DOLLAR GOING TO ZERO: How The System Was Rigged All Along

When it comes to the economy and what’s about to happen to the U.S. dollar and in fact, our entire way of life. This is global. So no matter where you are, this is about to happen to all of us. But you’re either well-researched and so many of your friends and family think you’re crazy or you’re just starting your research and you’re not even convinced yet that there’s really a major problem in either case. This is the video that shows you the truth of where we are, what brought us here, and the next most likely outcomes, which could absolutely make or break your financial future.

CHAPTERS:

0:00 US Dollar in Trouble

1:43 Four Pillars of Money

3:52 Purchasing Power of Consumer Dollar

6:19 Overnight Fed Funds Interest Rates

10:08 Original Functions of Money

13:31 Protecting Your Wealth

SLIDES FROM VIDEO:

TRANSCRIPT FROM VIDEO:

When it comes to the economy and what’s about to happen to the US dollar, and in fact our entire way of life though, this is global. So no matter where you are, this is about to happen to all of us. But you’re either well researched and so many of your friends and family think you’re crazy or you’re just starting your research and you’re not even convinced yet that there’s really a major problem. In either case, this is the video that shows you the truth of where we are, what brought us here, and the next most likely outcomes, which could absolutely make or break your financial future, coming up.

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, which is a full service physical gold and silver dealer. And I have to tell you that without a doubt, I have been groomed for this moment in time. Having been fortunate enough to study currencies and currency life cycles at Shearson since 1987. What I got to see were repeatable patterns. This is not rocket science. I’m gonna show you why you’re hearing talk of a reset, which if you listen to the World Economic Forum, is social, economic as well as financial. Let me show you, let’s just go ahead and start.

Because the reality is, is that we work for money and everybody wants to be fairly paid for their labor. Well, you wanna also have the ability to accumulate that wealth and use it in the future and want to last forever. So there are four pillars of money. One is a tool of accounting. So you know how much you’re gonna get paid a tool of barter so that you, the economy can specialize. You can have a lawyer, you can have a farmer, you can have a baker. You want it to be a store of value short term so that you are fairly paid for your labor and you want it to be a tool of savings for future use. And anybody that’s a tried to save dollars knows that through inflation, they lose value over time. You can’t buy as much with them tomorrow as you can buy with them today. But all of these things were true when money was actually tied to gold and we had a gold standard. But frankly, central banks very quietly, as invisibly as possible, are changing the definition and the very foundation of money. And frankly, not in your favor. So I can’t tell you when they did that. But in a recent research report that I was doing, I discovered that they removed one of the pillars of money and we went from four functions down to three, just a store of short-term value, a unit of account, and a medium of exchange. Well, at least eliminating the tool for savings for future use is more honest. But boy, is that okay with you because they’re forcing you to go out on the risk spectrum to keep pace with the inflation that they’re creating when they print money. More about that, and let me show you what I’m talking about because this is critical for you to see really simply cut out all the garbage.

