BREAKING NEWS on Silicon Valley Bank Collapse | with Lynette Zang

What’s really happening behind the scenes of the banking system? Well, you won’t want to miss this. Lynette Zang, is here to reveal the truth about this financial crisis we are living through. With the collapse of SVB Bank, the dominoes are falling, what’s going to be next and why should you care? Get ready for an eye-opening discussion about the unintended consequences of the banking system and how to protect your assets. Don’t miss out, stay tuned!

CHAPTERS:

0:00 Breaking News

3:03 SVB Collapse

7:39 Derivatives & Leverage

15:42 Bailout

20:40 DIF Reserve Ratios

25:00 Banks Are Interconnected

36:18 Doff-Frank Act

42:14 SVB Bonds & Cryptocurrency

48:27 Subscribe + LIVE Q&A

TRANSCRIPT FROM VIDEO:

Well, they did it first. The Fed created the foundation for the next crisis by holding interest rates at zero for more than a decade. And then they started raising rates until something broke. And now the dominoes are falling. What’s gonna be next? Let’s talk about that, coming up.

I’m Lynette Zang, Chief Market Analyst here at ITM Trading of full service, physical, hold it, own it. What are we? A gold and silver dealer specializing in custom strategies and, boy, I sure hope you guys out there have taken advantage of the strategy because is this the Lehman moment? Maybe. I mean, you can see all the crap I have on my desk. Didn’t get very much rest this weekend as this crisis starts to unfold. But let’s just start right here.

This is a graph on spot gold. This is just the contract, and we know that it helps us in adverse circumstances and oh so many things. But just as a reminder, listen to this

Should be accessible when people need to know, but I don’t think you have much hope of, of reaching a public that doesn’t have a professional need to know. I completely agree with that. I almost think you’d scare the public <laugh> if you put this out. Like, why are they telling me this? Should I be concerned about my bank? Like my insurance company doesn’t tell me what they’re doing with my assets, they just assume they’re gonna pay my claim, I think you’ve gotta think of the unintended consequences of taking a public that has more full faith and confidence in the banking system than Navy. People in this room do <laugh>. They, we want them to have full faith and confidence in the banking system. They know the FDIC insurance is there. They know it works. They put their money and they’re gonna get their money out. So there, there’s a select crowd of people that are in the institutional side, and if they wanna understand this, they’re gonna find a way to understand this. There’s a bunch of law firms representing this room. There’s a bunch of people that’ll charge ’em by the hour. A lot of money to explain this all to ’em and, and, and, and it’s fine. And I, I don’t have a, I don’t have a problem with that. And they all have huge staffs, but I would be careful about the unintended consequences of starting to blast too much of this out in the general public.

