is credit and debt. So up here, it’s where they’re tightening and you can see here’s 2008. So when a crisis hits, that’s when the tightening occurs, here’s 2020. This is when the tightening occurs. Now the, the us is in a black line, but it doesn’t frankly really matter because everybody’s the same. So what they say in the report is financial conditions in advanced economies, AE, advanced economies have eased further boy played by expectations that monetary policy will remain accommodate of another words that they will keep printing new money and issuing cheap credit to support the markets. Those that have been chosen to win in this game. You can make it that you’re the one that wins and therefore for everybody around you, but central banks don’t really choose to do that. So you can see this is in April. They came out with their last global financial stability report. And since then this one just came out in October 2021. You can see that yep. Conditions remained very accommodative, very easy for those that have access to those funds. So not the normal guy on the street typically, but the big kahunas, the banks, the big tech companies, the big corporations, etcetera, but they also state that financial vulnerabilities remain elevated in a number of sectors. And we’re going to be looking at those sectors here shortly, because quite honestly, central banks are between a rock and a hard place. Now it is certainly of their own doing because in a normal capitalist system, if you make a mistake and you fail, you fail.

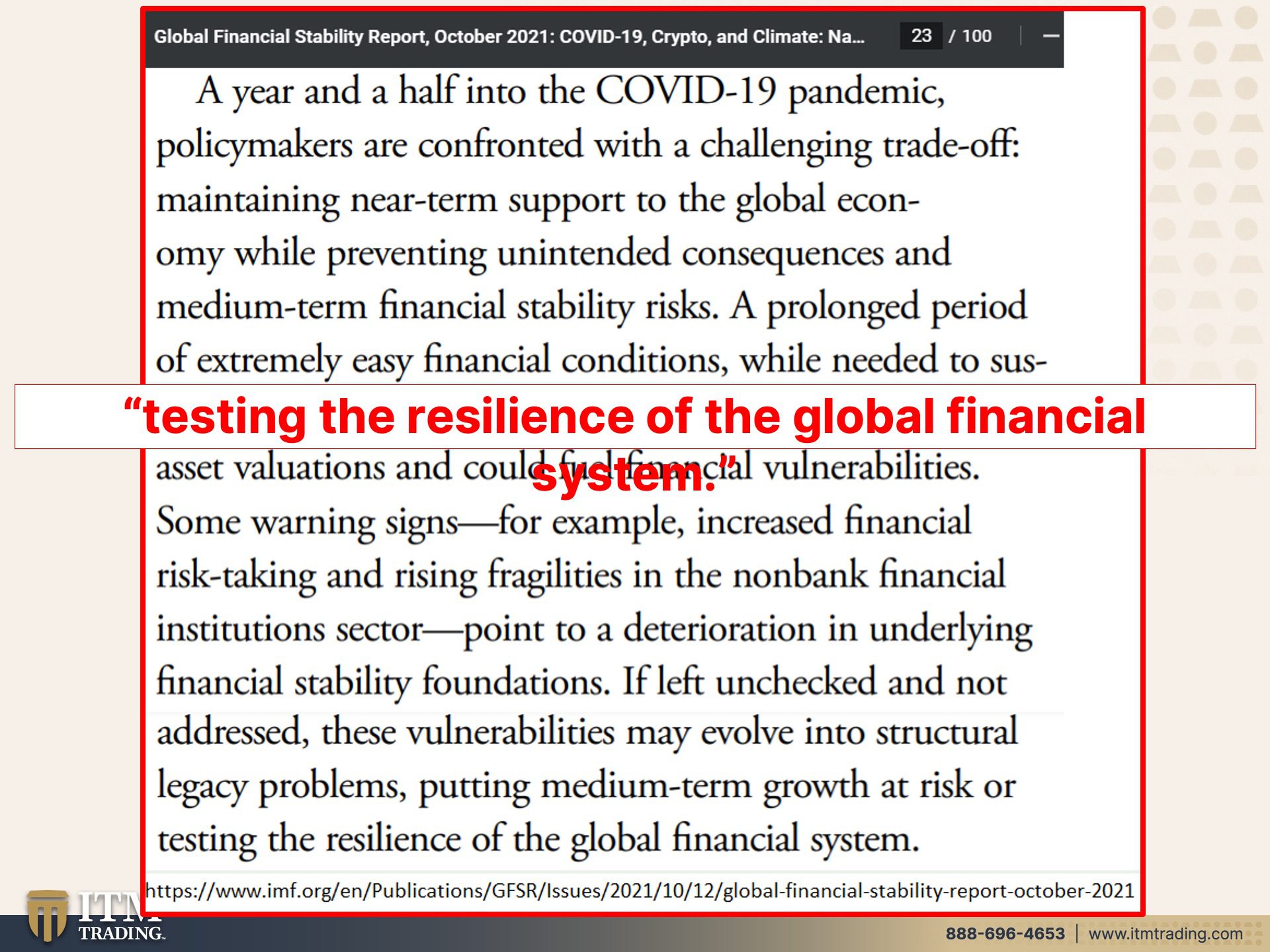

But in the system that we’re in the crony capitalism, really more, even towards fascism, since corporations are clearly more important than the individual, you get bailed out, the taxpayer bails you out. And I really like you to keep in mind that every time they talk about the government spending money, what the government is doing is spending your money. Now, forgive me on this. I’m going to read this whole thing, but I’m going to stop and make comments along the way, because there’s a lot of stuff to comment. And in here, so a year and a half into the COVID-19 pandemic, policymakers are confronted with a challenging trade off, maintaining near term support to the global economy. So in other words, continuing to print money and give money away for free to those that are closest to the central banks. And let’s see while preventing unintended consequences and medium term financial stability risks. So what are those unintended consequences? Well, some of them they don’t even know about yet. Some of them they’ve discovered like in the reverse repos where they’re now trying to maintain that after unleashing that genie not going very well demand continues to be extremely strong, like trillions of dollars in a day. A prolonged period of extremely easy financial conditions while needed to sustain the economic recovery may result. It might it hasn’t done this yet. According to this report, but may result in overly stretched asset valuations, you think, and could fuel financial vulnerabilities. Yeah. You think because what goes up, nothing goes straight up. None of that goes straight down. You always have to have some bouncing, but there hasn’t been very much bouncing to the upside because that’s where the government and the central banks want you to hold your wealth inside the markets, because it’s very easy to take it away from you and who you going to call Ghostbusters?

Yeah. Now I like this one, some warning signs, and we’re coming back to this in another slide. Some warning sock signs, for example, increased financial risk taking and raising fragilities, rising fragilities in the non-bank financial institutions sector. So FinTech, etcetera point to a deterioration in underlying financial stability foundations. So there is a growing vulnerability in the foundation of the global financial system. This is what they’re really saying to them. Do you point to a deterioration? Okay. If left unchecked. Oh, blah-blah-blah it is unchecked because if they stop and I know that, well, look at what just happened in Australia, right? They came out and said that they will buy, they will protect with the yield curve control, which all of the central banks are doing. And what that means, just to explain it for those that aren’t familiar with it, that the central banks are making an attempt to control the interest rates, whether they’re short term, which the overnight rate is a direct function. They say, okay, this is what the rate is. Or the longer term bond rates, which is a function of buying the bonds to suppress the interest rates. And they want to control it across the whole channel. Well, Australia over the weekend, Friday, really. And then over the weekend, it was a big fat fail with their interest rates, spiking, and that now tests all of the central banks. So we’re keeping an eye on that, but that is a huge vulnerability that has evolved. And we’ll see if they can get that back under control. I’m not sure yet, but we’ll find out. But here it is, these vulnerabilities may evolve into structural legacy problems like the, it did prior to 2008 with the derivatives. Now all of those, they call them legacy derivatives because they cannot get rid of them. They have to keep paying the fees to keep them floating because they were so unique. So that changed the structure of the derivatives market permanently. And that’s what they’re talking about here may evolve into structural legacy problems. Now on this, I would say it’s because everything is based on your never ending ability to grow more debt, not you or me, but the corporations and governments ability to just continue to grow debt when it’s already at beyond nosebleed levels, that puts medium term growth at risk, or, and here’s the piece testing the resilience of the global financial system. And while I cannot make you any guarantees, I’m not even going to give myself any fudge room. I am a hundred percent certain that the resilience of this global financial system will be tested. And I’m also a hundred percent certain that it will fail the test and that will justify ushering in a whole new system.

