Central Banks Warn Against Forced Selling

I have been hearing the term “forced selling” quite a lot recently. Do you know what forced selling means? It means stock market and bond market collapse. I was there in 1987 on Black Monday. I know what that looks like, smells like, tastes like everything. And let me tell you something else. When there is forced selling, everything gets sold with it except for physical gold and physical silver.

CHAPTERS:

0:00 What is Forced Selling?

1:38 Alchemists of Wall Street

8:19 Corporate Defaults Coming

10:47 Fed’s Latest Rate Hike

13:22 Forced Sale on Consumer Goods

15:43 ECB Warning

20:13 Gold Mining Reached Record High

SLIDES FROM VIDEO:

TRANSCRIPT FROM VIDEO:

You know what keeps coming up a lot that I’ve been hearing? The term “forced selling” You know what forced selling means? It means stock market and bond market collapse. I was there in 1987 on Black Monday. I know what that looks like, smells like, tastes like everything. And let me tell you something else. When there is forced selling, everything gets sold with it except for physical gold and physical silver, coming up.

I’m Lynette Zang, Chief Market Analyst here at ITM Trading a full service physical, gold and silver dealer specializing in those custom strategies. And boy, you better have one <laugh> if you don’t click that calendly link below and make an appointment because things are changing very, very rapidly. And what I thought was really interesting is the video that I recently did on treasury liquidity where I showed you where the traders took over. And then right after I did that video, what was the next headline that I saw?

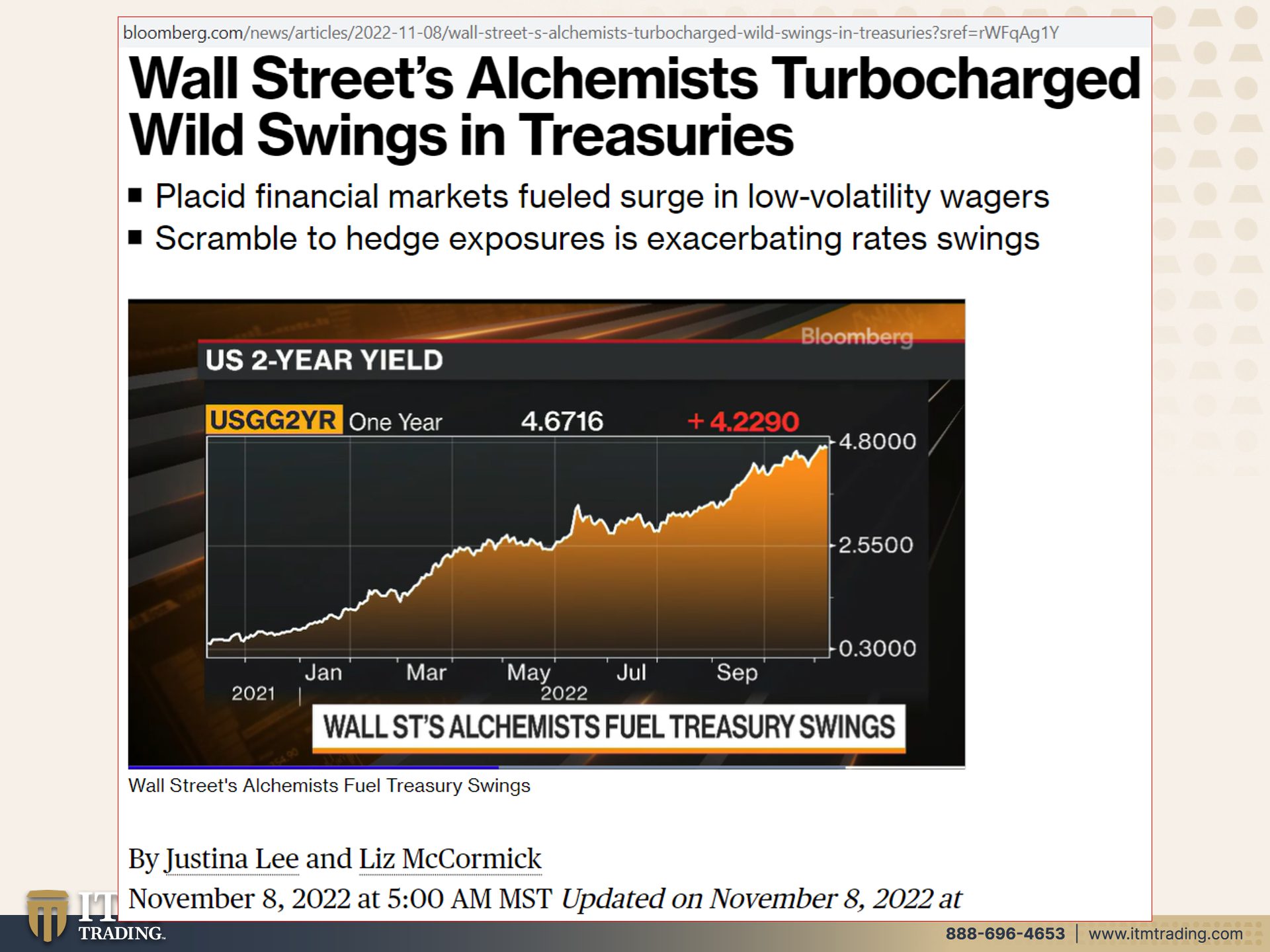

Voila. Wall Street’s Alchemists Turbo charged wild swings in treasuries. You think? Of course, because traders don’t really care about stability in any of the markets, but you need to understand that the treasury market is the foundation of the global system. And so all of this manipulation that the central banks did, I mean look, they used interest rates to regulate the rate and speed of inflation. They wanted big inflation after or during 2008 when the system actually died. So they gave it over to the traders. And now are they lamenting that?