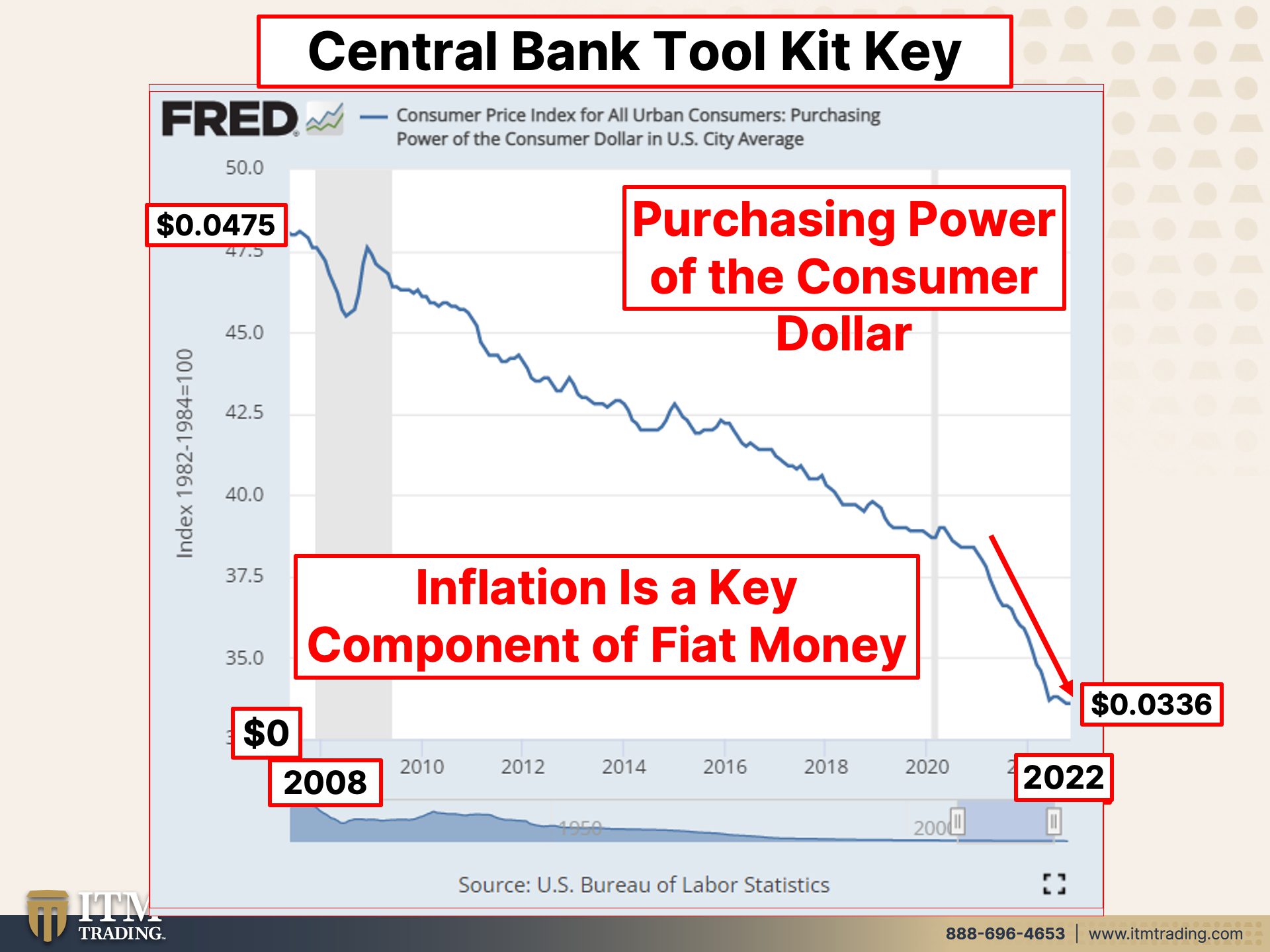

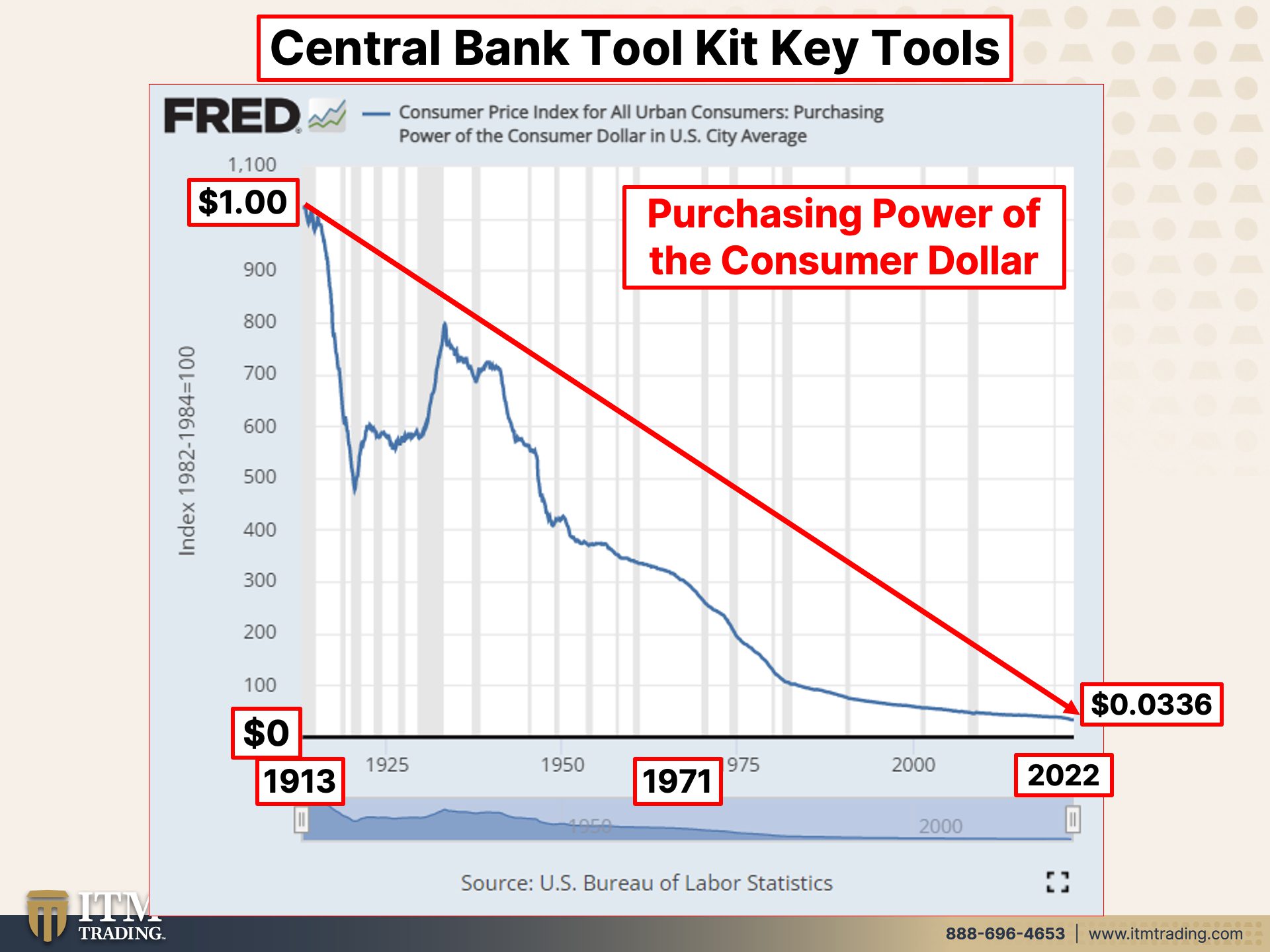

I’m gonna show you two key charts to pay attention to. Both of them are from the Fred, which is the Federal Reserve Economic Department. You can click on those links below and pull these charts and graphs up yourself. The first one, the most important one, frankly, is the purchasing power of the consumer dollar. So you can see back in 1913, there’s your dollar. Now, isn’t that interesting? How close are we to that zero? Now, you may say to me, but Lynette, look it, it’s just kind of leveling off. And I would say to you that what you’re really actually looking at is not a leveling off. But let me show you, I’ll, I’ll come back to this, but just hold on to the image of this in your mind. This is short term since the financial crisis in 2008, and that’s how much purchasing power we have had to lose in order for the central bank to print enough money to satisfy Wall Street. Okay? Every time they do this, the money that’s already out there loses purchasing power value by design. Inflation is not a monetary phenomenon. It is a fiat money phenomenon. What is fiat money? Well, it is government backed money. And what are we told backs the dollar, the full faith and credit of the US government. Well, let’s translate that. As long as you trust them, you have faith, then you will continue to loan them money, extend them credit. So what backs the currency is the government’s ability to generate and create more and more debt. Well, when you got debt, you got interest payments. So are you really surprised that inflation is part of the very system? Nominally a hundred dollars 20 years ago, a hundred dollars today, exactly the same. It’s a hundred bucks. But what that a hundred bucks would buy you 20 years ago and what it would buy you today, vastly different. So officially we have roughly 3 cents left in terms of purchasing power out of the original dollar.