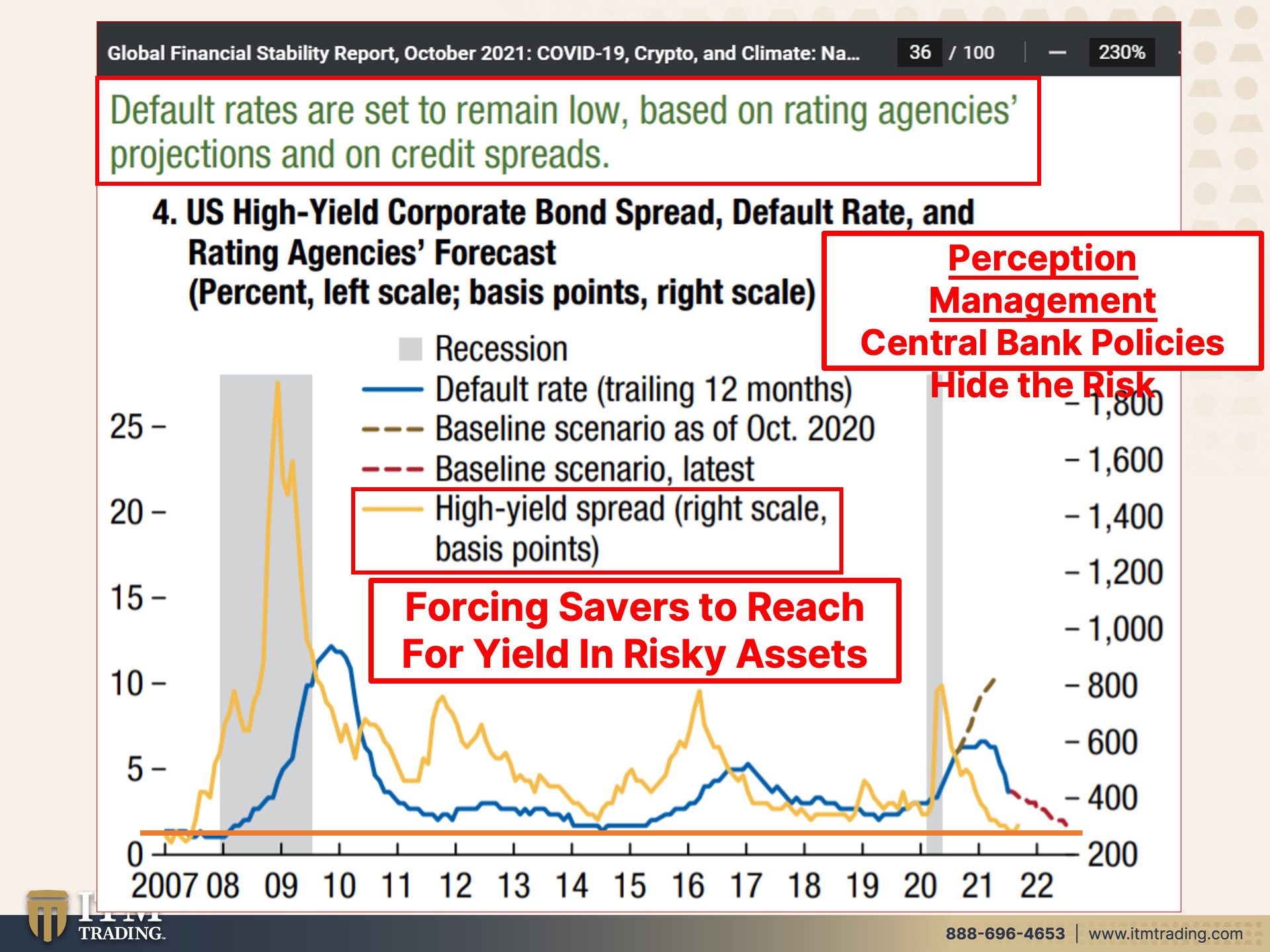

But in the meantime, do they really want you to know or understand what’s going on? No, they don’t. Because if you really understood that the currency was going away, that this little thing, whether it’s a digit in your account, or whether you hold it in your wallet, it has no value. It seriously has no value. So they create policies really as much to hide the risk, because what do they always talk about is expectations, inflation expectations, right? As long as the public is moving forward, perception management are tools that help the public move forward in a way that supports central bank policies. So let’s take a look at some of those. And we’ve talked about this before, but this is in the report. It’s absolutely true. And I want to talk about it more with you. Default rates are set to remain low based on rating agencies, projections, and on credit spreads. So let’s break that down. The rating agencies like Moody’s, SMP what we know because they have admitted it. And we’ve talked about it is that they have made conditions for their grading all whole lot looser and easier than they really should be or were. And that’s why we’ve had that huge growth in triple B, which is that one level above junk. When a lot of the issuers in that triple B range should be junk just to paste upon the standard parameters that Moody’s and SMP usually or has in the past. I mean, look, we see this before every crisis, the grading agencies that are paid by those that issue, the debt, right? They have a vested interest in giving them the best possible score, or they’re going to go someplace else to a different grading agency to get the score that they want. So we, so can you really believe or trust the rating agencies? No, you can’t. Could you in 2007? No, you couldn’t. Can you in 2021? No, you can’t. But the market’s still relies on that and therefore they pay less, they have lower interest rates. Now, here, they’re talking about and by the way, as long as their investment quality, then these bonds, these debt issuances can be held in certain products like pension and retirement products that if it was junk category, they couldn’t by law because it’s in their prospects. They couldn’t by law hold. So there are lots of reasons for that. I’ve done other videos on that, but you can’t. The bottom line is you can’t trust the rating agencies, rating projections, you can’t, and on credit spreads in other words, the difference that you’re in interest that you’re going to pay on a junk bond versus an investment quality bond. You’re not getting paid to take the risk. So here is that okay. Here is the high yield spread right here. It is basically at the lowest that it’s been since. So I don’t know one was up oh, 2007. Oh my goodness. Do you believe that these corporations are not so risky? Well, don’t believe it don’t believe it because it’s a lie and it’s a lie to hold your wealth in there so that when it erupts and you see interest rates rise, well, what do we know about interest rates? All right. As a reminder, this is interest rates. This is principal value. When interest rates go up, look what happens to the principal value of the bond. Now, if you’re in a mutual fund, maybe that’s hidden from you. Maybe even the defaults are hidden from you. But when this happens on a large scale, it won’t be hidden from you anymore, but there’s not going to be anything you can do about it either. It’s going to be too late. You know, I mean, look at, look at how rapidly you see these yields rise. You can’t move that fast. And I’ve heard too many stories of what happens to people that call their brokers, their stockbrokers, and they want to sell, are they, oh, they’re out to lunch or the run vacation. I mean, when I was a stockbroker, you never heard of that. Somebody wanted to place a buy or sell order. You did it lickety split. And if I wasn’t there, I had an assistant that did it look at his split. And if she wasn’t there or he wasn’t there for some reason, there was always a manager. There was never any good excuse for you, not executing a trade immediately. But I hear that all the time, these days it’s really quite disgusting, but central bank policies of low interest rates have forced savers. And those that need that income out on the risk spectrum and push those yields down too. So you are not not getting paid now. I’ve also heard a lot of people say, well, but I use that for income. And I’m kind of digressing here a little bit. However, what you need to understand is that you’re risking your principal for that. itty bitty teeny weeny bit of income. There’s a strategy to overcome that. If you talk to one of our consultants, they’ll explain it to you. Okay?