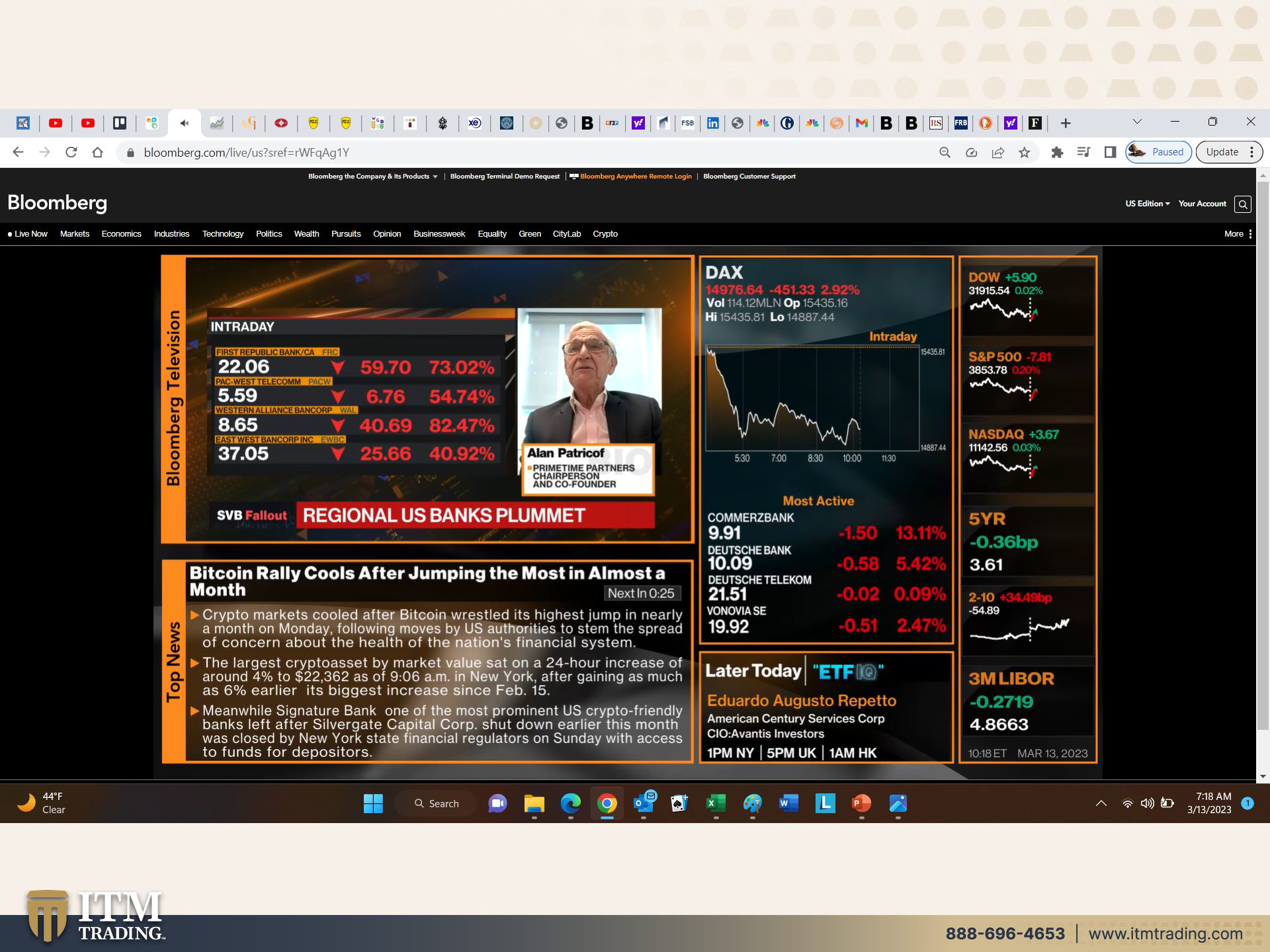

So, okay, we all know that SVB Bank failed and then another bank failed over the weekend.