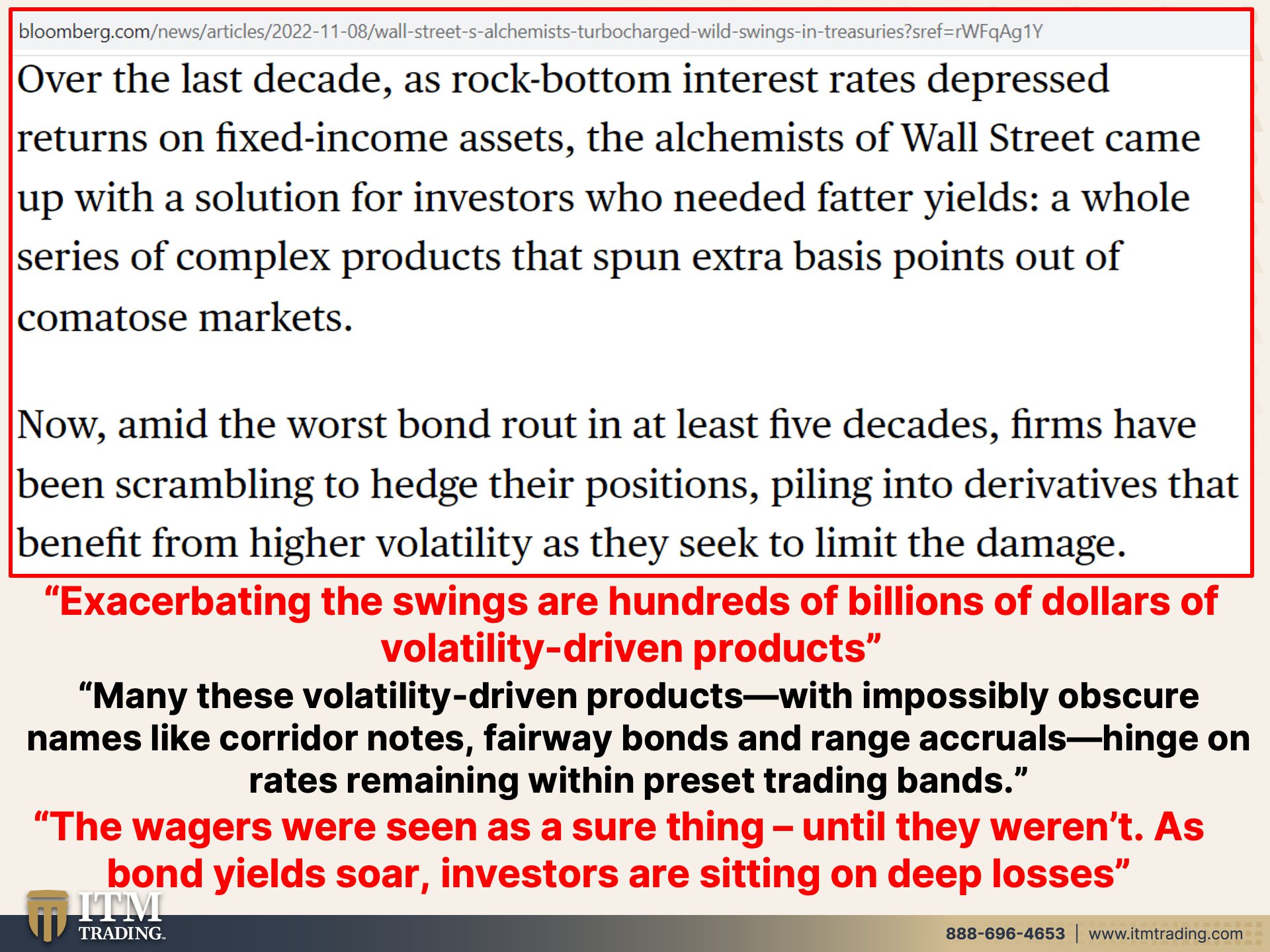

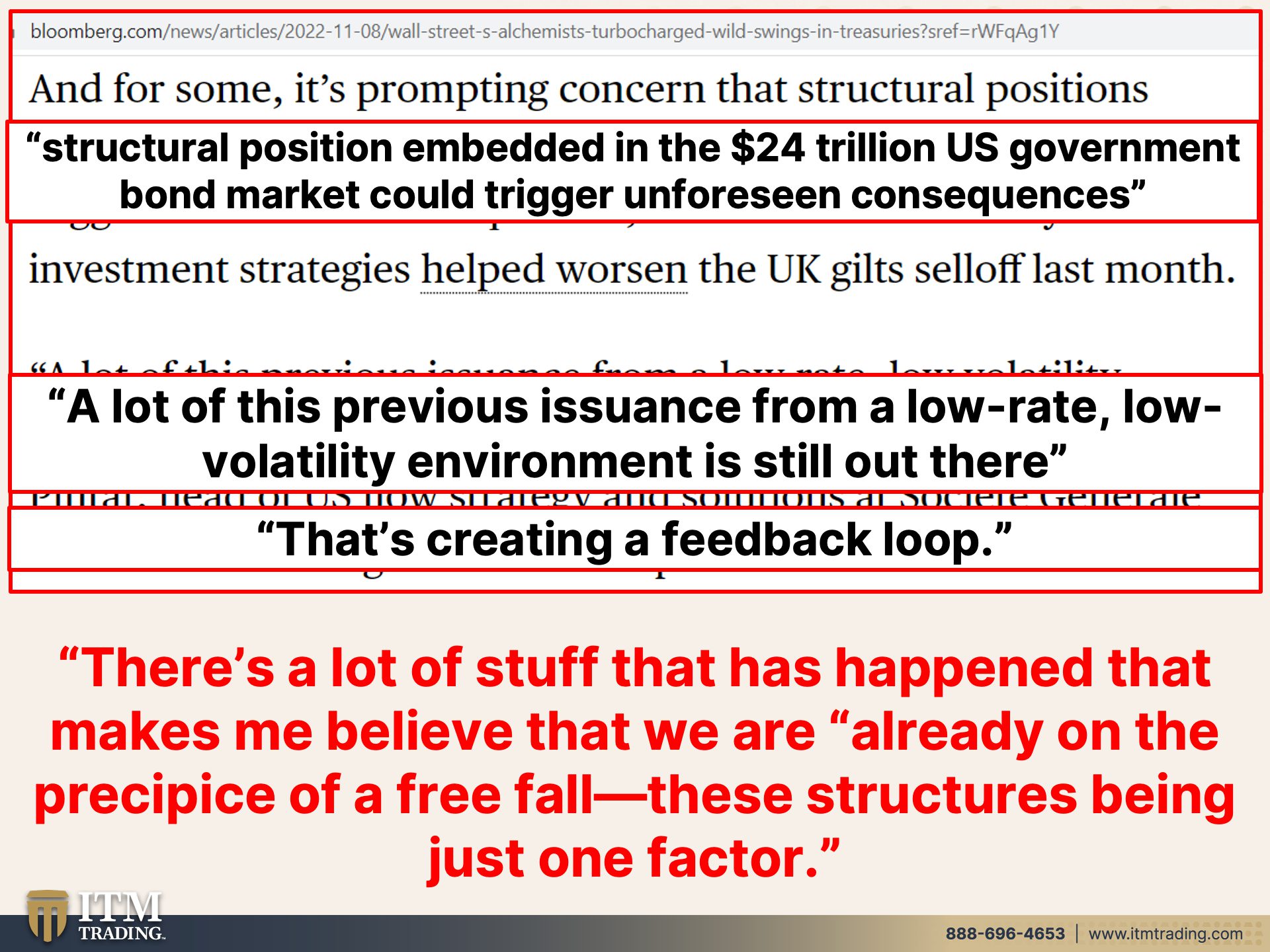

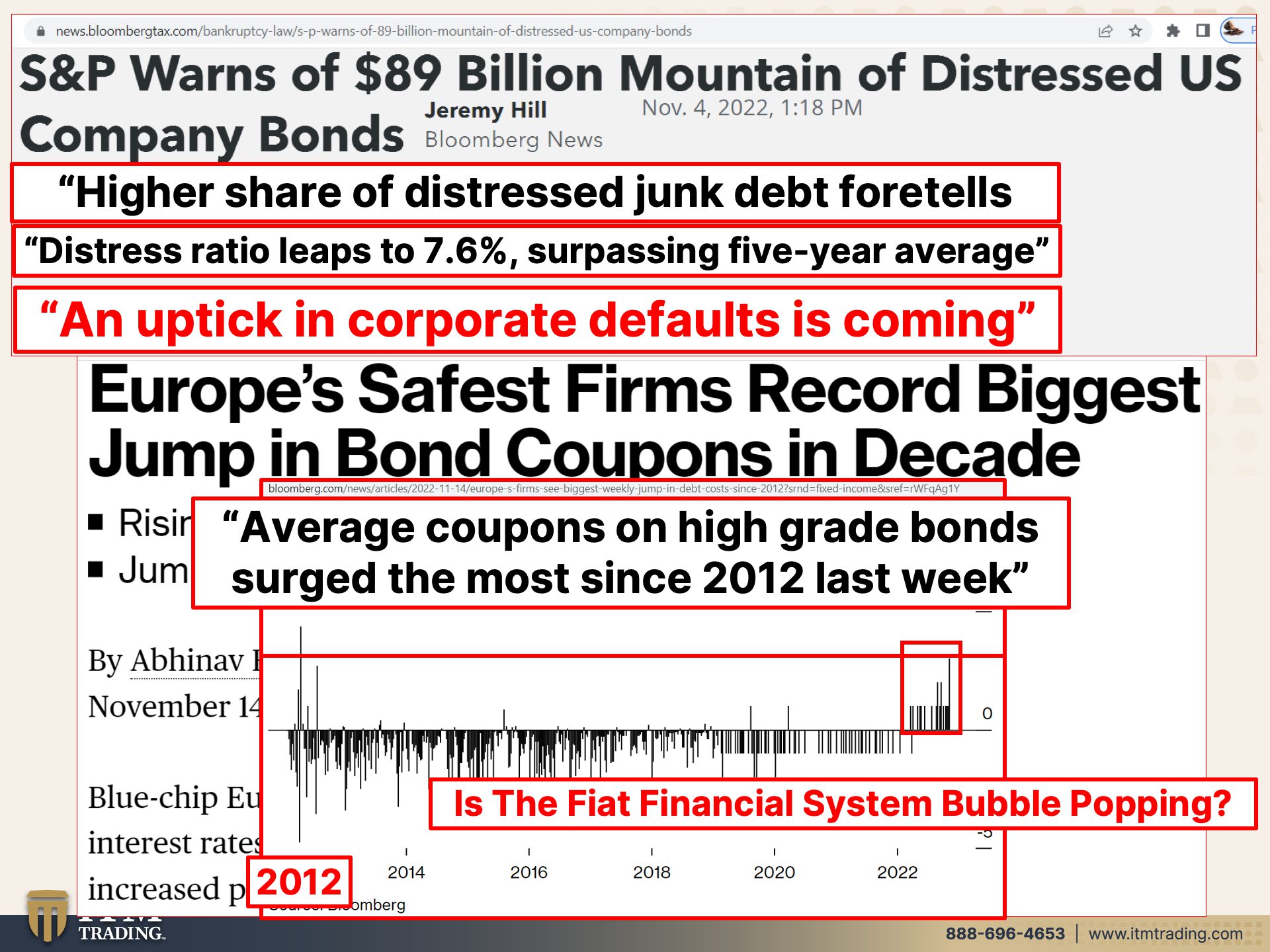

Oh my goodness, who are they gonna blame that over? Because over the last decade as rock bottom interest rates, depressed returns on fixed income assets, the alchemists of Wall Street came up with a solution for investors who needed fatter yields. A whole series of complex products that spun extra basis points out of comatose markets. So derivatives, they created tons and tons of complex derivatives. And make no mistake about it, the derivatives markets will be our downfall because it’s so leveraged, so big, so opaque that we can’t even think about the Black Swan event that’s coming out of that. But now amid the worst bond route, in at least five decades, firms have been scrambling to hedge their positions piling into, they just say derivatives more derivatives that benefit from higher volatility. So what they’re doing, what Wall Street does, is that they are creating product after product with all these formulas and algorithms and etcetera, etcetera, that are so complex. And they say this, if we make this really complicated, nobody questions us. But the problem is, is they make this so complicated that they don’t even understand it. They don’t understand what might happen, the unintended consequences, but exacerbating the swings are hundreds of billions of dollars in volatility driven products. So they want this volatility. They’re traders, they’re…should that be the foundation of the entire system. I don’t think so many of these volatility driven products with impossibly obscure names like corridor notes, fairway bonds and range accruals, hinge on rates remaining within preset trading ranges. So now you have the central bank that wants to raise rates inside of all of these products that are based on those rates staying within a very narrow range. Can you start to see the problem? Because we don’t know, it’s not hundreds of billions. It is more likely trillions and trillions in even quadrillions. The wagers were seen as a sure thing until