FDIC PLANS FOR COLLAPSE: Banks Buy Gold and Plan for Bail-Ins

In the beginning, we had gold and silver money. Then they transitioned us to a gold certificate, so you’d walk in the bank with gold and you could walk out with the gold certificate. That helped you feel like, okay, well these had some value, until they don’t. What’s coming up, is about to devastate most people and the foundation is laid, I’m gonna talk to you about the insurance and what’s really happening underneath the surface that actually puts all of your wealth at risk.

CHAPTERS:

0:00 Wealth at Risk

1:24 Deposit Reclassification

9:27 Deposit Insurance Fund Report

13:43 Leverage Debt Machine

16:08 FDIC Bankers Discuss Bail-In

23:01 Central Banks Binge on Gold

SLIDES FROM VIDEO:

TRANSCRIPT FROM VIDEO:

In the beginning, we had gold and silver money. You didn’t need any guarantees because these were the guarantees. Then they transitioned us to this, which is, this is a gold certificate, a $10 gold certificate. So you’d walk in the bank with this and you could walk out like that with that. And so that helped you feel like, okay, well these had some value until they don’t. But what’s coming up, is about to devastate most people and the foundation is laid. I’m gonna show you this and more, coming up.

I am Lynette Zang, Chief Market Analyst at ITM Trading of full service physical gold and silver dealer specializing in custom strategies. And you darn well better have one because this is now 2023. And I’m gonna talk to you about the insurance and what’s really happening underneath the surface that actually puts all of your wealth at risk.

You’ve heard the term bail-in, well you know, back in 1933, what did the government have to do? There was a bank run prior to that 29 there was a bank run and people actually got very local and were bartering because they, did not trust the banking system and the money because of all of the devaluations. Let’s just take a little trip down memory lane. So after the stock market crashed in 1929, people stopped trusting the banks, the monetary system, certainly the stock market. Their confidence was really lost. And so the government and the central bank, in order to stay into control, well they had to make some changes. Let’s listen to Roosevelt’s, an excerpt from Roosevelt’s fireside chat.

The new law allows the 12 federal reserve banks to issue additional currency on good assets and thus the banks that reopen will be able to meet every legitimate call. The new currency is being sent out by the Bureau of Engraving and printing in large volume to every part of the country. It is sound currency because it is backed by actual good assets.

So let’s think about what he just said there, right? What he was really talking about is after the confiscation of the gold in 33, those are the good assets that he’s referring to. And he’s also referring to the revaluation when he was talking about them being able to issue this money in large volumes. So he wanted to prevent a run, the run to continue, much as we saw back in March of 2020 when we had all these central bankers coming out and saying, you don’t have to worry about your cash in the bank or your money in the bank because we can just create as much as we want to. So don’t worry about it. It’s the same kind of rule book that they used to use. And by the way, I’m gonna show you this. This is the $10 gold certificate and you could walk into the bank with this and walk out of the bank with this $10 gold coin. Well I want you to take a look at the new $10 bills after that. They look very, very similar. So that’s the way they make the make these transitions. They’ll change the laws to instill that confidence and they’ll try and keep things looking as close to normal as possible so that you don’t realize that anything has changed. When in reality everything had changed. The other thing that they did was install the Glass-Steagall Act, which separated deposit taking banks from investment risk taking banks. So they wanted everybody to feel confident because after all, what created the crash in 29 was a lot of risk taking. There’s more to it, but that’s for another day. And they guaranteed deposits. That’s when the FDIC was born so that people would put their deposit in the bank trusting that they would be able to get it back out again. We’re gonna talk more about that in a while. But I think it’s really interesting that openly he was talking about the revaluation of gold to dollars, which enabled them to print so many more because after all they’re backed by good assets. Guess what guys? These are still good assets, but you know this evolution, they can’t do things overnight because then you notice things and you make different choices.