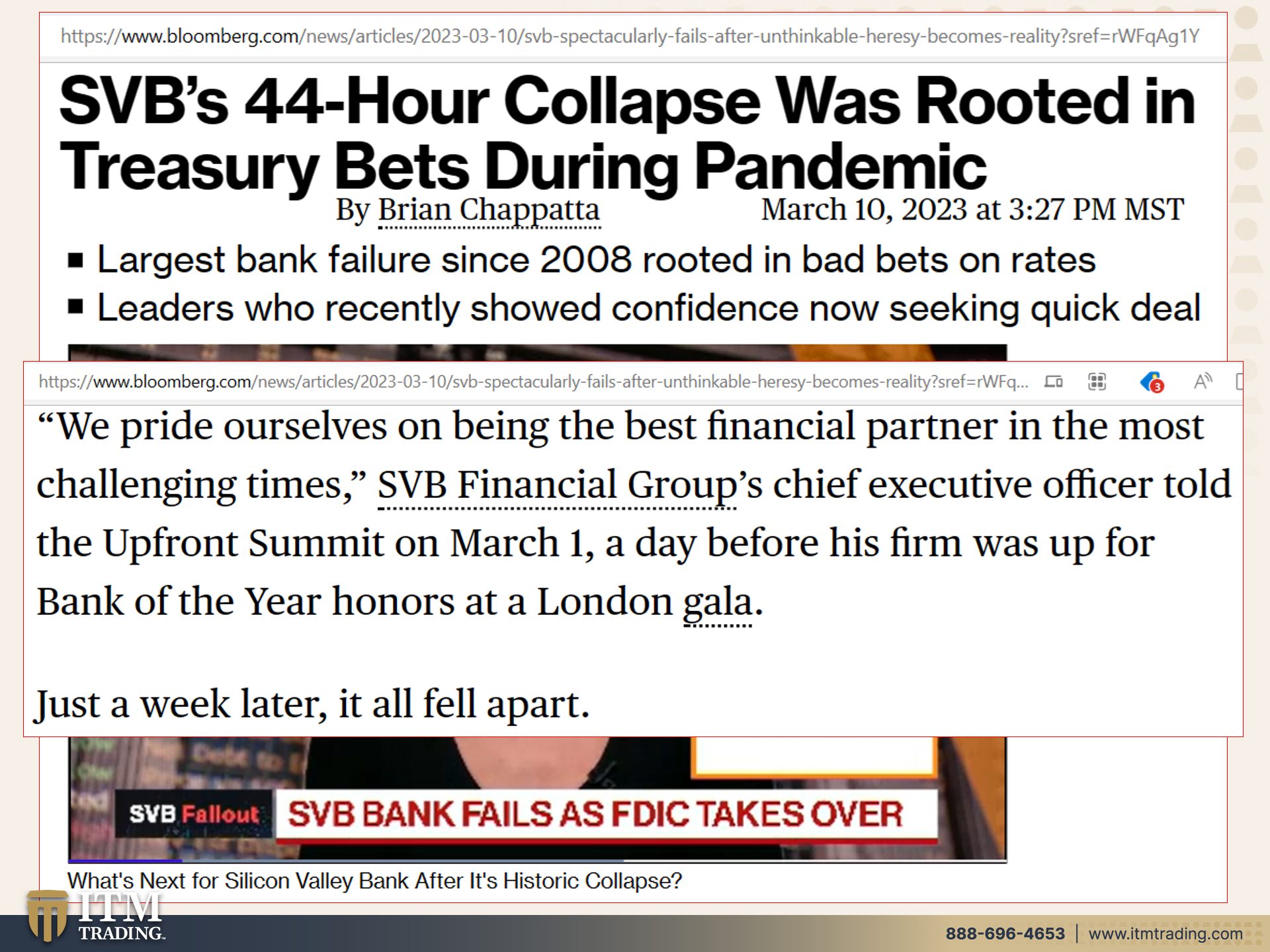

But let’s just take a look at how and what made that collapse happen. And you might recall that we’ve talked about this before. This is interest rates. This is the principle value of the bonds as the Fed has been raising rates. The principle value of the mortgage backed securities of the treasury bonds of all other debt instruments that they hold goes down. So when they say SVBs 44 hour collapse was rooted in treasury bets during the pandemic, that means buying treasuries, buying mortgage backed securities, near 0% interest. And then, okay, interest rates go up. Largest bank failure since 2008, rooted in bad bets on rates. So really what is happening in the, and I’ve asked this question many times in this opaque arena, what’s happening with all those derivative bets most of which were on interest rates.