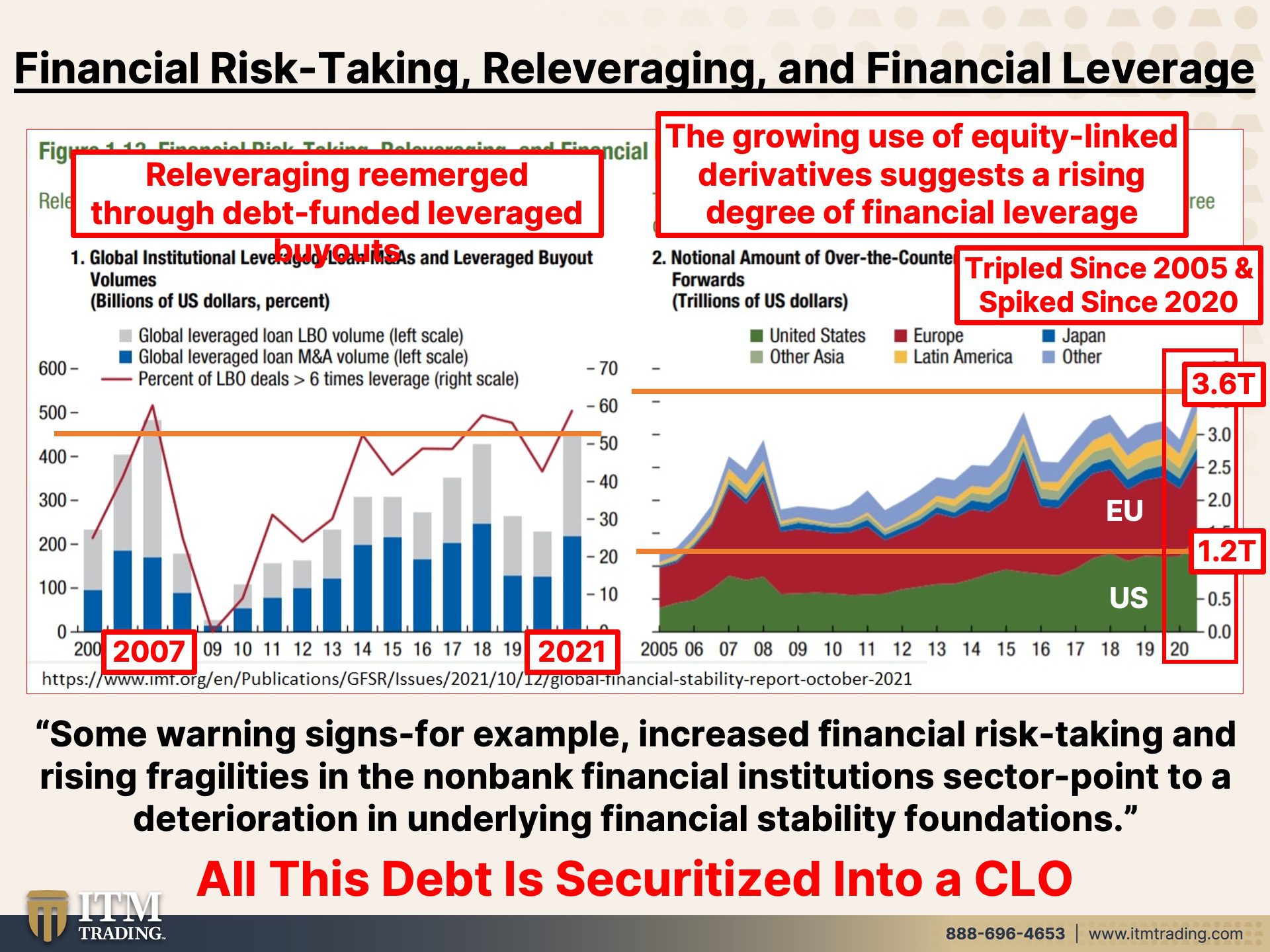

So then they get into financial risk taking re-leveraging and financial leverage. Let’s take a look at that okay? So this graph goes back to 2005, both of these do all right, but look at 2009. So really leveraging reemerge through debt funded, leveraged buyouts. The cost of debt is virtually zero. Why not take on as much debt as you can. This is all the leverage in the system. Now there are advantages to leverage, but only if you have the ability to boom, pay that off immediately, if you needed to. And that’s also part of the strategy. Leverage can kill you in a deflationary environment, kill ya. Okay. And that’s exactly what I think is going to happen because we have those leverage and really leveraging rates at the highest that they’ve been since. Oh, look at that 2007. Well, hindsight is great. Do we know what happened after that? Yeah. The, the great financial crisis, that’s still isn’t over. This is really the end of that because the system died in 2008, but also the growing use of equity linked derivative suggests a rising degree of financial leverage. Now he liked this. It suggests that which means they have no clue. Do you really want to trust an entity that really frankly has no clue about how deep this risk is? Because frankly from 2005, it’s tripled, tripled, and in 2020, actually starting in 2019, it spiked to the highest level ever, ever, ever. Yeah. That should make you feel really safe. I really comfortable that everything is hunky Dory. Like the interest rates would imply, no, that’s all manufactured and it’s all designed to get you to go in the direction they want you to go in. So back to that, on that first piece, some warning signs, for example, increased financial risk taking and rising fragilities in the non-bank financial institution sector point to a deterioration in underlying financial stability foundations. Well, now mind you, they did not put that quote with these graphs because they don’t want anybody to connect those dots, but it’s pretty obvious what they’re talking about because then what they do on top of it to create even more leverage, more debt, more risk is they turn all of this garbage into financial products and sell them back to you for your retirement. And they’re not getting paid for the risk that you’re taking.