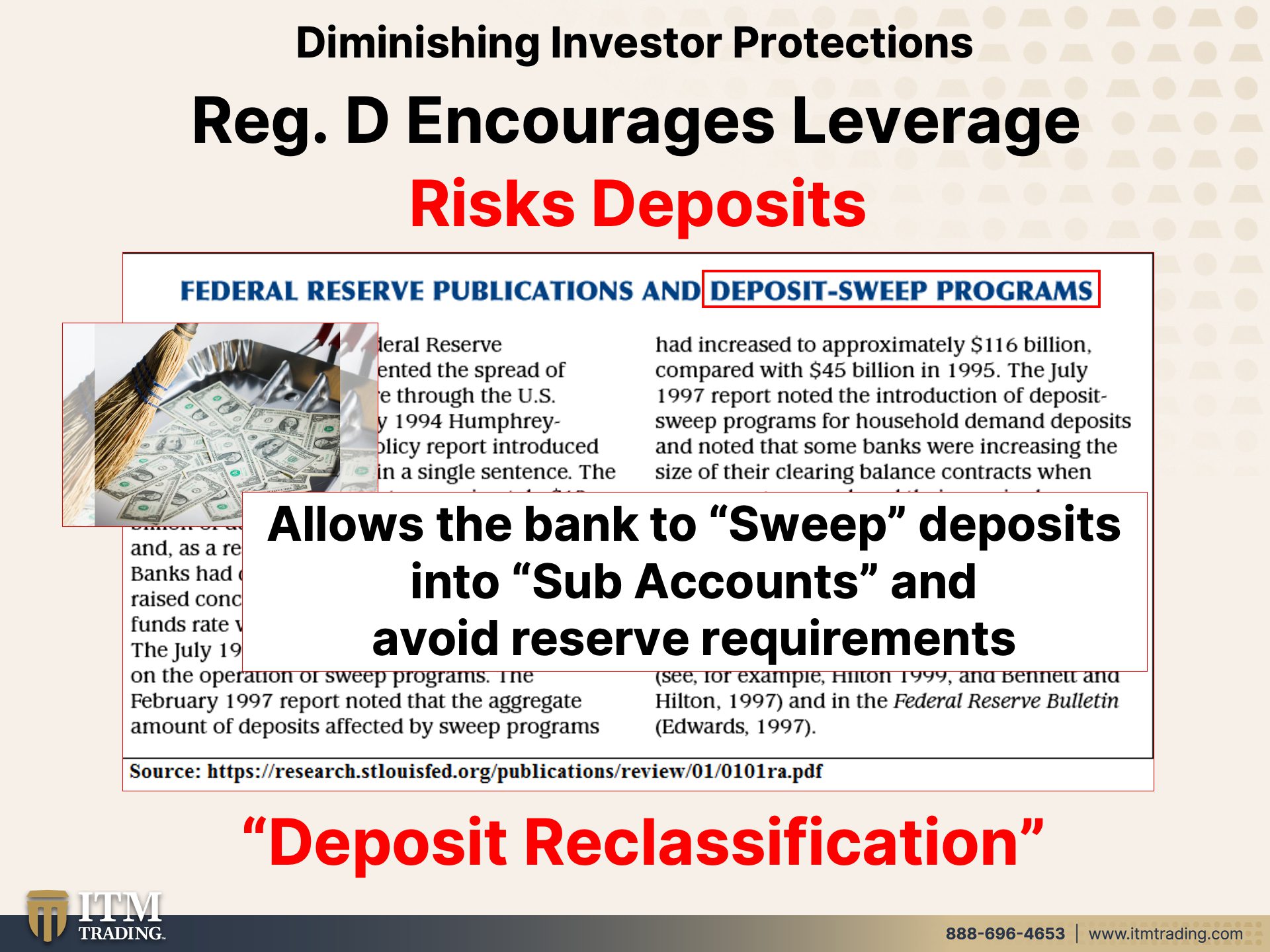

And I’ve talked about this many times in 95 they, they legalized Reg. D and that actually was about the banks having more money to work with in their speculations because when you make a deposit in a bank, it is swept into a sub-account that is in the bank’s name, not yours. And that’s how they justify where they legalize the banks using your equity for their benefit. And by the way, what’s that called? Deposit reclassification. It’s also what sets up the bail in. So you know, you may think all of this is just coincidental, but I don’t think any of it’s coincidental. I think it was very well planned.

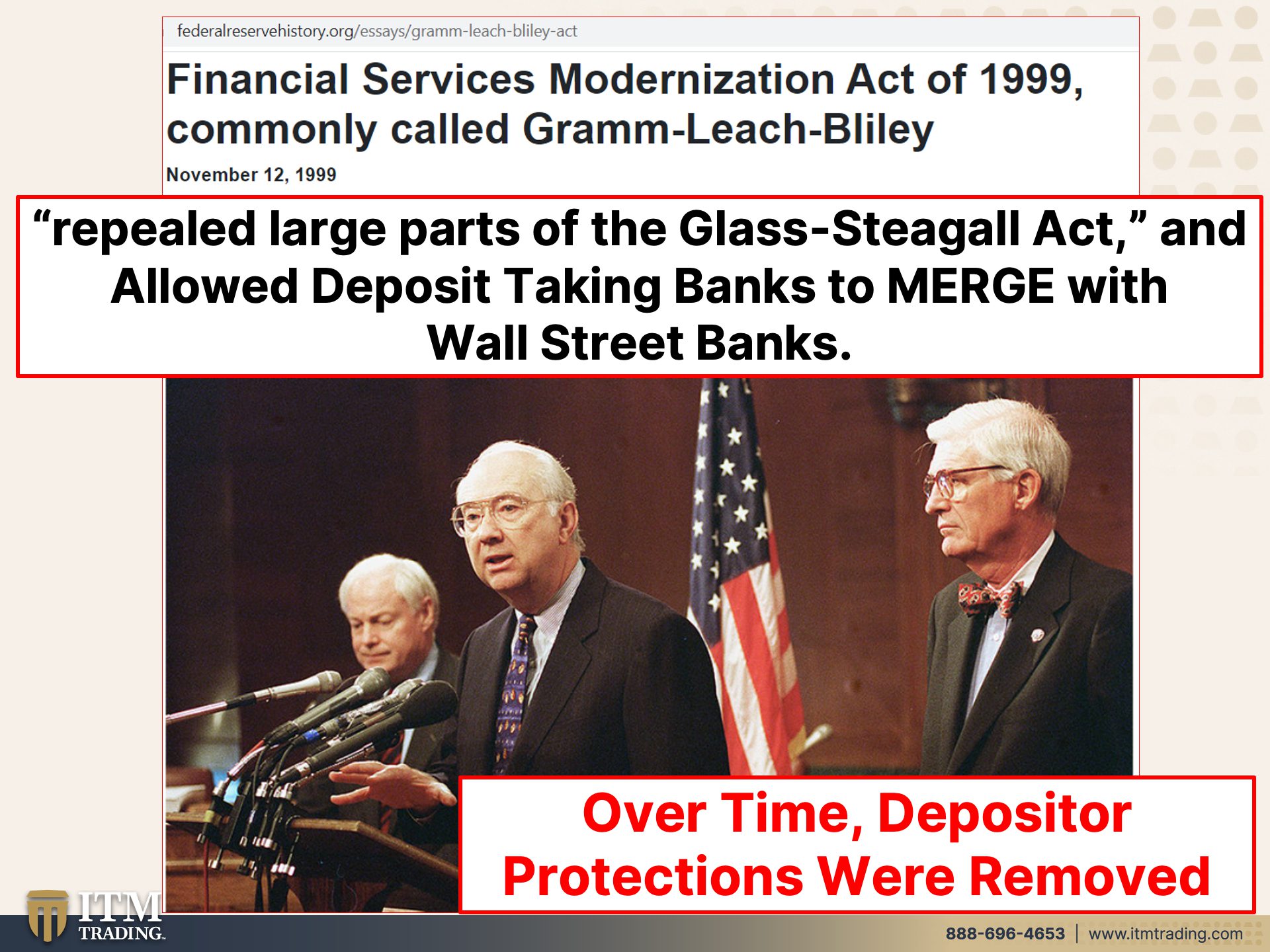

And what happened back in 99 Financial Services Modernization Act, the Gramm-Leach Bliley Act, which repealed large parts of the Glass-Steagall Act and allowed deposit taking banks to merge with Wall Street risk-taking banks, okay, that was 99 and we certainly know what happened afterwards in 2008, but has that changed? No, it’s just gotten bigger and bigger and bigger. All of these risks, we’ll talk more in a second, but over time depositor protections were removed. Not a shocker, they did it again in 2008. But this also enabled consolidation of the banking sector.