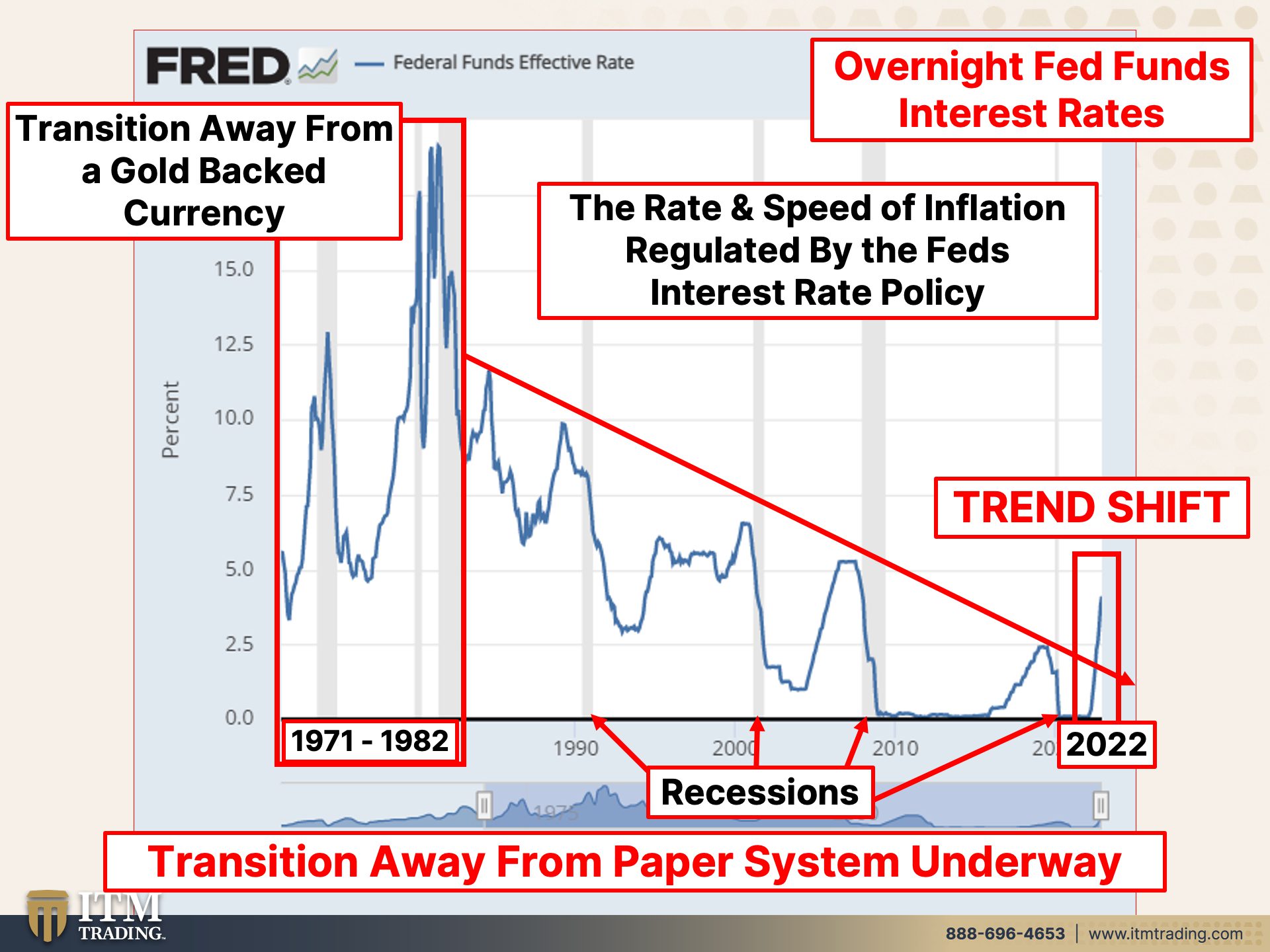

Now, how did they do this? This is really the great experiment that started in 1913, which is using interest rates to regulate the speed and the rate of inflation. So if they want to speed inflation up, they drop interest rates down. That inspires more borrowing and spending. And if they want to slow inflation down like we’re seeing in the globe right now, they raise inflation and interest rates up and that reduces borrowing and spending. At least that’s the theory. So this, what you’re looking at again from the FRED is the overnight fed funds rate. This is the rate that the central banks control directly. Now, interestingly enough, 1971 when we went off the gold standard to 1982 was when we were transitioning from a gold standard to a debt-based system. Okay? Now they ratcheted interest rates all the way up to 18.5%, Actually 21.5% intra day. And today, 18.5% These gray bars are official recessions and, and they gave themself enough ramp room that every time they went into a recession, they could drop interest rates between five and a half and five and three quarters percent, which again would inspire borrowing and spending. But when the financial crisis hit 2007-2008, they dropped the interest rates all the way to zero. And in the attempt to raise them, it was a big fat fail, as you can see. And they were forced back to zero again. But all the money printing they did between 2008 and today, really all of that inflation was held inside of the stock market, the bond market, the real estate market, those markets that they specifically targeted for reflation. And now what we’re seeing is a trend shift because this downward line like this is a trend line and the trend has been broken. This is a big deal because what it tells you, whether you realize something or not, is that things are changing and it doesn’t matter whether or not you fully understand it. Ignorance does not make you you immune though. It just leaves you vulnerable. So when you hear Wall Street talk about a 30 year trend and how that’s shifting, well, here it is, you can see it and you can also see that every time they raised interest rates, it’s sent us into into a recession. This coming, this recession coming up that everybody’s talking about. Of course now they want you to think no recession ahead, but it’s garbage. And that’s for another day. If you, if you go ahead and you look at this, what’s coming up is gonna be far bigger than a recession because even where they are right now, can they drop interest rates and not be below zero? With the historic norm of five and a half to five and three quarters percent? No, they can’t. So negative rates are in our history, but that’s mostly because what do we have here? We have virtually no purchasing power left in the currency. So what do they have to do? They have to attack your principle, and that’s what negative rates are about. And they ran this big test since 2009 and it was a big fat fail, but hey, let’s do it again. Maybe it’ll be different this time.