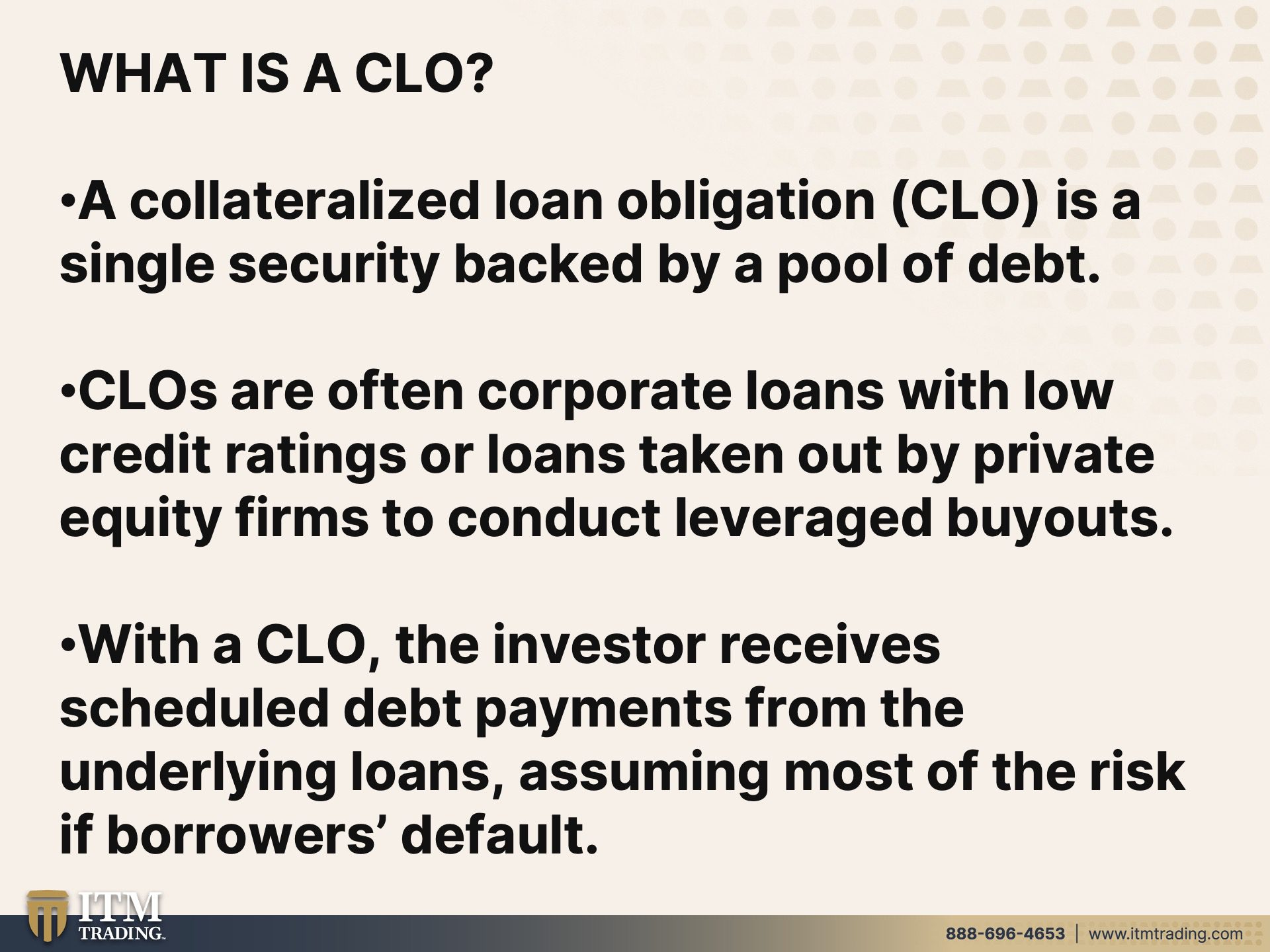

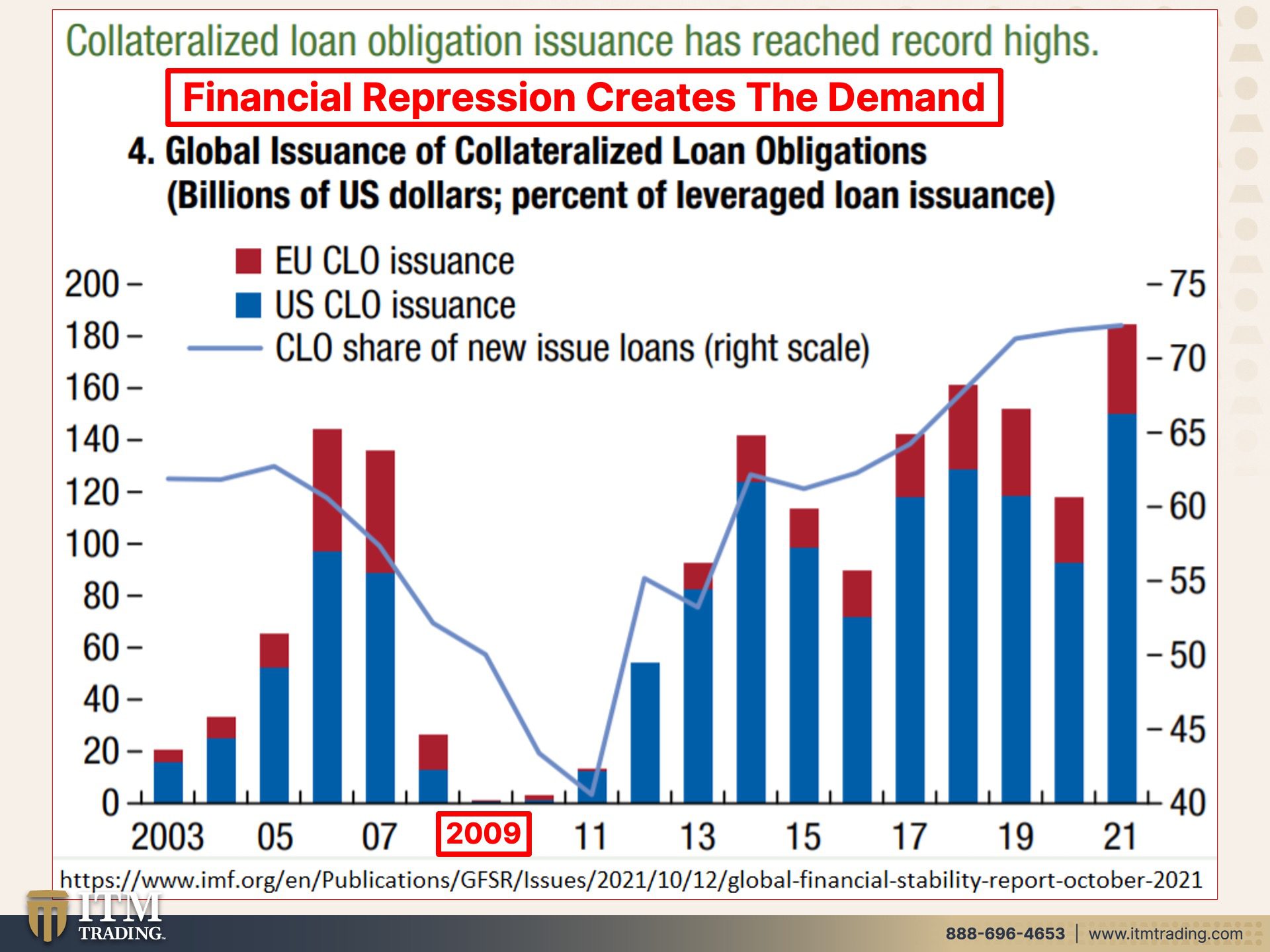

Now. It was a CDO that, that the freezing of it created the financial crisis in 2008. This is a CLO. The difference between the two is the CDO was based on mortgages. And this is based on debt, corporate debt, a collateralized loan obligation as a single security backed by a pool of debt. So all that debt that you saw put into a big, huge pool they’re offering corporate loans with low credit ratings or loans taken out by private equity firms to conduct leveraged buyouts, to take on more debt. So there are loans taken out to take on even more debt. Okay. That sounds great to me, with a CLO, the investor receives scheduled debt payments from the underlying loans. Assuming most of the risk, if borrowers default, let’s see. So wall street benefits because they’re making all these fees from giving the loans to begin with. I mean, we can look at that here. Let me go back so you can look at it again. Okay. So they make money on all of these debt, issuances, all of them, right? Then they put them into a pretty package and they sell them to you. And now we are at record levels. What could go wrong? You see why the central banks cannot raise interest rates. They’re going to try, do you see why the central banks cannot run off their balance sheet from buying all of this garbage? They’re going to try Australia, tried to control the interest rates and they had a big fat fail. This is going to be a big fat fail globally. I mean, I can’t guarantee it, but I’m a hundred percent certain. There’s not, one doubt in my mind about what we’re going to see. So here was the CLO issuance in 2006-07. It was in 2009. Just keep that in mind because the central bank policies, we’re all about financial repression. I just did a video recently. So, because it’s really important that you understand that central banks have used financial repression to create demand in the markets and they’ve been doing it forever, but they’ve specifically been doing it since the 40s, really, without a break, without a break. And that’s what they, that’s how they do it, you know, oh, I need more income. So you’re not looking at the risk, especially when the risk is being hidden by grading agencies and by the yield curve, because they’re artificially suppressing that. So people just go, oh yeah, I’d rather get 5% than 2%. But the level of risk that you’re taking, actually even on the 2% is huge. It’s just all in the training. I’m so grateful that I was a stock broker, I’m telling you, and a banker. I’m so grateful that I had those experiences so I could share my experiences with you.