they weren’t. As bond yields soar investors are sitting on deep losses. You know when something seems too good to be true, I gotta tell you, it’s typically not so true. And for some it’s prompting concern that structural positions embedded in the 24 trillion US government bond market could trigger unforeseen consequences. You think? Because I think so, structural positions, do get that? It is the foundation of the entire system that is now based on derivative, leveraged bets. How comfortable does that make you feel? Because it does not make me feel very comfortable. A lot of this previous issuance from a low rate, low volatility environment is still out there. And the point I wanna make on that is we are shifting from LIBOR to SOFR in what, eight months? Or by the end of eight months I should say. And there is a lot of issuance out there that still has to shift. And when they shift, the valuation changes, I’ve done videos on this, please make sure that you go and watch them. Maybe we can put that one video link up there. But that is creating a feedback loop because everything is all convoluted and interconnected. And what do you think that’s gonna? Do when there are unforeseen consequences? Because the structure that has been built is not strong. It’s based on things going like this volatility going like this that is not good. Or remember, this is nice and strong. What you’ve got going on here is just the opposite. It’s creating a lot of fragility. There’s a lot of stuff that has happened that makes me believe that we are already on the precipice of a free fall. These structures being just one factor. What are some other factors? Cause what we’re talking about here is the treasury bond market, but there’s also 89 billion mountain of distress US company bonds. So these corporations, these zombie corporations that could not pay all their interests, let alone any of their principle. So the banks just kept loaning the money to pay the interest so that they didn’t have to declare this as a bad debt on their books. Well, this is coming home to roost now, because as long as interest rates were anchored at zero, then they could just keep piling on the debt. But now that interest rates are up all of that mountain of debt, it still needs to be paid or restructured or it’s gonna default. And that’s the problem.