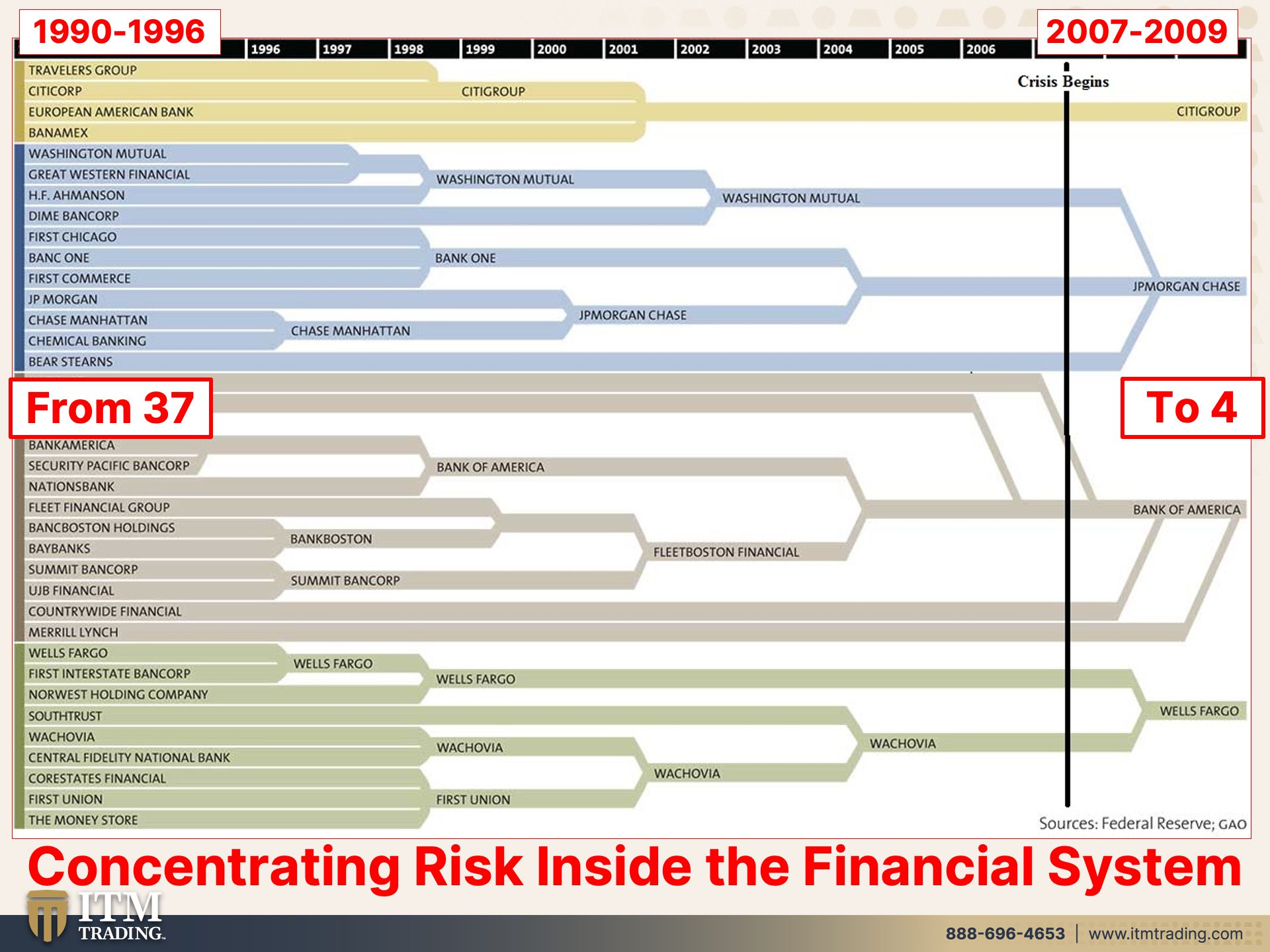

So back between 90 and 96, there were 37 banks down to four in this particular example, Citigroup, JP Morgan, bank of America and Wells Fargo.