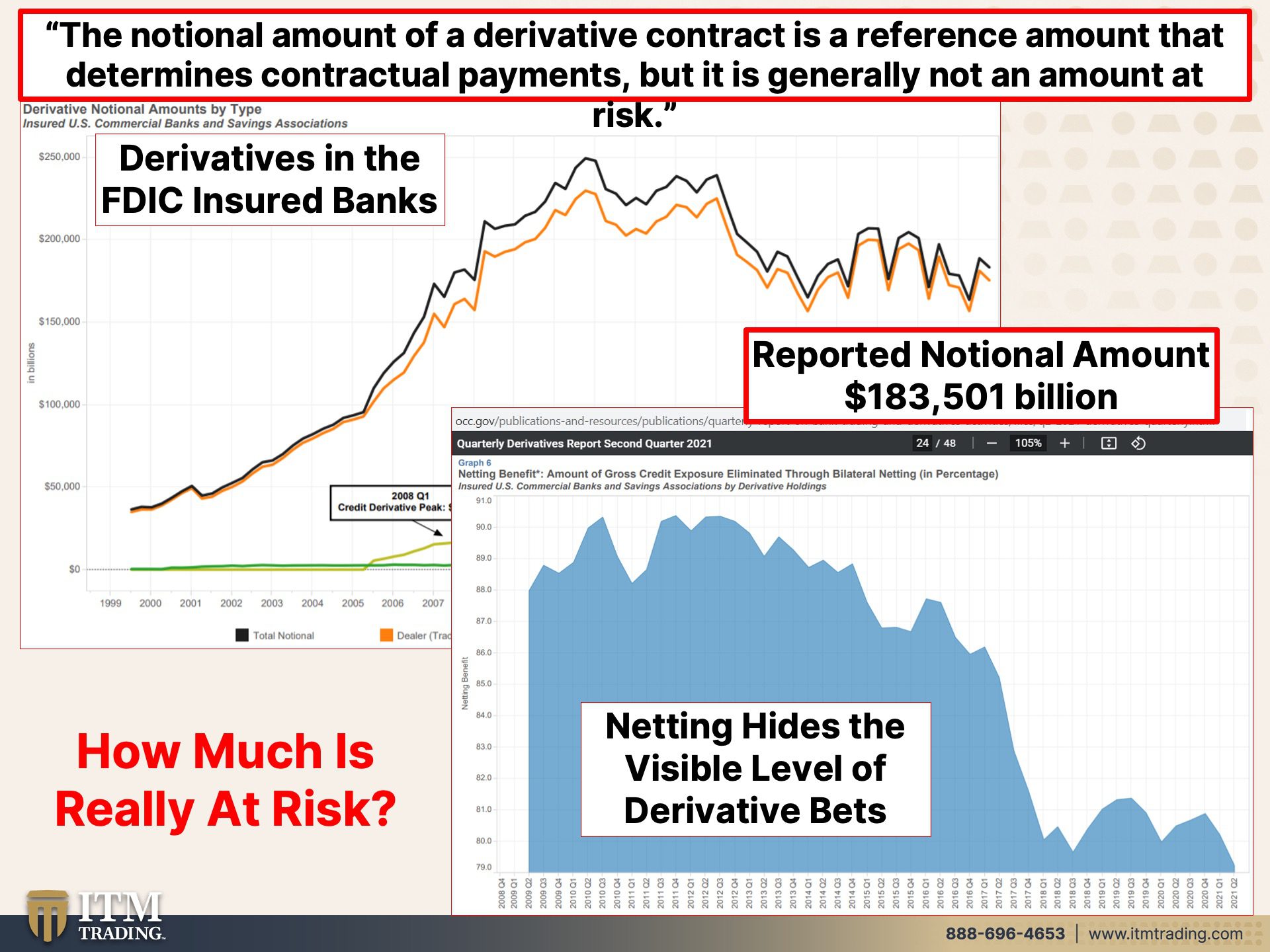

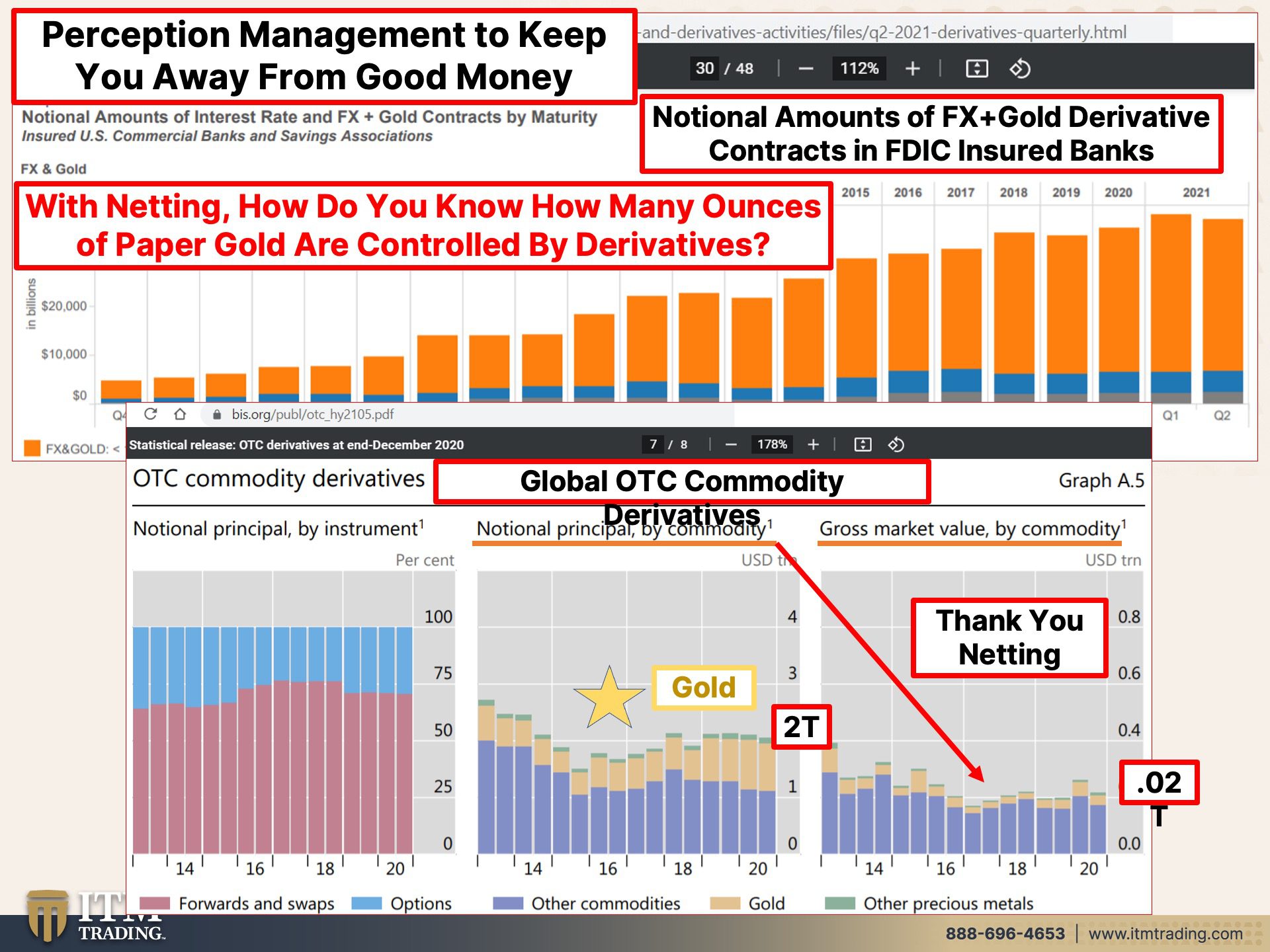

So this supported, because they’re really talking about derivatives and derivatives are something that will a hundred percent take this system down. So this is the most current Q2 report from the office of the comptroller of the currency. And as always, all of the links are available on our blogs. Okay? So these are the levels of derivatives in the FDIC insured U.S. Banks. This is not global. I’m going to show you that too. This is just in the U.S. in the FDIC insured banks, which they really, if all the banks go down at one time, there’s not enough money to cover it. Okay. Now they’re reporting a notional value of 183, almost 184 billion if I was going to round up. Okay. So, all right. Maybe that’s not horrible, except for the problem that whenever you hear nominal or notional, what you should immediately just know is that you’re not really going to know the risk or the level involved. So then, and this is from that report from the OCC report, the notional amount of a derivative contract is a reference amount that determines contractual payments, but it is generally not an amount of risk. Nobody really knows the amount at risk and the admittedly, they all say the same thing. And in 2013, rather than changing behavior, what they did was they created formulas to make it look like there were doing fewer derivatives, even though that’s not. So, and you can see, this is the netting benefit. So how much in notional value really is reported? Well, we know what they’ve reported rather, but how much is really floating out there? Nobody knows. Nobody knows. Well, that should make you sleep really well at night. This frankly is what will keep me up at night, because I know this. Netting hides the visible level. It doesn’t change the risk, what they’re saying is well if you have this derivative over here and somebody has an opposite derivative over there, they cancel each other out. Yeah, they do until they don’t. They do until they don’t. So we are really flying blind on this. And it’s not just you and me that are flying blind. It’s really the central banks, the governments, even the banks and the entities that create these derivatives. Everybody is flying blind by choice. And as long as the printing presses can roll, they can keep it floating. But the reality is, is nobody knows, but it’s a lot. I will tell you.