So just as a quick review, what’s the original functions of money? It’s a tool of accounting for measure, a tool of barter for trading, a tool of savings for future use and legacy building, and a store of value for fair payment of labor. Four key functions and only gold fulfills those functions. And the other things that you need to know is this gold gives you power, and we always vote with our purse. So if you as a consumer did not like what the government was doing when we were on a gold standard, you would walk into the bank with this and you would walk out the bank with this. And that would create restrictions around what governments could do, how much more debt they could grow. So the public had control and it is decentralized and virtually invisible. You hold it, you own it outright. In fact, the BIS, the Bank for International Settlements tells us that gold is the only financial asset that runs no counterparty risk. So it’s key, your control, your privacy. Then they shifted us to this Federal Reserve notes. Well, a note is a debt instrument and it’s under their control. So the Federal Reserve raises or lowers interest rates and an a attempt to regulate the rate and speed of how much this loses value and how quickly it does it over time. But if you’re sitting in this, you still preserve your principle, not your purchasing power, but you preserve your principle because this is a debt instrument that guarantees that for future use. And you may have a hundred dollars bill like I showed you before from 20 years ago. Nominally, they’re identical and if you hold it, it is still private. They’re transitioning us into a central bank digital currency, CBDC, which is programmable fiat money. This is not programmable, it’s policy, but programmable money, which means that it is completely under their control. And the Federal Reserve is talking about having their finger on that button constantly to make sure that they get the results that they want from their policy. And you have absolutely no privacy. They see how much you make. Everything goes through the system. They see what you spend, they see where you spend it, they know how much they can tax you. They can take that money out. They can say, oh, if you don’t spend this here, here, and here, then it goes away after a certain period of, anything. But it is programmable with no privacy. So you have to decide what kind of money you actually want, because when they go to CBDC’s, then it reduces those four functions to two simply as a tool of measure and a tool of barter. Because when your funds hit your bank account into negative rates, boom, they immediately start going down. So you’re not even gonna be fairly paid for the labor that you’ve always put forth.