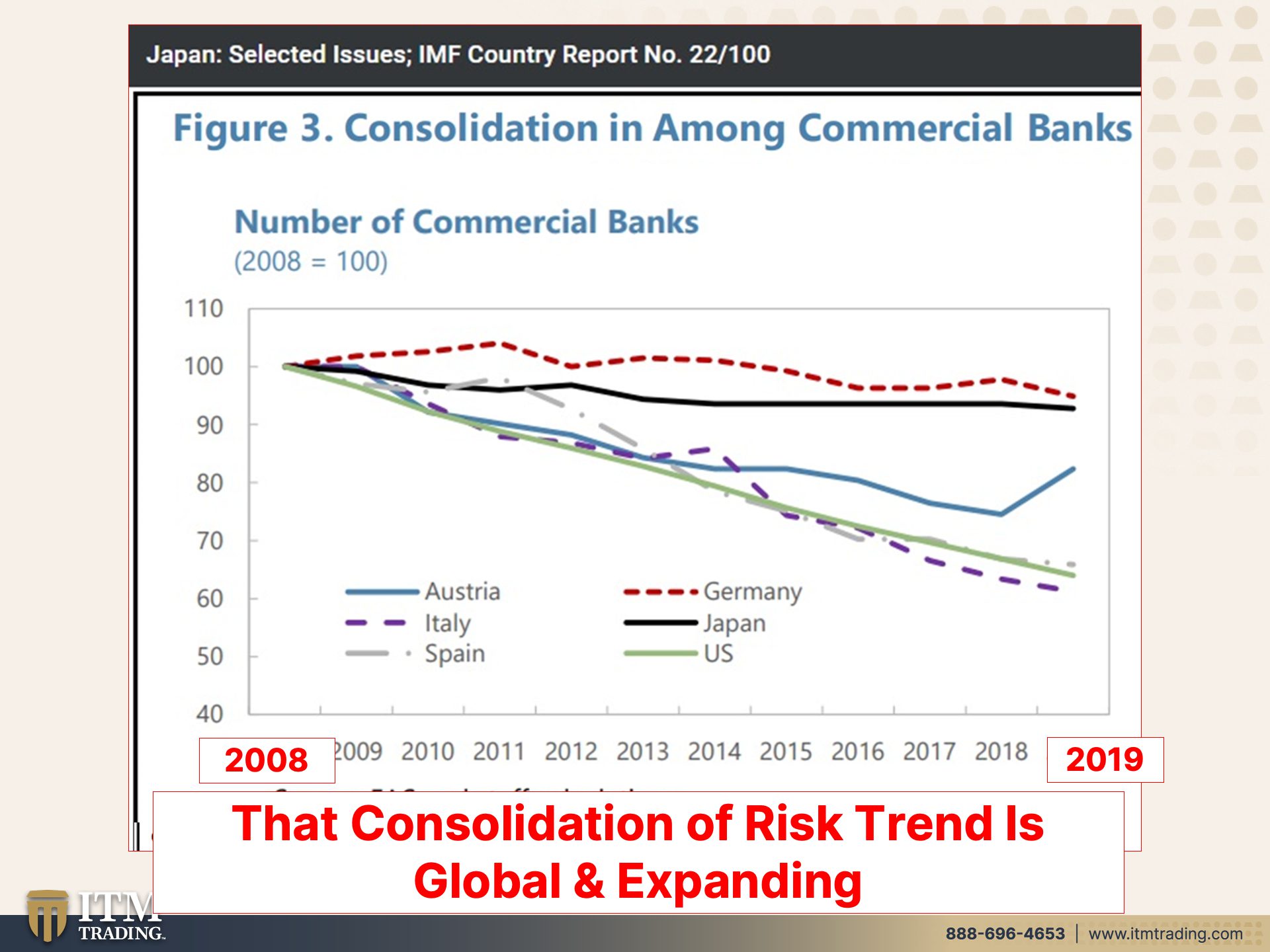

Those are the big four. And you can see how we went from a whole bunch of banks down into four. So what that really does is it concentrates the wealth and the risk inside the financial system because if one of these four go down, you’ve heard of the term too big to fail, right? Well this is 2007 to 2009. The crisis began in 2007 and that consolidation into fewer and fewer banks has continued. This is 2008 to 2019, the most current numbers, and this is Austria, Italy, Spain, Germany, Japan, and the US. Here’s the US right there, that green line. So that whole trend and of consolidation of risk is happening globally as well. It is not just a US issue, it is a global issue.

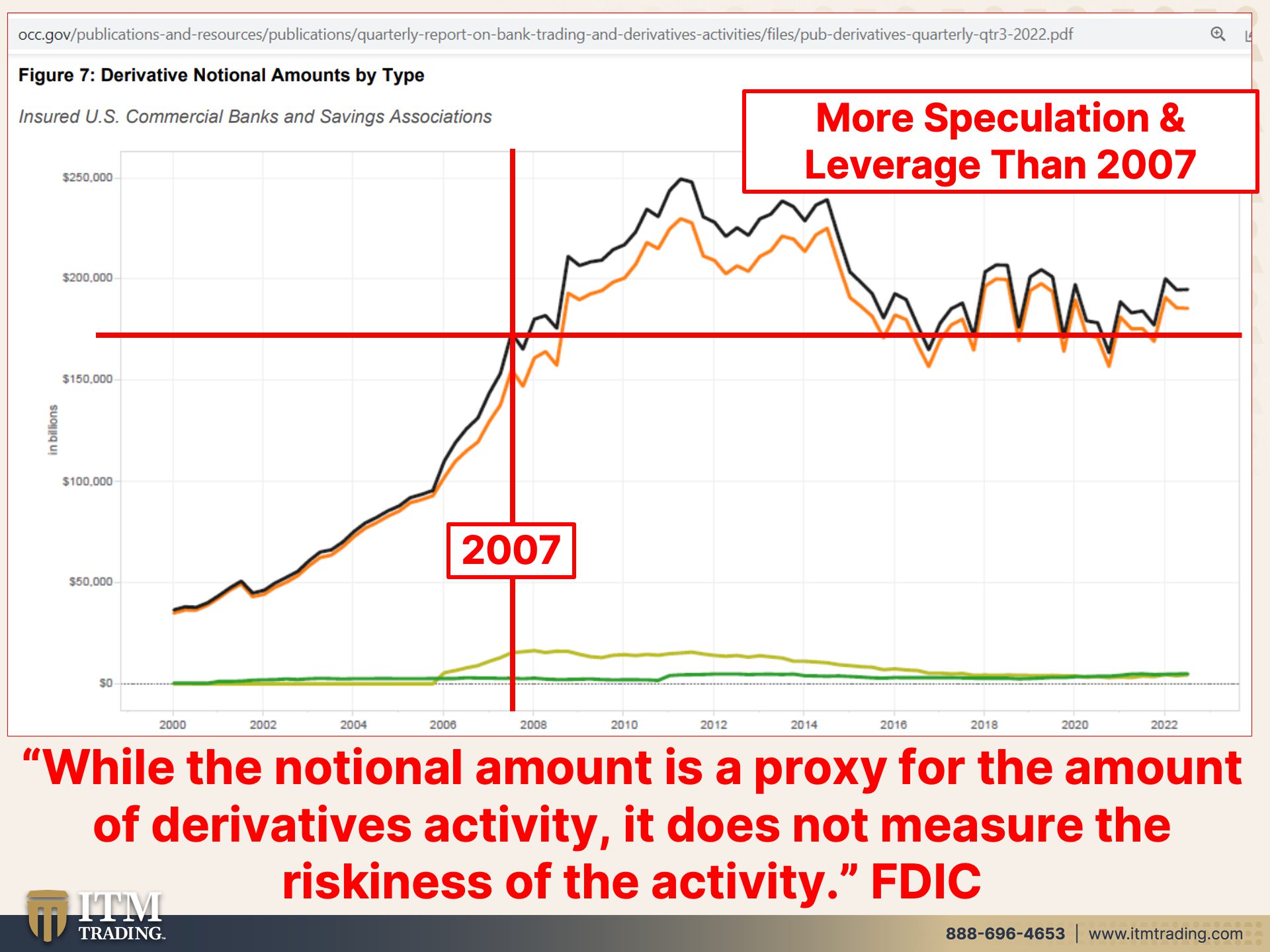

And what has their access to all of that very cheap deposit or money for their speculation? Well, you’ve seen this about a gazillion times. This goes through the third quarter of 2022. These are the most, this is the most current data that we have on this. And you can see that derivative exposure was here in 2007 when the crisis began. And it’s higher than that. And in the meantime we’ve talked about it. They have created these mathematical formulas, netting and compression to make it look smaller. So do we know how much is really at risk? Well, let’s see what the FDIC has to say about that cause what they say is, while the notional amount is a proxy for the amount of derivatives activity, it does not measure the riskiness of the activity, nor frankly the size of the activity. And just keep in mind they’re doing all of this risk behavior with your deposits legally. Legally, nobody went to jail in 2008 cause it was all legal.