There is a higher share of distress junk debt foretells defaults. So this is in our very near future. The distress ratio leaps to 7.6% surpassing the five year average. That’s like danger, danger, danger. So the warning signs are out there and an uptick in corporate defaults is coming and probably not that far down the road. And it’s not just here in the US because we’re all incestuously interconnected. But now Europe’s safest firms of record biggest jump in bond coupons in decades. That means interest rates going up, bond coupons, rising costs are a headwind to profitability. You think? I mean we’ve seen so many times how these corporate profits just went straight up through covid 19 and the whole pandemic, etcetera. Well now guess what, with the interest rates going up, they are the opposite is happening. And they’ve got rising costs on this mountain of debt as well as the inflation for whatever they’re inputting. Blue chip European companies saw the biggest weekly rise in the interest rates they pay on their bonds in a decade. A sign of the increased pressure on corporate balance sheets, and this is what that looks like. Average coupons and high grade bonds surge the most since 2012. What was going on in Europe back then? Hmm? The sovereign debt crisis. So are we in a debt crisis right now? Yeah, the debt markets are falling apart. Let’s make no mistake about that because I think what we’re really watching is the fiat financial system bubble popping. So that means bonds plus stocks plus everything. The treasury bond is the biggest thing because how are they gonna bail that out? So the treasury’s gonna buy back treasuries? I mean this is not gonna work. This should tell you how close we are to the end. So we’ve looked at the government treasury bonds and we’ve looked at the corporations. What about the individuals?