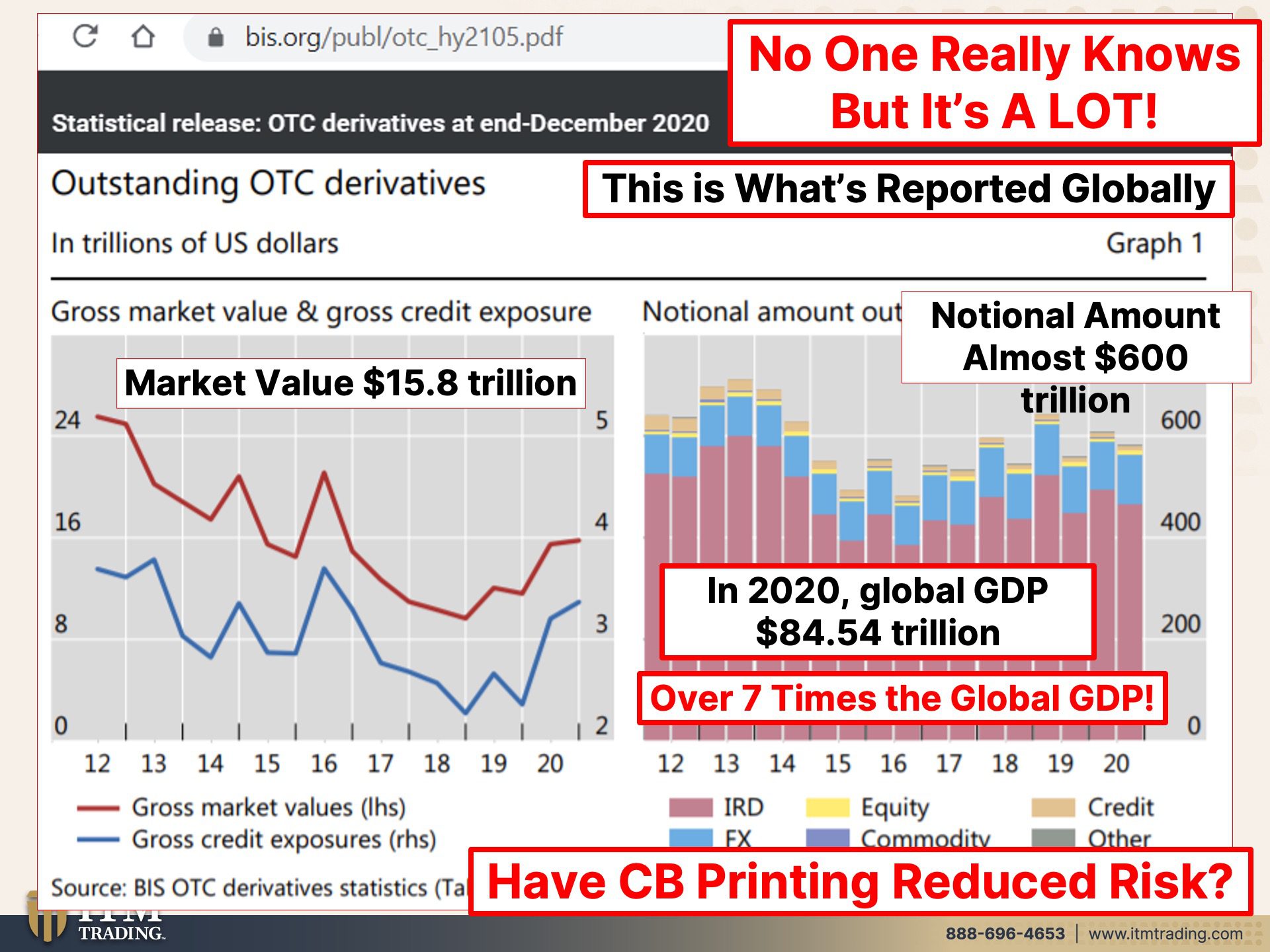

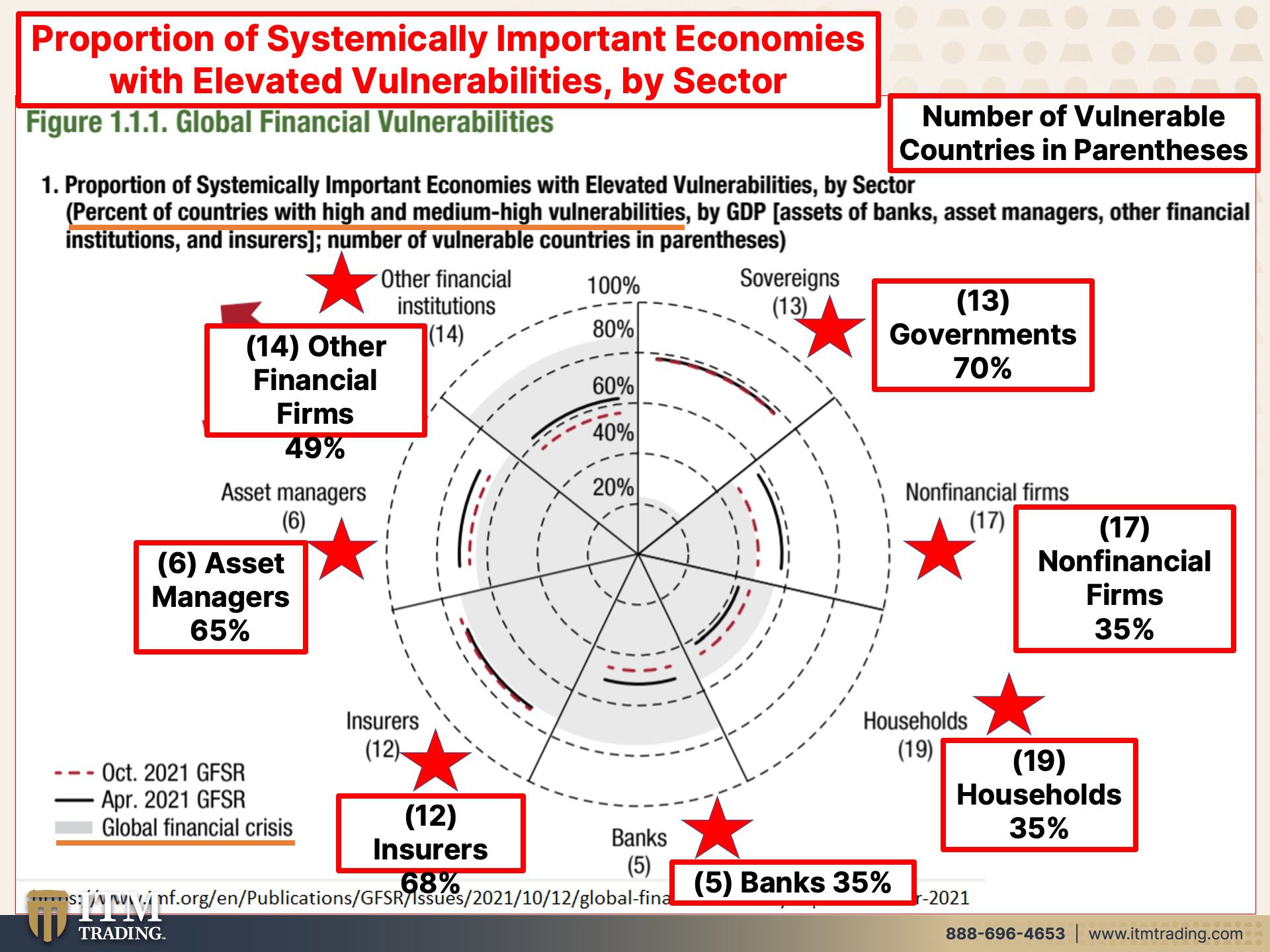

So this is from the bank for international settlements report on derivatives and it goes through December, 2020. Okay. And it is in trillions of dollars, which we throw around. Like, that’s nothing, but I mean, you know, put that in perspective. So what they’re admitting to reporting to is a total of 600 trillion in notional value. How much is at risk? I don’t know, but what I can tell you is before they changed the accounting rules of the bank for international settlements reported, And I, I totaled this up myself from their reports, 1.49 quadrillion in risk 1.4 quadrillion. So I don’t know how much is really at risk, a lot more than 600 trillion. And yet thanks to netting and thanks to financial innovation, the market value of those contracts from 600 trillion in notional contracts, take it down to 15.8 trillion. Yeah. If you believe it, I have a bridge in Brooklyn that I’d like to sell you. I don’t believe it, but here’s the kicker. The global GDP is 84.5, 4 trillion. So, you know, if you’ve got notional amounts at 600 trillion, that still isn’t telling you how much is really at risk underneath that, just what they’re admitting to is over seven times, the global GDP. Can you tell me how in the world you can print that out where you can, or you can wallpaper over it. Like they didn’t do thousand and eight, which was harder for them to do that’s the first time they had to do it in 98 with long-term capital management, third, time’s a charm. How about third time can take down the system? They can’t bail it out, but it would justify a new system wouldn’t it absolutely will justify it. So has any of this that I’ve shown you and all of the central bank printing and money creation and interest rates at zero and all their shenanigans, has it reduced the risk according to them? I mean, according to me, no, it has not, but this is also in the report and here are the vulnerabilities. Now, first of all, what they’re showing you is the proportion of systemically important economies with elevated vulnerabilities and the percent of countries with high and medium high vulnerabilities by GDP. So they are looking at the most advanced economies first. Okay. And it’s all done by GDP. Now, they’re also letting you know, in these parentheses, the number of countries that according to all their parameters are vulnerable. And then finally, any of this gray area represents the risk to these different entities, these different sectors during 2020s financial crisis. All right. So now let me show you this. All right. So here you go. Now here is, I think this is like super interesting, really, when you look at this stuff and you go, wow, that is really interesting, but you’ve really got to study it to fully benefit from what they’re trying to show you here. So sovereign, which our governments were not very vulnerable. According to this, they were at like a 20% vulnerability or 10% vulnerability level. And guess what? They are now elevated up to like a 70% vulnerability level, 13 governments, their vulnerability level has grown exponentially. Why? We’ll come back to that. We’ll come back to that. I’m going to show you why. Here are those regular corporations that are not financial and 17 of those. All right. Well, here’s their vulnerability during the crisis here. So they’ve elevated vulnerability since the crisis, even with all of the bailouts, even with all of the new debt for free and, and the central banks buying corporate bonds and all that garbage, they still have an all of elevated vulnerability today, which I think is very interesting