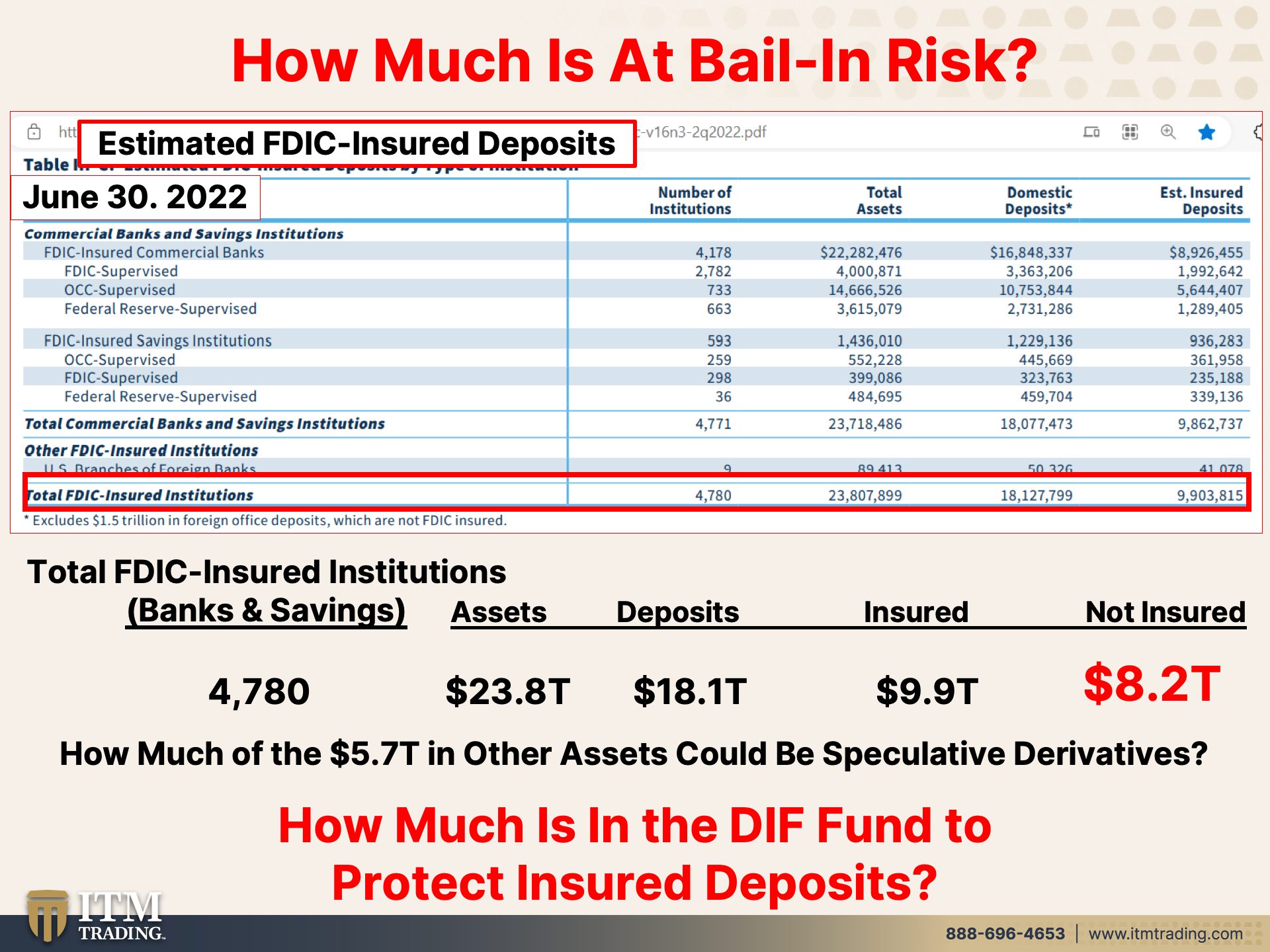

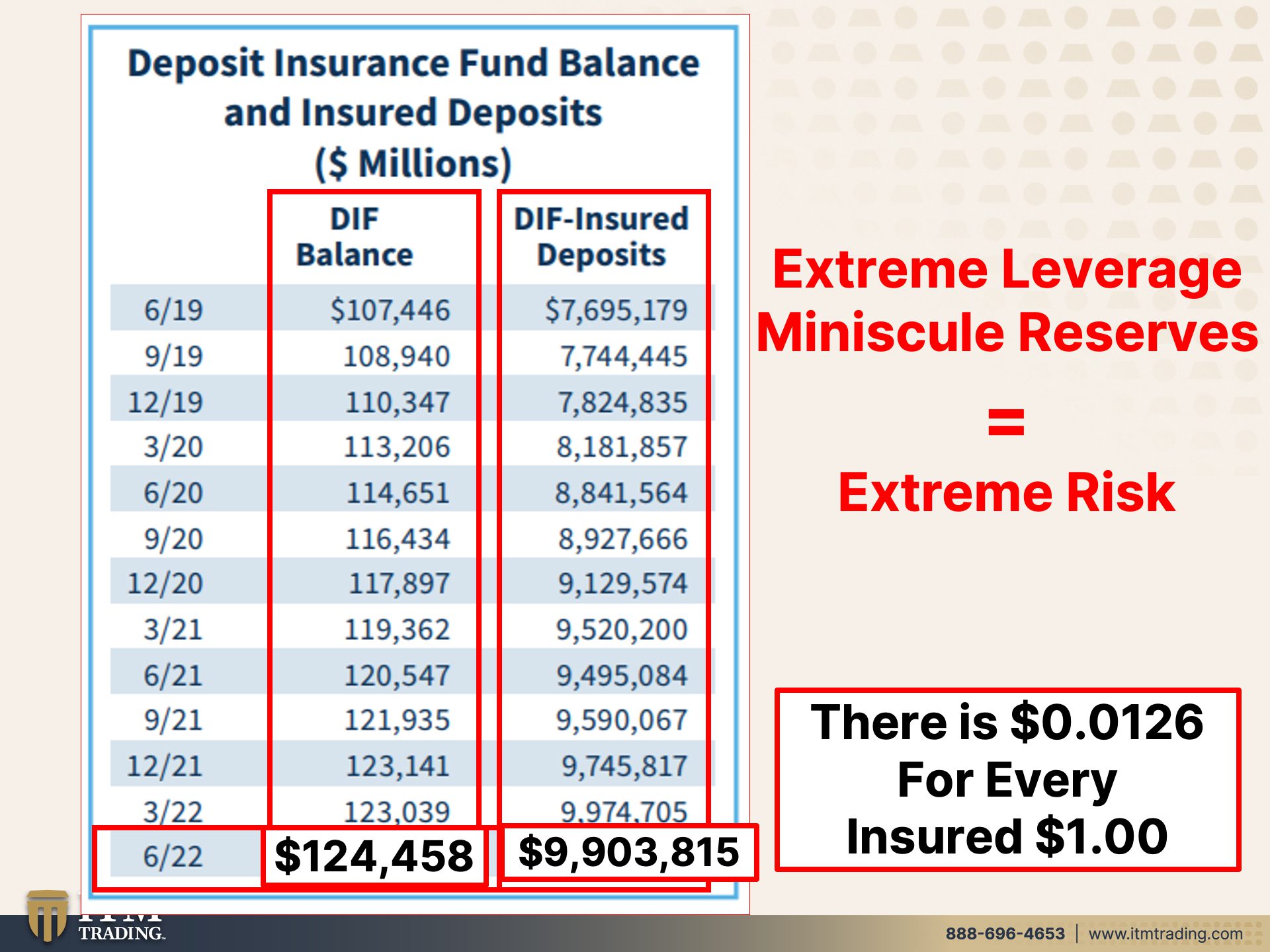

So let’s take a look at how much is at risk of bail-in. And this is the estimated FDIC insured deposits as of June, 2022. This is the most current, from the most current DIF report and remember. You’ve got links, you can listen to the whole fireside chat. You can follow all these and take a look for yourself at the FDIC’s deposit insurance fund DIF report. So this is total FDIC insured institutions. There are 4,780 of them banks and savings and loans. They have 23.8 trillion in assets. So that includes your deposits outta that 23.8, 18.1 trillion are in deposits, but only 9.9 of that 18.1 is insured. The rest of it falls above that $250,000 threshold for the insurance. So how much is it? 8.2 trillion. That is not insured. Boom. As we’ve seen <laugh> in in Greece, in Cyprus, in Portugal, in many other countries around 2013, all the rest of that gets bailed in. So you have to kind of wonder if you’re a small business and you have your payroll in the banks and that beats that $250,000 insurance limit or is your payroll gonna be bailed in when there’s a bail-in event? So how much of the 5.7 trillion in other assets could be those speculative derivatives? We already know that banks generate more than 52% or 50% of their income through trading. But let’s just take a look at how much is in that fund to protect the other. That what, what did I say that was 9.2 trillion? 9.9 trillion. How much is in there to ensure that? Let’s take a look. This is the deposit insurance fund balance, also known as the DIF and these are the insured deposits. So there’s your 9.9 trillion, but oh my goodness, they only have 124.458 billion to insure 9.9 trillion. Does that seem about right to you? No. That’s 0.0126 pennies for every a dollar, one insured dollar. So that means that as long as only one bank and they go down in an orderly fashion, okay, you are not gonna know it. But if there is indeed to real crisis and a lot of those big banks, you saw the four big insured banks, they go down at once, you, my friends will notice because they’re not gonna be able to give you that money. And they were one small bank failure away after 2008, 2009, one small bank failure away from the whole world knowing that they were out of money. They’re ensuring 9.9 trillion. How are they gonna do that with 124 billion? They’re not. So what