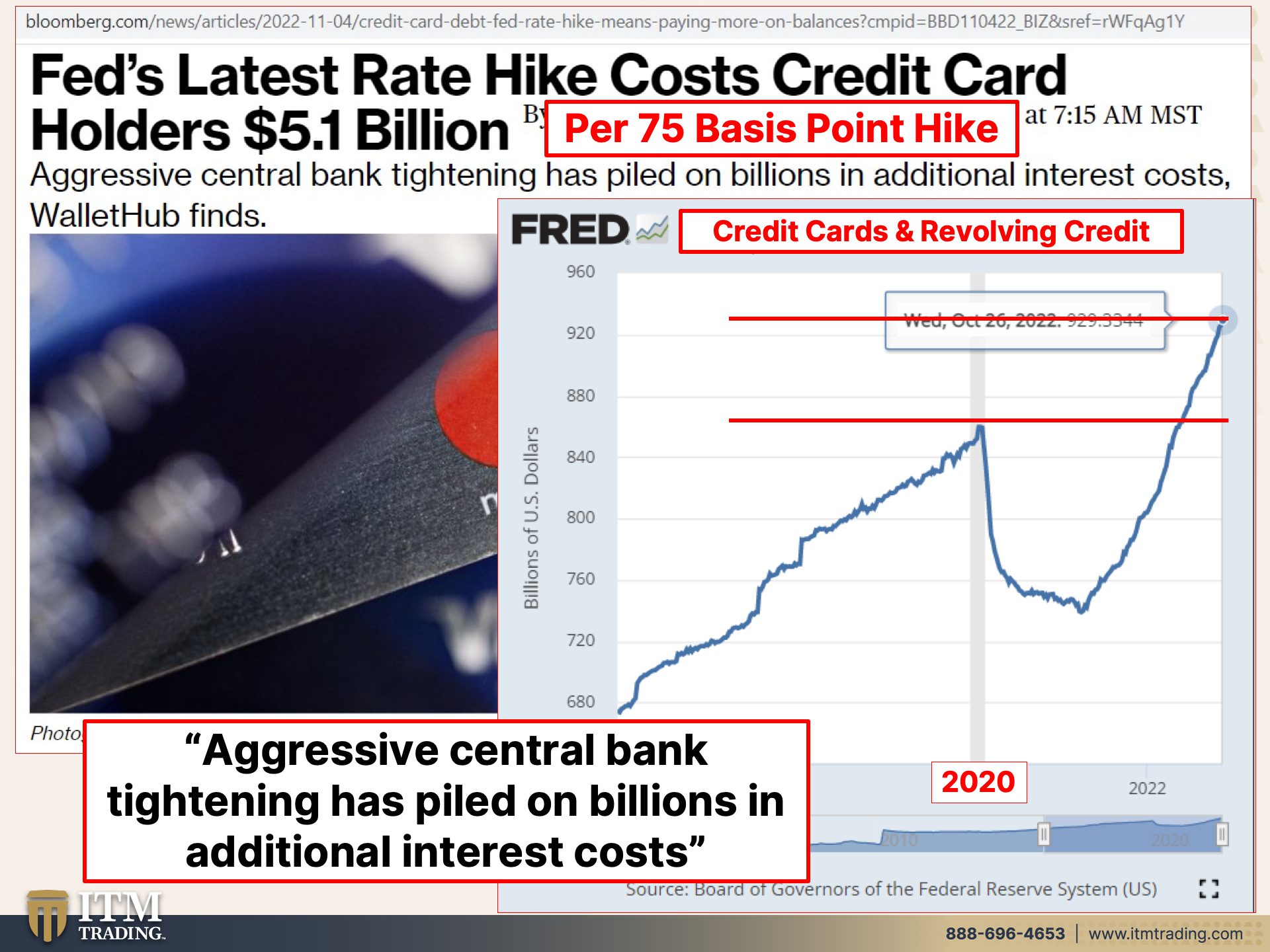

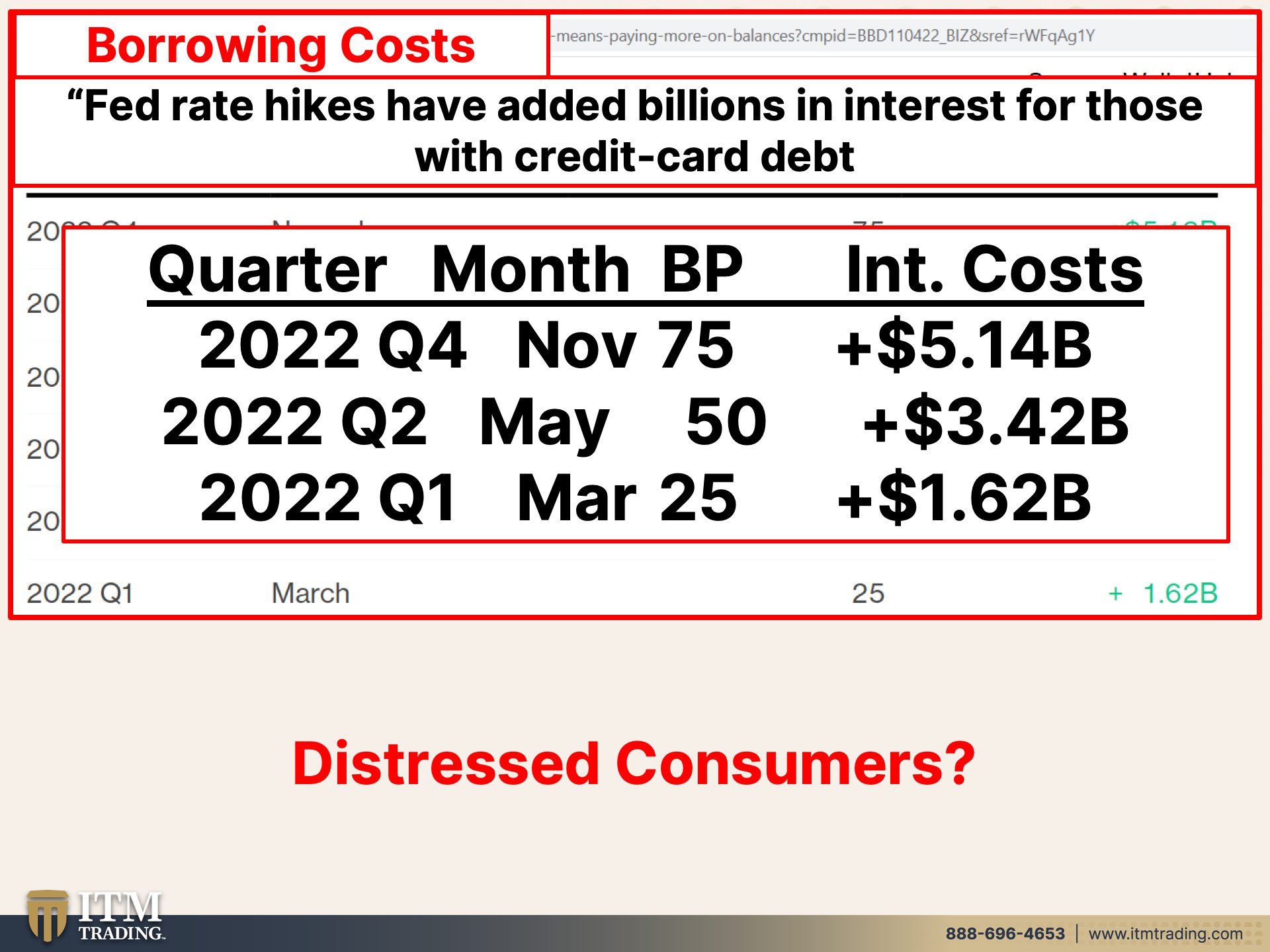

Fed’s latest rate hike costs, credit card holders, 5.1 billion. Yeah, that’s per 75 basis point hike. They’re gonna do a 75 basis point hike again? They might do 50, it doesn’t matter. I’m gonna show you in a second. But these are credit cards and revolving credit and you can see that they far surpass where we were in 2020. And you can see also from, well forever that the credit card balances just keep going up. But now more people are using them just to buy food and gas and energy and the things that they need. So that’s happening. While at the same time interest rates are going up. This is a huge problem and I hope you can see that. Aggressive central bank tightening has piled on billions in additional interest costs. So if the individual could not afford the food at the grocery store and they put it on a credit card and they’re not paying that credit card off every month, now they’re tacking on all of that interest. And before you know it, some people may be already compounding that interest. You ever getting outta debt when you do that? Nope. Not at all. This is what that looks like. All right, here you go. 75 basis points, 5.14 billion in additional interest costs. But let’s say the next one is 50 basis points, that’s still 3.42 billion in additional interest costs on these credit cards. And even if they do a 25 basis point move, that’s still 1.62 billion. Do you see the problem? And these credit cards are compounding that problem on top of the inflation and the prices that everybody’s having to pay for things. So what do you think? You think we might have a distressed consumer as well? So we’ve looked at a distressed treasury market where the treasury may step in to buy the treasury bonds back. You see distressed or distressed corporations with higher interest rates and higher costs and the distressed consumers. I’m thinking we got a real problem on our hands here.