households. Well now the household vulnerability has improved. Right. That’s gone down. Okay. All right. That’s that’s good. That’s good. Well, we’ll talk more about that. There are banks. Oh, so too, banks were very vulnerable, like 70, 80% vulnerable, but their vulnerability has also fallen and 35% of the banks. So five banks, are systemically important banks, by the way, are still very, very vulnerable and insurers. So many times I hear, but it’s insured. But look on your insurance contracts, your annuity contracts. It says it’s based upon the claims paying ability of the company. And what they’re showing you here is that the insurers are at least as vulnerable 12 insurers. And, you know, look, we don’t really have a lot of choices. It’s always just a small group of entities that basically control a whole entire area. So 68% of the insurers are as vulnerable today as they were when the crisis hit. So, Hmm, I guess that didn’t help very much asset managers. Now, asset managers are those entities that invest your money for your retirement or for if you’re trying to save or whatever. So six asset managers, and I got news for you. There’s not a gazillion of them. 65% of them are more vulnerable today than they were during the crisis, more vulnerable. And then lastly, other financial institutions, which they didn’t really give me a definition, but it would be things like FinTech, etcetera. Non-Bank, shadow banks that are financial firms may be, they, you know, I mean, we see that most of the mortgages are generated not in the banking entity, but by non-banks. So you can see that they’re not as vulnerable as they were during the crisis, but there’s still 49% of them are vulnerable. Now here’s the pattern. Those that got all of that easy money. So those financial institutions, the banks, and even the households that have increased their savings, they’re less vulnerable, but that’s not really true. And the reason why I’m saying that that’s not really true is because whenever a government spends your money or spends money, they’re spending your money. So they have transferred the risk really from these private entities here, primarily. I mean, look, it, this is just a little bit, households are just a little bit better, but banks and other financial institutions have fared much, much better than the households have. So I think it’s really interesting that those entities that directly benefited from all of the federal reserves, monetary programs are showing up here as less vulnerable, but the sovereigns are off the charts. Look at this, they’re off the charts. This is how vulnerable they were before. This is how vulnerable they are. Now. A lot of that has to do with all of the debt that they’ve taken on and the choices that they’ve made, we are very vulnerable because even where it’s showing it’s not as vulnerable, it’s not true. It’s not true because of everything that I’ve just shown you. Okay. In the same time, perception management wants to keep you away from good money, from real money that can protect you. They want you to hold your wealth inside of the system that they are attempting to control, and they can control it until they can’t. And I know that’s not really a very good answer because we want things that are more definitive. But the reality is as long as the general public has confidence in their abilities, they can continue to do it. But we are so vulnerable. That one little change can topple the whole Jenga economy. So when that happens, what do you need? You need physical gold. You need physical silver. That is de-centralized and outside of the system, but they don’t want you to do that.