all of this is, is extreme leverage with minuscule reserves because all of the new laws way more than what I’ve talked about, has been all about reducing reserve requirements. And what that means is if the banks don’t have to put money here for a rainy day, then they have more money to speculate and play with and then that means more profits and all sorts of other things. And as long as everything is hunky-dory, you’re okay. You’re never gonna realize the risk you’re in. But when things turn different, they turn different. And by the way, they have turned different. The debt bubble has popped.

Wall street’s lucrative leverage debt machine is breaking down. They’re stuck. And we’ve talked about this before with roughly 40 billion of risky debt on their books that they typically repackage and sell to you for your retirement, for your IRAs, etcetera. And now they’re stuck with this debt because, because frankly investors are going, no, I’m not really comfortable with this. Yeah, so they haven’t been buying it. And I just wanna bring this up cause we talked about it a couple weeks ago. The 12.6 billion of debt that backed Elon Musk’s buyout of Twitter is by far the biggest burden weighing on balance sheet for any single buyout. But what I wanna point out to you is that the equity that he used were his shares of stock. That’s when he used that as collateral for these loans. And now that stock is down big. Can you see it? It’s oh, a tangle web. We weave, well first we practice two decede. This is a very tangled, tangled web, but in the same time, so this is their lending machine. The debt machine. Bank of America reaps benefits of volatility of as lending income misses. So traders beat estimates of what they’re going to all of that volatility that generates the trading revenue and those traders beat that estimates not on the debt side, not on the lending side, but on the speculation side because investment banking, so we’re talking about this kind of banking over here fell 54% and don’t you think the banks are gonna be more and more dependent on trading revenues? What they can pick up fees for advising on mergers and acquisitions declined 43%. The underwriting of equity deals fell 65% debt underwriting slumped almost 58%. You see the problem? So they’ve gotta keep this machine going. They’ve gotta keep those profits going. And speculative trading becomes a whole lot more important.