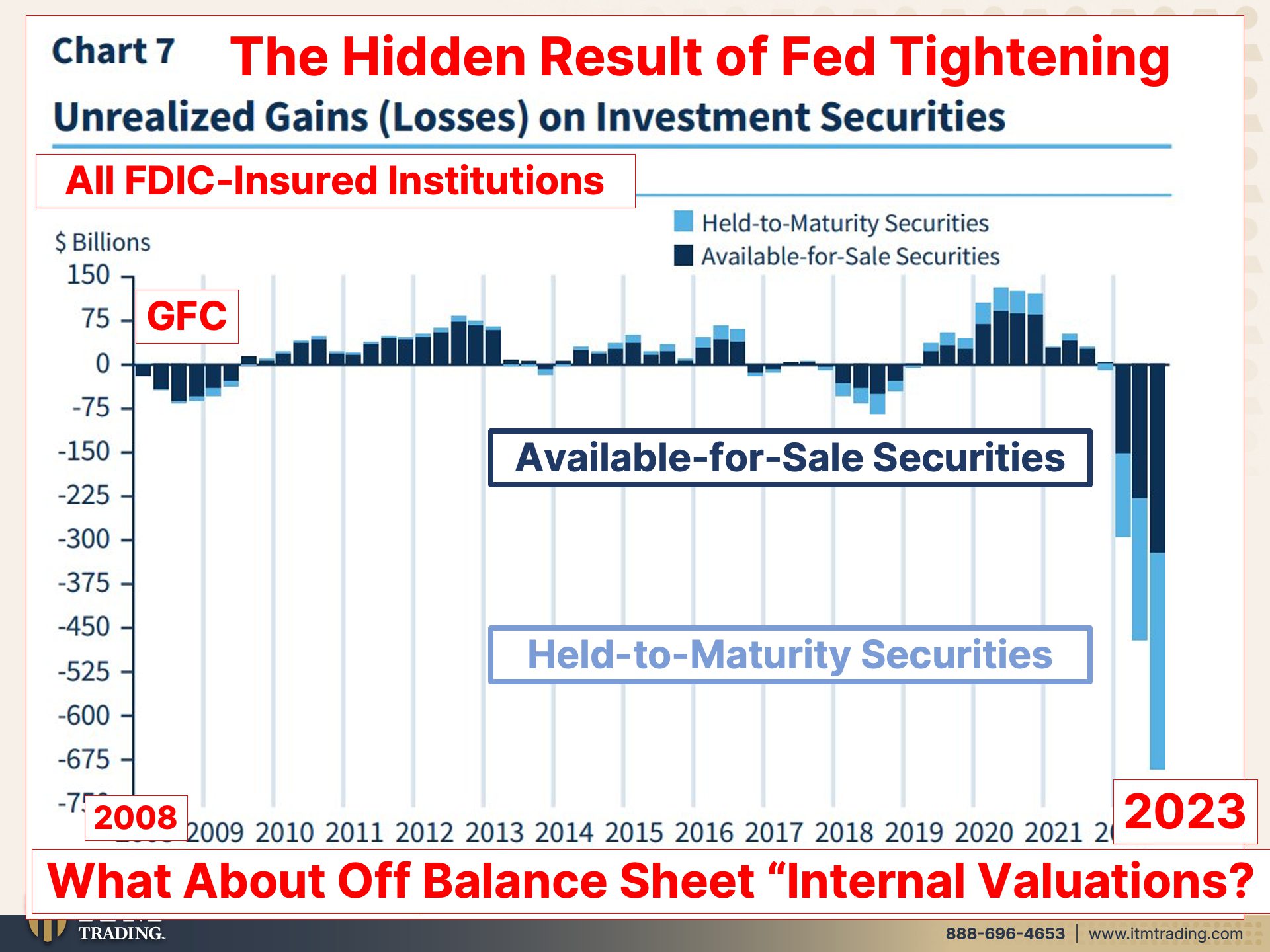

I mean, there’s a lot that’s happening that we can’t see, but March 1st, we pride ourselves on being the best financial partner in the most challenging times. SVB financial group’s Chief Executive told the upfront summit on March 1st, a day before his firm was up for Bank of the Year honors at a London Gala, just a week later, it fell apart. Do you trust them in physical gold and silver I trust I worked in that belly of the beast. I know how disgusting and convoluted it is. But if you think that this is just relegated to regional banks, oh, no, no, no, no, no, no. This is what they’re talking about. Unrealized gains, losses on investment securities, which they have two categories because this is the hidden result of all of the Fed tightening. This is only part of it, honestly, this is only part of it. You can’t find a whole lot on what’s happening in derivatives right now. But these are all FDIC insured institutions. What are you worried about? They’re insured. Well, we’ll talk about that in just a second. This is how bad it got in 2008 during the great financial crisis. This is where we are in 2023. It’s a good thing. We’re not going through a financial crisis. We’ve been look at, consumers have been good, everything’s been good. Everything could weather these increase in rate hikes until they can’t. So this dark blue is the available for sale securities, which means that the banks will, can sell these securities at a loss when they have to raise capital. And when that happens, it pushes the value of all of those other instruments down more. Okay? Now this area is the, this lighter blue is held to maturity securities. So those are on the books at par. They don’t really reflect that undervaluation, can you see the problem? Because these are all FDIC insured institutions. And what none of this really actually even reflects is the off balance sheet internal valuations, which I’ll talk more about in the, this coming week. But I’ve talked about it quite a bit in the past where banks will create their own formulas for valuations. Great. So how in the world do you know as a depositor, as a lender to the bank, because that’s what you really are. Remember, once you deposit that money in, you’ve loaned it to the bank. So how can you possibly know if your bank is safe or not? Most of the fallout is happening in the, in the small regional banks at this point. But guess what? Your big banks aren’t any safer. In fact, they’re even more risky because of all of the derivatives that they carry. We’re gonna talk more about this this week.

This week, you know, I mean, if you haven’t subscribed yet, subscribe, because this is when I get to really, really, really do my job. Okay? All right, hit that button. We’ll let you know when we’re going live. Let’s kind of get a little overview of this because SVB bank for 44% of tech IPOs, what do we know about a lot of the IPOs that came out in the zero interest rate environment? They didn’t have to make any profits. They could just burn through all that cash that they raised like crazy. Well, now it’s coming home to roost. Who couldn’t see that coming? I mean, come on. Who couldn’t see that? Used by private equity portfolio companies, mortgages to tech elites and conduit to Chinese tech. So essentially what you’re looking at is incestuously interconnected in every segment of the global economy. I’m gonna show you more about that Credit Swiss default swaps. So that’s a derivative hit record as SVB Royals Banks. But Credit Swiss was already in trouble, weren’t they? And now their derivatives are hitting new records. Well, my bet would be that derivatives in all of these banks are hitting new records, but the guys that create these monsters, Warren Buffet said it. He’s not my favorite, but he definitely said this. Financial weapons of mass destruction, I said it before, I’ll say it again. This is what’s going to topple the system and overwhelm the government’s and the central bank’s ability to bail anything out. And we’re gonna talk a little bit more about that.