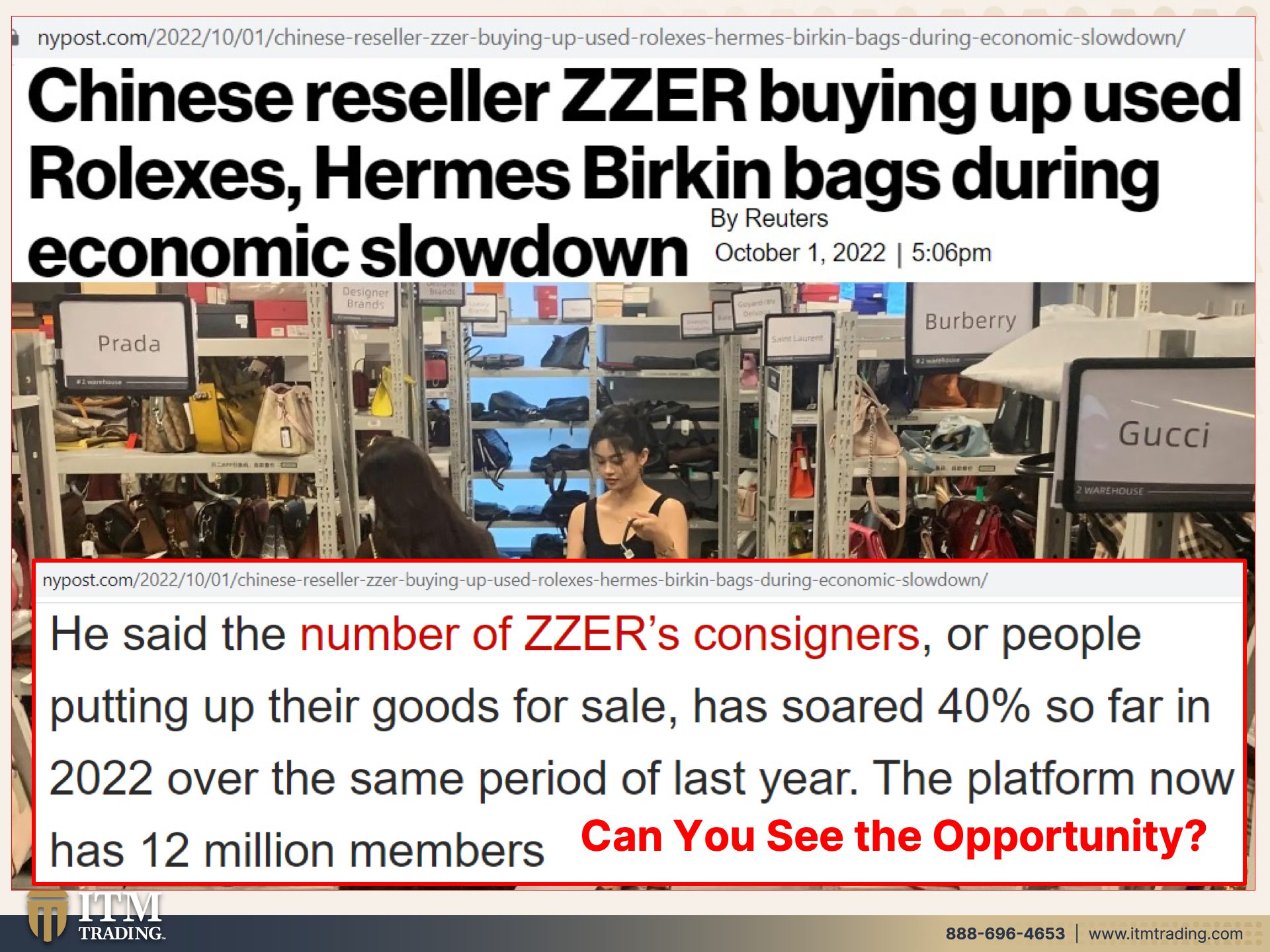

And here though is the opportunity. I’m gonna show this to you just in this one little piece because this Chinese reseller is buying up, used Rolexes, Hermes Birkin bags during the economic slowdown. You think they’re paying retail? I don’t think so? He said the number of ZZERs, consigners or people putting up their goods for sale has soared 40% so far in 2022. Because this is also a forced sale, right? If you need to raise capital, you’re gonna sell whatever the market will buy the platform now has 12 million members, but eventually because these are non income producing assets. But this is where it starts, right? So when you need to come up with money, you will sell whatever the market is willing to buy. And when that happens, what do you think happens to prices? They start to come down, not just at the resellers, but also you’re going to see it happen at the corporate level too, because they’re now gonna have to compete with this, but they’re also gonna have to come up with money, forced sales. If you have gold, when these opportunities present, you are gonna be able to convert your gold into not, we’re not talking about handbags, but you’re gonna be able to convert this gold into income producing assets so that on the whole other side of this mess, you come out better because you’re not in a position to have to sell forced sales, corporations are in that position. Individuals are in that position and maybe even the government is getting in that position. But you are going to be in a position to take advantage of these opportunities and they’re coming and they’re coming quickly.