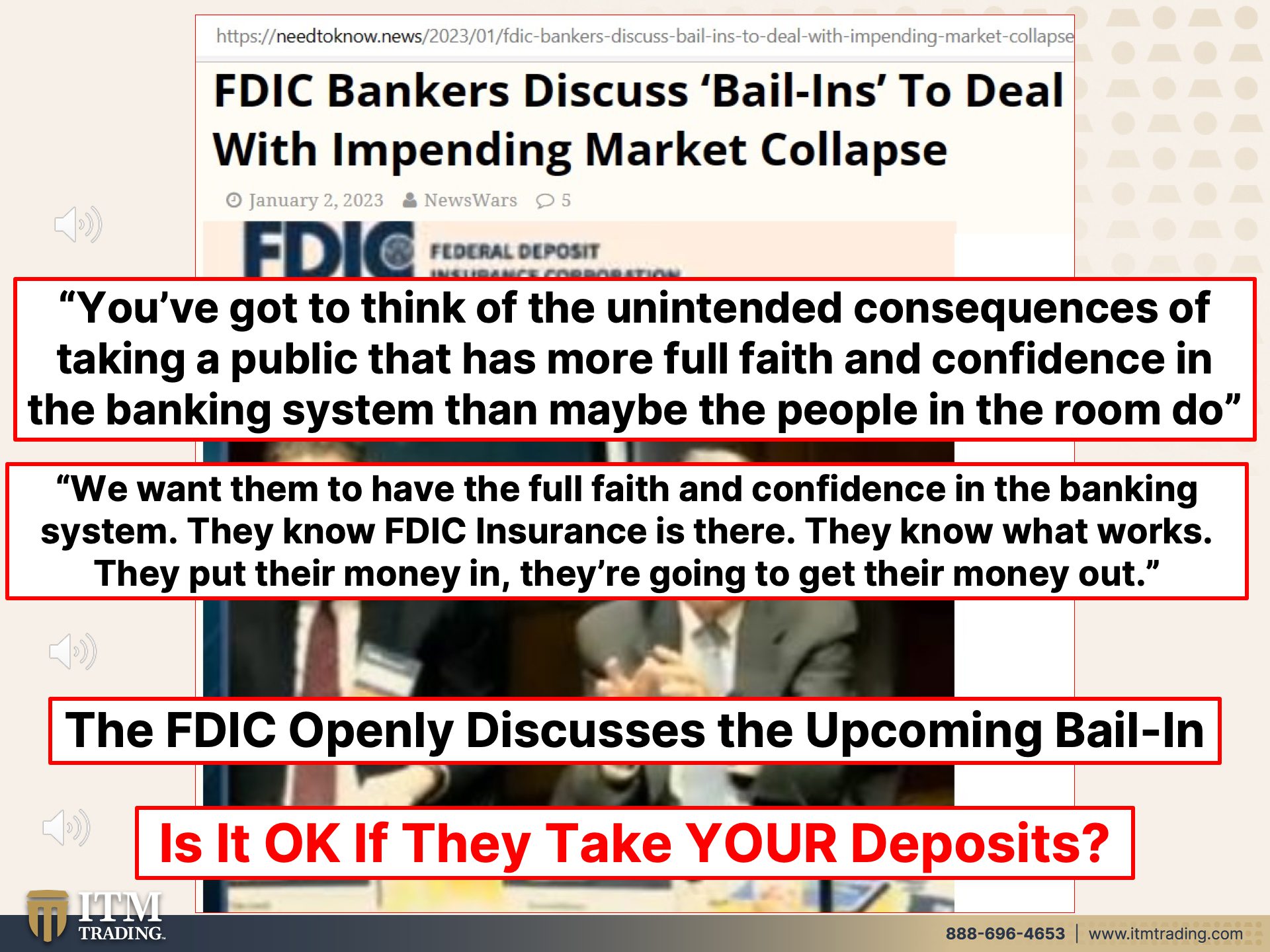

But this is what I really want you to hear because it’s not me saying it. This would be if you only share this slide with your family and friends, they need to hear this. And by the way, the link for this entire, I think three and a half hour meeting is below. But you also have just the snippet links as well, because the FDIC bankers discuss bail-in’s to deal with impending market

Accessible when people need to know. But I don’t think you have much hope of of reaching a public that doesn’t have a professional need to know.

Why do you need to know?

I completely agree with that. I almost think you’d scare the public if you put this out. Like why are they telling me this? Should I be concerned about my bank? Like my insurance company doesn’t tell me what they’re doing with my assets, they just assume they’re gonna pay my claim. Right. It’s, it’s, I I think you’ve gotta think of the unintended consequences of taking a public that has more full faith and confidence in the banking system than maybe people in this room do.

And that’s the FDIC

We want them to have full faith and confidence in the banking system. They know the FDIC Insurance is there, they know it works. They put their money and they’re gonna get their money out. So there, there’s a select crowd of people that are in the institutional side and if they wanna understand this, they’re gonna find a way to understand this. There’s a bunch of law firms represented in this room. There’s a bunch of people that’ll charge ’em by the hour. A lot of money to explain this all to ’em. And, and and, and it’s fine. And I, I don’t have a, I don’t have a problem with that and they all have huge staffs, but I would be careful about the unintended consequences of starting to blast too much of this out in the general public.

Yeah, because they don’t want you to know. And just like we saw in Cyprus and you remember that graph and maybe Edgar, we can just kind of post that in there. Your deposits are what they call sticky. Ask yourself, when was the last time you changed banks? People don’t, they just trust, okay, I’m gonna make my deposit. That’s my money. It’s not, it’s legally their money. It’s not your money. You’ve now loaned them that money. But in your mind you’re thinking that’s my money. And so when this next crisis happens, well let’s see what they say about discussing the bail-in

Little bit conflicted, right? I mean it’s important that people understand they can be bailed in, but you don’t want a huge run on the institution. But they I mean they’re going to be, that’s, and and it could be an early warning signal to the FDIC and the primary regulators when these things happen. And there may be some other prices. This is similar to what Jay was saying in the market that you can tell whether people understand how the, who’s gonna be protected, who isn’t going to be protected?

You’re not gonna be protected.

I think an interesting study to look at the evolution of market prices in a situation like March of 2020 for example, and see whether people understood what might happen, right?

Yeah. Did you think that in March of 2020 were you thinking that your savings might be bailed in? And so what did you do? That’s when there was a start of the run going all the way back to the beginning, right? That’s when there was a start of the run at the banks and we had all those central banks tried out and say, oh, but no, we can just print as much money. We can just print as much money as we want. You don’t have to worry about your deposits in the bank. You can get your money back. Yeah, of course it has a whole lot less value. Hello inflation than when you put it in there. But people will ask me all the time, oh, but what about CDs? And what about bonds? Well, okay, let’s see what the FDIC, this FDIC committee says about that.

I think we have to sit down and talk to long-term debt investors and make sure that they as a stakeholder group fully understand bank debt today is not what it was before. It is not principle protected by design. And I think that that is that expectation. I like how you started off Betsy. Like it’s all about expectation setting. And I think that is, that is absolutely critical if that doesn’t hold, this whole thing doesn’t hold. And so I think it’s one area to focus on. I do wanna go back to something Jay said about stable

So they know what they’re about to do and they’re making plans. Are you making plans? Because you need to click that Calendly link below and set up a time to set up your own strategy and become your own central bank because you cannot count on FDIC insurance. You cannot count on them. And my question is, you’ve gotta ask yourself, is it okay if they take your deposits? Is that okay with you?

Now look, we can’t just close out our bank accounts and I’m not telling you to rush and pull every penny out of the bank. If you’re running a business like I am, obviously, you’ve gotta have money in there to run your business. But anything more than that, why are you leaving it at risk and in jeopardy? They have roughly a penny for every insured deposit. They have a lot of deposits that are not Insured. I make sure that I have enough cash outside of the system in a private vault so that if something like that happens, I can still pay everybody that works with me cause I don’t want them to be in a bad position. Now of course, once they take this all digital and we have CBDC’s that makes having this and this outside of the system that much more important because it is good money, good assets as Roosevelt says, that will get you through whatever you need to get through. Cause you can always convert this into the local currency if you need to. Or if like we were in the depression, we go to bartering because people no longer trust the money, then you’ve got something to work with because this has the broadest base of buyer and the broadest base of demand and it’s the only financial asset that runs no political risk and no counterparty risk.