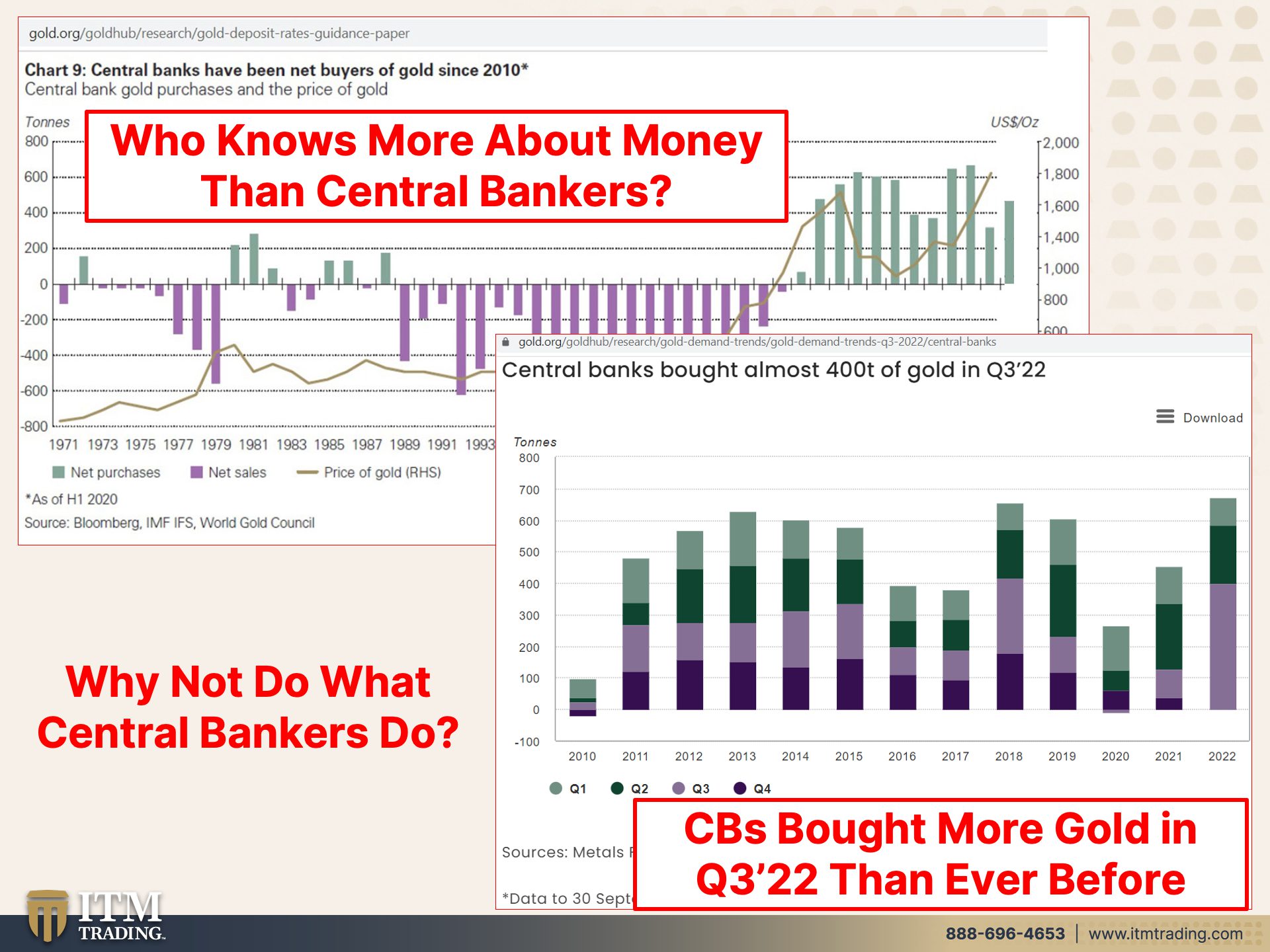

Now, what is central bankers doing for themselves? Guess what? They’re buying gold. And frankly, who knows more about money than the central bankers And who knows more about what they’re doing than central bankers? And maybe because they know that this is the end, they’ve gone out through the third quarter of 2022. We don’t have fourth quarter numbers yet, through the third quarter, and they have bought more gold than ever as long as they have been tracking it. And you can certainly see this. We don’t have 2022 numbers on the top. This is for 2022 so far. So why aren’t you doing what the central bankers are doing for themselves? I am.

SOURCES:

https://fred.stlouisfed.org/series/CUUR0000SA0R

https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-q3-2022/central-banks