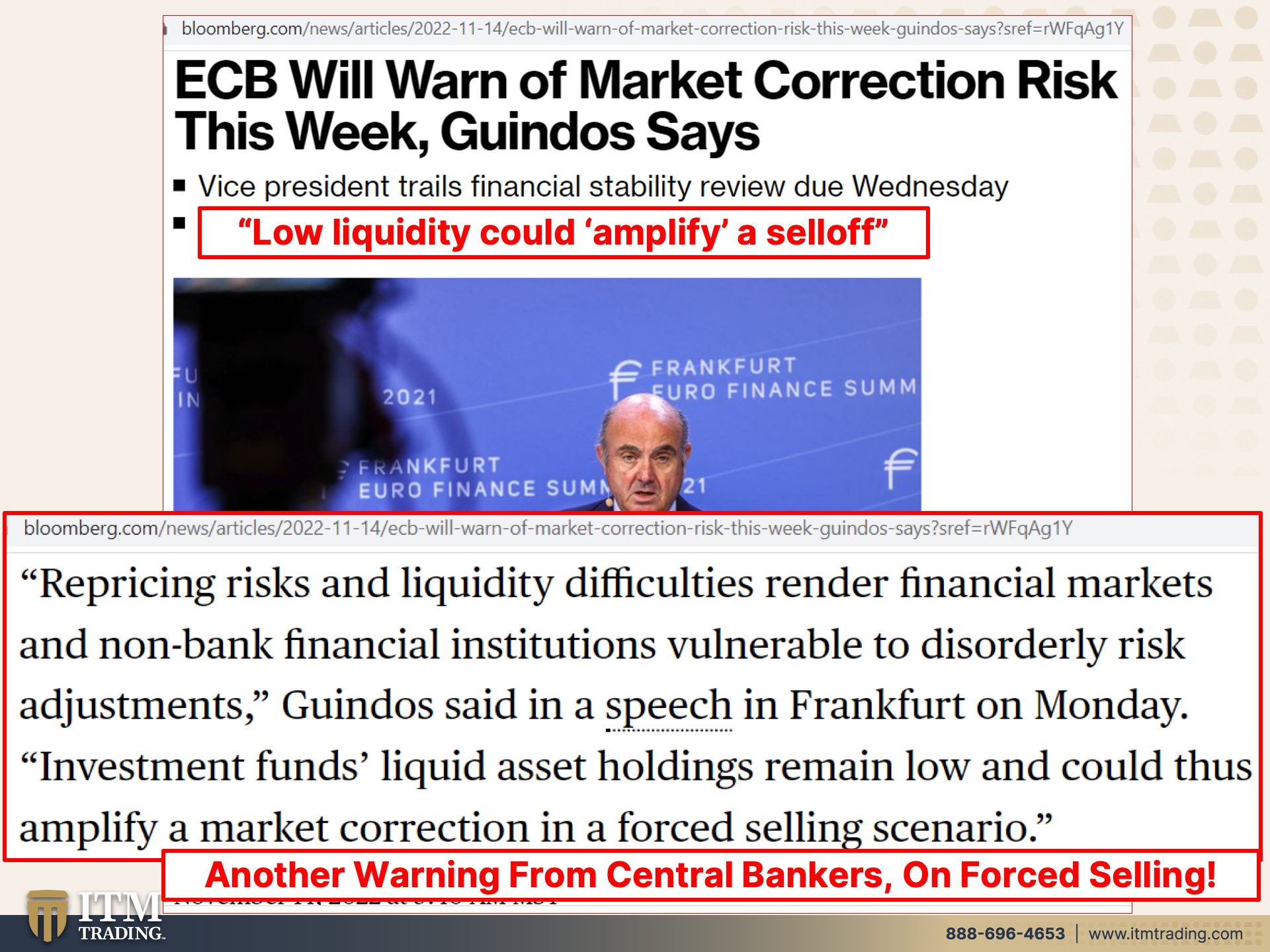

Even the ECB, now we are getting so many warnings from the central bankers primarily and from governments. Excuse me, I’m getting excited about this because I’m able to show you in real time that the opportunities are now at the beginning of this. That’s why you gotta have this. ECB will warn a market correction risk this week. The Vice President trails financial stability review, Wednesday. So you’ll be seeing that tomorrow. But what they’re talking about is low liquidity could amplify a selloff. With all the central banks having done this. Well with all the central banks printing massive amounts of money, how could there be this lack of liquidity? Maybe because rather than taking advantage of it and retiring debt and getting in a position or turning around. We’d certainly know central banks have been buying more gold than they ever, ever have just through the third quarter of this year, they’re getting in a position to buy up those assets. And we also saw a huge jump in bar and coin demand, up 36% year-over-year. So those people that have positioned into gold, I mean, okay, here’s my hesitancy. This is where you’re hearing my hesitancy. I don’t think they’re gonna let you have that opportunity with bullion, which are those new coins and the bars. That’s why I only do the collectibles and you guys know that if you’ve been watching me, you know that I don’t buy that. But people are trying to do the right thing and people are trying to get in the position. So that number one, the wealth that they’ve already managed to accumulate remains intact. And then number two, so that you can take advantage of these opportunities as they present. Okay, let’s go back to the slides now because re-pricing risks and liquidity difficulties. So repricing risks means the markets go from here to here, okay? And liquidity difficulties render financial markets and non-bank financial institutions vulnerable to disorderly risk adjustments like Black Monday in 1987, let’s see, investment funds. So we’re talking ETFs which don’t have to hold a lot of cash. Typically mutual funds. So investment funds, liquid asset holdings remain low and could thus amplify a market correction in a forced selling scenario. Because if you bought all this crap on debt margin debt or any other debt and the market goes against you, the market drops. Well, you got a marketing call. You’ve got to come up with cash. And so what do you have to do? You have to sell off some of your holdings. And then that pushes the markets down even more. That’s that feedback loop. So you have to sell more and there you go, you’re in trouble. But make no mistake, I mean, the fact that they keep warning us that there might be forced selling is telling you that that’s what they expect to happen. They expect a market crash to happen. Now, what will happen to spot gold when the market crashes? Spot gold will most likely sell off. But what will happen to physical gold, those premiums are gonna get bigger and bigger and bigger. This is what’s gonna save you. So if you haven’t started to build that position, click that calendly link below, get yourself into a position to whether this storm because inflation impacts everybody, including the gold industry.