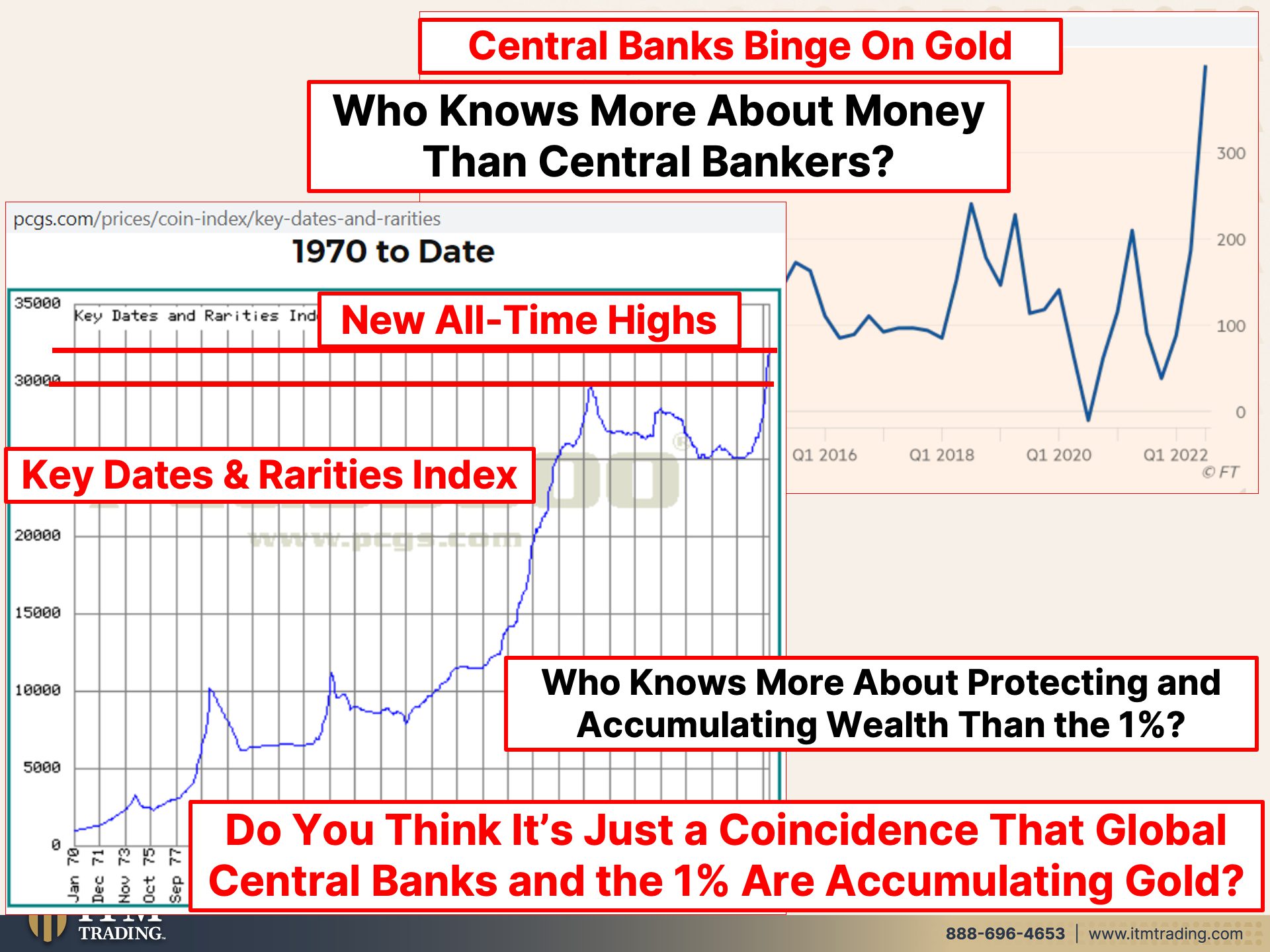

And we know that central banks have been binging like crazy on gold. Why? Cause you just listened to the whole group over the FDIC. You think central bankers don’t know that better than you and me? Oh yes they do. And they also have an indication of just how close we are. And while everybody makes this assumption that they want this thing to keep going forever, I do not make that assumption because there’s no, virtually no purchasing power left in the currency and they’re anchored somewhere near zero. They’re attempting to do a liftoff in interest rates, but that’s pushing us into much more than a global recession. Although if you listen, you’re going to hear, oh, this is just gonna be a mild reset. No, this is the end of the, of this currency’s life cycle. It’s the end, it’s over, it’s over. There’s no purchasing power left. They have to attack principle. That is by the way, what negative rates are, but this is not impacted by it.

And who knows more about money than central bankers and who knows more about what they’re doing than central bankers? But also the 1%, right? Look at that, these coins. Now this is not, this is not an ultra rarity, this is a lot more common than that, which is all we need. I just wanna be in this category. You don’t need to spend 8 million on a coin, but I wanna be in this category because as we’re seeing in places like Ghana and India, etcetera, that gold can easily be, well, not easily, but gold can be confiscated. They don’t want you to hold your wealth. But are they going to swap an 8 million coin for $42 and 22 cents or even $50, which is the face value of the new one ounce gold eagles. No. So I wanna be in that category so it doesn’t matter. What if I’m right and they confiscate? What if I’m wrong and they don’t? Confiscate doesn’t matter. A hundred bazillion percent. This is the end of this currency’s life cycle. And nobody seems to be talking about it but me. I lived through it. I lived through it in 71. I know what that looks like. I wanna live through it this time with my wealth protected because who knows more about protecting and accumulating wealth than the 1%. I mean, seriously, do you really think that it’s just a coincidence that global central banks and the 1% are accumulating gold as fast as they can at the same time? Hmm, I don’t think it’s coincidence. And I think this is what you should do too. It’s what I’m doing.

So we started doing something for, for just this minute because it is so important for you to understand that the system actually died in 2008. And so that 2008 was just a warning. So I know we just put out a piece on the history and everything that led up to 2008 and then to where we are today. But Eric and I also did a piece, just a conversational piece to help you understand that even better. So, because it’s critically important. Ignorance doesn’t make you immune, it just leaves you vulnerable. And we’re trying to create pieces that you can share with your friends and loved ones that maybe they will listen to and start to understand where we are. Because seriously, we’re running out of time. And again, if you have not yet started your gold and silver strategy, click that Calendly link below and give us a call and set that time up. You’ve got to have wealth insurance and that’s exactly what gold is and purchasing power insurance. And for me, that’s what silver is. So if you like this, please give us a thumbs up. Make sure you leave us a comment, make sure you subscribe. And really, I think this is a great one to share, share, share. Even if all you share on this one are the audios from that just recent FDIC meeting. Share please. And until next we meet, please be safe out there. Bye-Bye.

SOURCES:

https://www.federalreservehistory.org/essays/glass-steagall-act

https://www.federalreservehistory.org/essays/gramm-leach-bliley-act

FDIC Quarterly Second Quarter 2022 Volume 16 Number 3

Wall Street’s Leveraged-Loan Machine Breaks Down With Twitter Debt Left Unsold – Bloomberg

Bank of America (BAC) Reaps Benefits of Interest-Rate Hikes, Trading Volatility – Bloomberg

https://twitter.com/i/status/1608294141812785152

https://twitter.com/i/status/1608510850700017667

*This is the full FDIC meeting https://onlinexperiences.com/scripts/Server.nxp

https://www.pcgs.com/prices/coin-index/key-dates-and-rarities