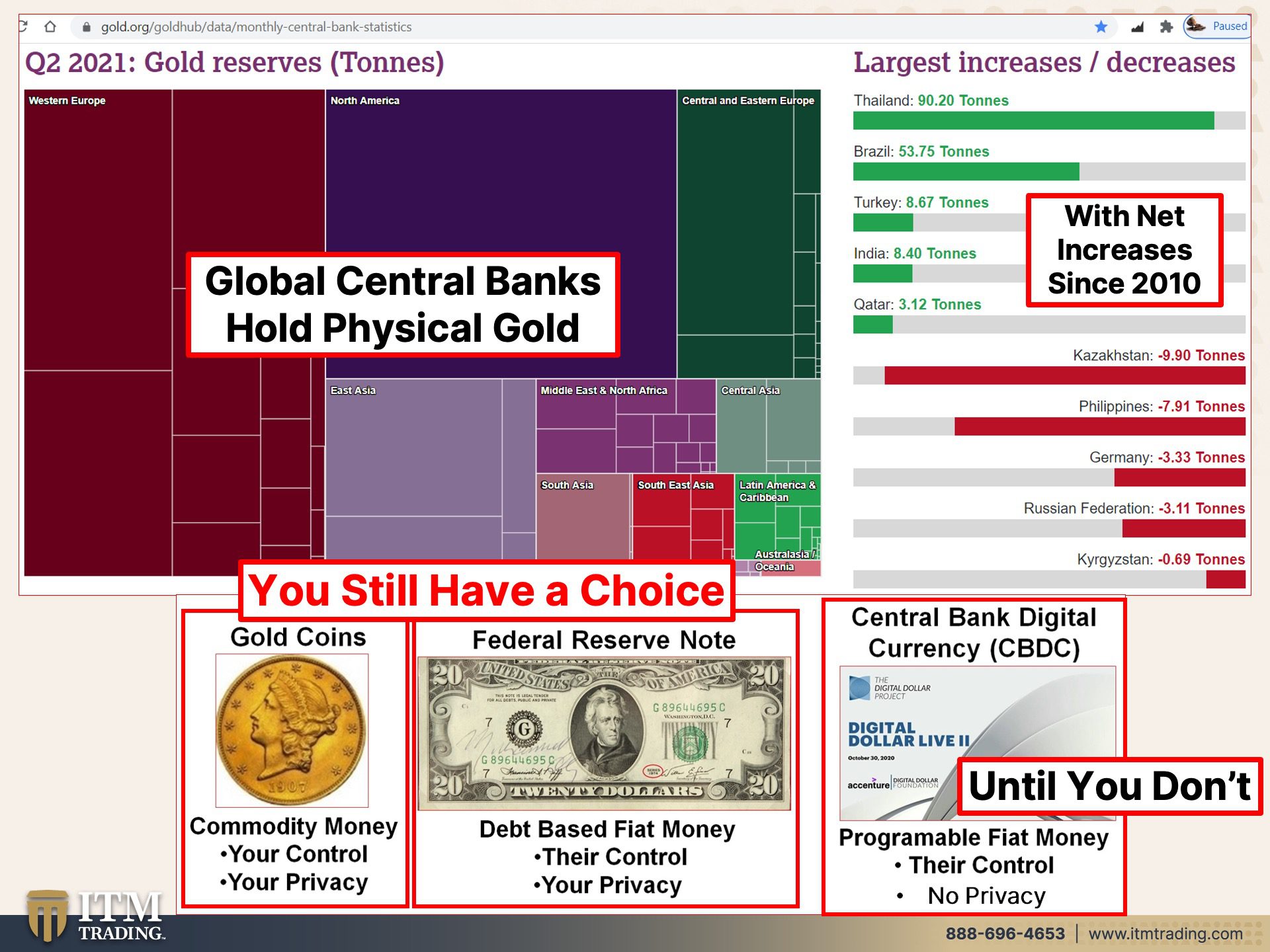

So they would rather have intangible wealth exploding, nominal value while the value of the dollar or any Fiat currency goes down. So this is also from the OCC’s report on derivatives, in the USFDIC in short banking system. And this is the, these are the gold derivatives. And you can see how they have grown. And here’s 2021 right here. Okay. So it’s all manipulation because when you do a derivative, you know, first of all, you cannot convert it into the underlying asset. And second of all, you can make it appear like there’s a whole lot more than there really ever is, but less you think that it’s just in the U.S. Oh no, no, no, no. Let’s look at the BIS report on the, over the counter derivatives. And in specifically, I’m going to look at the notional principal by commodity and here’s gold. Okay. So they did make gold golden. And I would like to point out to you that you can see that those globally, the derivatives against gold have grown as well. So this is the short term battle because a rise in gold price is an indication of a failing currency. They don’t want you to know that this garbage is dying. They don’t want you to know that. So what they do is they make the stock markets and even the crypto markets, let them go up because those are all intangibles, but let us suppress gold and silver, let us suppress real money so that you don’t go there. I mean, it makes it easier for them. Well, in the meantime, what I’d also like you to see is that they’re saying that there’s 2 trillion in notional value. So nobody really knows how much is really at risk, but 2 trillion, but thanks to financial engineering and netting, what does it show up as 0.02 trillion substantially lower. Wow, thank you netting. See how handy it is to have the ability to create the rules as you go along. And when things don’t happen the way you want them to happen, just change the rules, don’t change the behavior. Well, let me tell you, I think we all need to take a really hard look at ourselves. And if you are counting on the Fiat markets to save you from this collapse, well, you know, maybe you need to rethink that because they don’t have your best interest at heart. Gold and Silver has your best interest at heart because you hold it and you own it outright, all this other stuff, they’re just contracts. That’s what they are. Contracts. Could you actually tell me how many ounces of gold they are suppressing or they have created just by all of this derivative garbage and all of this netting. No. And they couldn’t tell you either, but in the meantime, central banks are accumulating gold, gee! Physical, real physical gold in their vaults because they are very clear on what they’re doing to this garbage. And they don’t even want you to have this garbage. They’re very clear audit. They have been net buyers since 2010, but interestingly enough, and I don’t have that chart up here today. I show it a lot. But you know, interestingly enough, if you look at the long-term chart on central banks and their gold buying, they really started buying back in I think it was 2006 or 2005. That’s when you saw bottom and then an increase, she had fewer central banks selling and more central banks buying and by 2010. It was all net. Because even here you can see, these are the sales, you know, 0.9 tons. See, here’s a big one, the Philippines 7.91 tons. I mean, that’s the biggest one. But up here, you’re looking at Thailand buying 90.2 tons and Brazil buying 53.75 tons and Turkey, even buying 8.67 tons. And what do we know about these countries? And what do we know about all the countries in the world? We’re all vulnerable. This debt mountain is going to explode on us because all of that garbage has been turned into big derivative bets. That’s really what you need to know about, about derivatives. More than anything. They are huge leverage bets. That’s all they are. They are bets. I would not want to plan my financial future on a big bet, because this is how they’ve, you know, I mean, you can see same thing right here. When we had good money, the gold coins, they were in your control. If you did not like what governments were doing, you simply went to the bank and you converted this $20 gold certificate into this one ounce of gold. And since you know, it’s not centrally cleared. It’s decentralized, you hold it. You own it. You have full privacy. And then of course, they went to this, the federal reserve note. And by the way, federal reserve note right up across the top, a note is a debt instrument. And it’s owned by the federal reserve. You’re just borrowing this, right? You don’t own this. And it’s in their control, but typically takes like an average of 18 months between policy until they know whether or not it worked the way they wanted it to work. But at least if I have this in my possession, I still have privacy. Today, you still have a choice. I don’t know how long you’re going to be able to retain that choice. But this is not the time for any procrastination, because this is the direction that we’re going in. Their control. No privacy, programmable money. No, no, no. That is not what I want. Now, mind you, look, if we end up there and I’m sure we will, everybody’s going to have to use it including me, because that’s going to be our tool of barter. But I tell you originally in my strategy, I thought, well, I would convert more of this, especially if it’s my asset protection gold into the new currency once I was certain. and it’s easy to tell, I’ll tell you how I know when this whole game is over. When they back it with gold, then it’s over. Okay. So just when we go into a CBDC that transition. No, no, no. That gives them direct control to destroy the value of what you work for and what you try and save that gives them direct control over this. This eliminates their control. So instead of, of converting a lot of it into the new currency, I’m going to convert it as needed because I don’t trust them. Do you? This I trust and is global usage. There’s always demand. I hold it. I own it. And for all intents and purposes, even though you’re sitting and seeing this here, right, it’s real. You can hear it, right. You can hear it for all intents and purposes. It’s invisible, and that’s the way at this juncture in the trend. I prefer to hold my wealth because we have a choice until we don’t. And I would always rather be two weeks too, early, 10 years, too early. I don’t really care. I would always rather be early than even one second, too late, because that one second could cost you all of your choices.

We need more than gold and silver. During this transition, we need food, water, energy, security, community, and shelter, as well as asset protection and wealth preservation. We need all of those things. So please start today because I don’t know how much longer this can go, but Australia could be a warning for us. We’ll have to keep an eye on it. All right. We may be losing choices sooner than you would think.

Now, next week, I’m going to be on with my good friend, George Gammon Rebel Capitalist channel. And you know, after the last conversation that we had and some other things that have gone on, I’m really looking forward to spending some time with him and talking to him.

But if you haven’t already, please leave us a comment, give us a thumbs up if you like this and make sure, and this one, particularly share, share, share this video. I know I’m running a little long on it, but it’s that important. And if you want to start your golden silver strategy, which I highly suggest, just click that Calendly link below, and we’ll set up a time for you to meet with one of our consultants. If the times that are available, don’t work for you. Call us. We love human contact. So just keep in mind without a doubt. It is so time to cover your assets. And here at ITM, we use the wealth shield and the wealth shield is made of metal paper and promises. That’s not going to shield you from anything. I just showed you all of the stuff that’s going on from the IMF that they’re talking about the vulnerabilities from the OCC, you know, where we think that banks are safe because after all they’re FDIC, well, I’ve done reports recently on the level of FDIC insurance too. It doesn’t mean anything. It doesn’t mean anything. And the bank for international settlements to step back and give us again with the IMF, that global view. So tomorrow I’m going to be with Q&A with Eric. If you have any questions about them, send them into questions@itmtrading.com. And until next we meet, please be safe out there. Bye-Bye.

SOURCES:

https://www.investopedia.com/terms/c/clo.asp

https://www.bis.org/publ/otc_hy2105.pdf