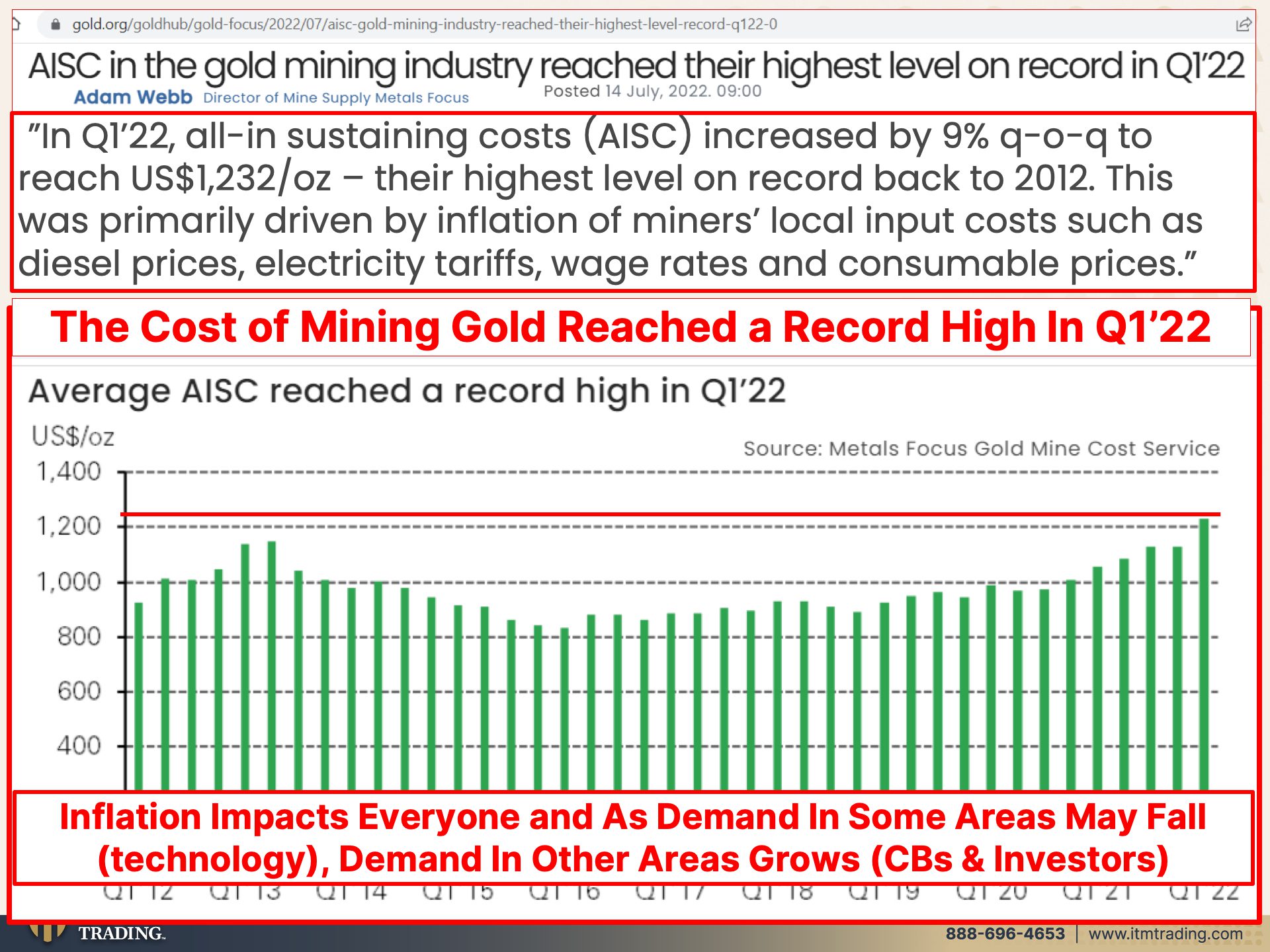

So AISC is all in sustaining costs. So it’s the cost to mine gold and it increased by 9% quarter over quarter. That’s a lot 9% quarter over quarter to reach $1,232. Their highest level on record back to 2012, this was primarily driven by inflation of minors, local input costs, so workers costs, but also diesel prices, electricity, tariffs, and consumable prices. And this is actually higher than going back there. I don’t know where they only went back to 2012. I’m gonna look at that more deeply to see where we’ve ever had this level of cost. It also may put a floor underneath gold spot because it may not because those are just traders and there’s as many contracts as they wanna create to suppress the price. But don’t be fooled. That’s, I guess my point in this because the markets are very, very fragile and forced liquidations are really a big deal if you’re holding those fiat money products. And we don’t know who’s gonna survive that yet. But what we do know is that inflation is not going away anytime soon. And it’s not like a price goes up and then it comes back down. It typically it, the whole system’s based on never ending compounding inflation. But the problem is we’re at the end and that’s why we’re getting all of these funny results. And that’s why we’re getting, that’s why the system is so fragile and also why we’re getting all of these warnings. Inflation impacts everyone and as demand in some areas may fall, and I’m talking about gold here for a minute, like in technology, because people aren’t spending the money on those iPhones or what have you, demand in other areas grows central bankers most gold in history and investors up 36% year over year. So I believe that what we’re now witnessing is the flight from fiat to real safety.

Where do you wanna be in this? I wanna be holding this. I sleep well at night. I don’t worry about what happens in the markets other than to tell you what’s happening in those markets. So make sure if you didn’t watch this yet, you absolutely a hundred percent. And if you watched it once, maybe you watch it again, the video, last week’s video on treasury liquidity. I cannot emphasize enough how important what we’re talking about is this is the foundation, when your foundation crumbles, your house is going to implode. Also, make sure that you visit BGS Beyond Gold and Silver with my interview with Marjory Wildcraft, which will go out next Monday. And we talked about, I thought we were gonna talk about growing a medicinal garden, and she pointed out quite brilliantly that we already have a medicinal garden growing right outside your door. So very, very important because when those pharmacy shelves go bare, you still need to be able to take care of your family and preventative, etcetera. If you like this, please give us a thumbs up. Make sure you leave a comment, make sure that you share, share, share. And if you haven’t subscribed yet, good time to do it right now. And until next we meet. Please be safe out there. Bye-bye.