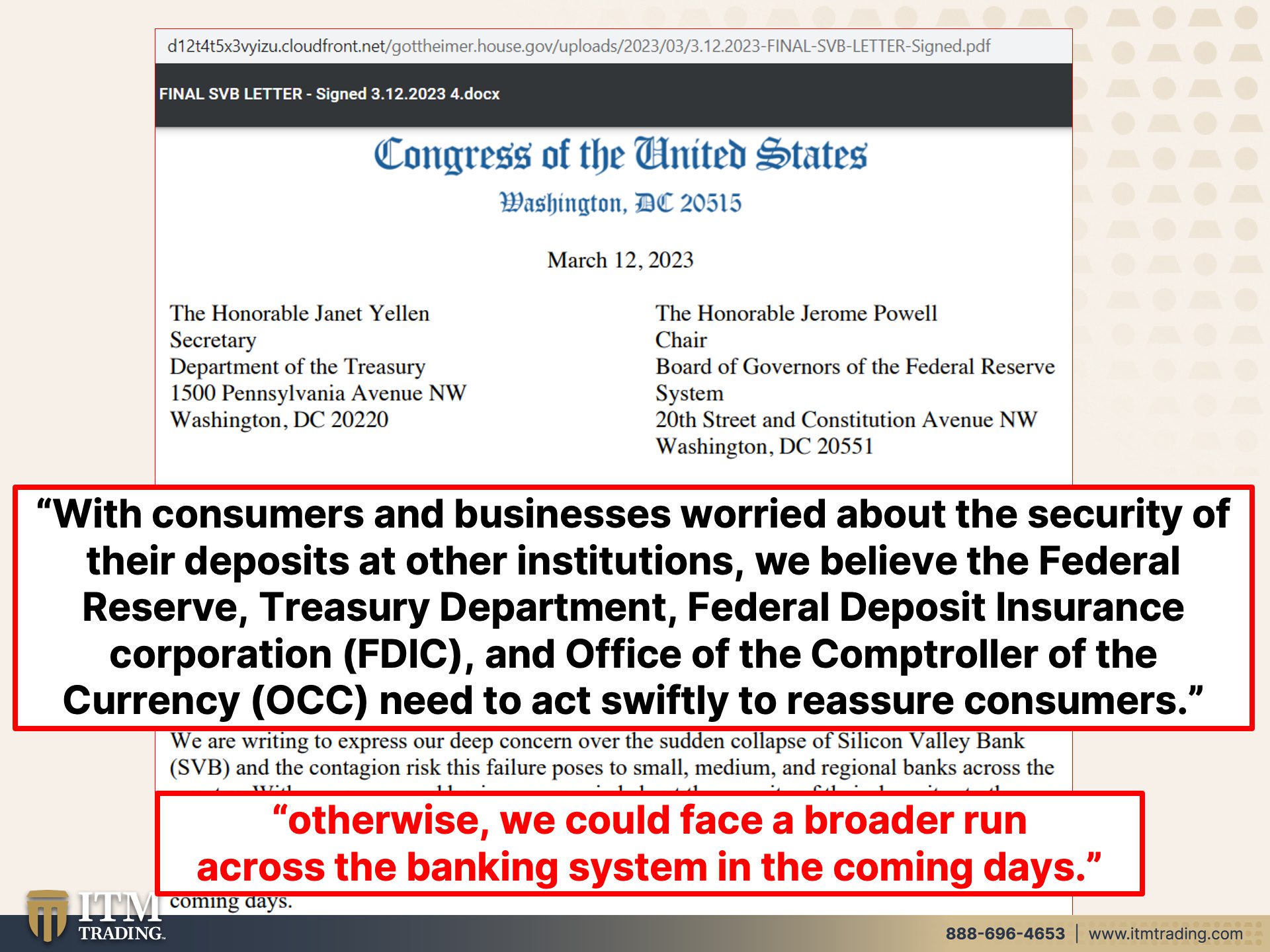

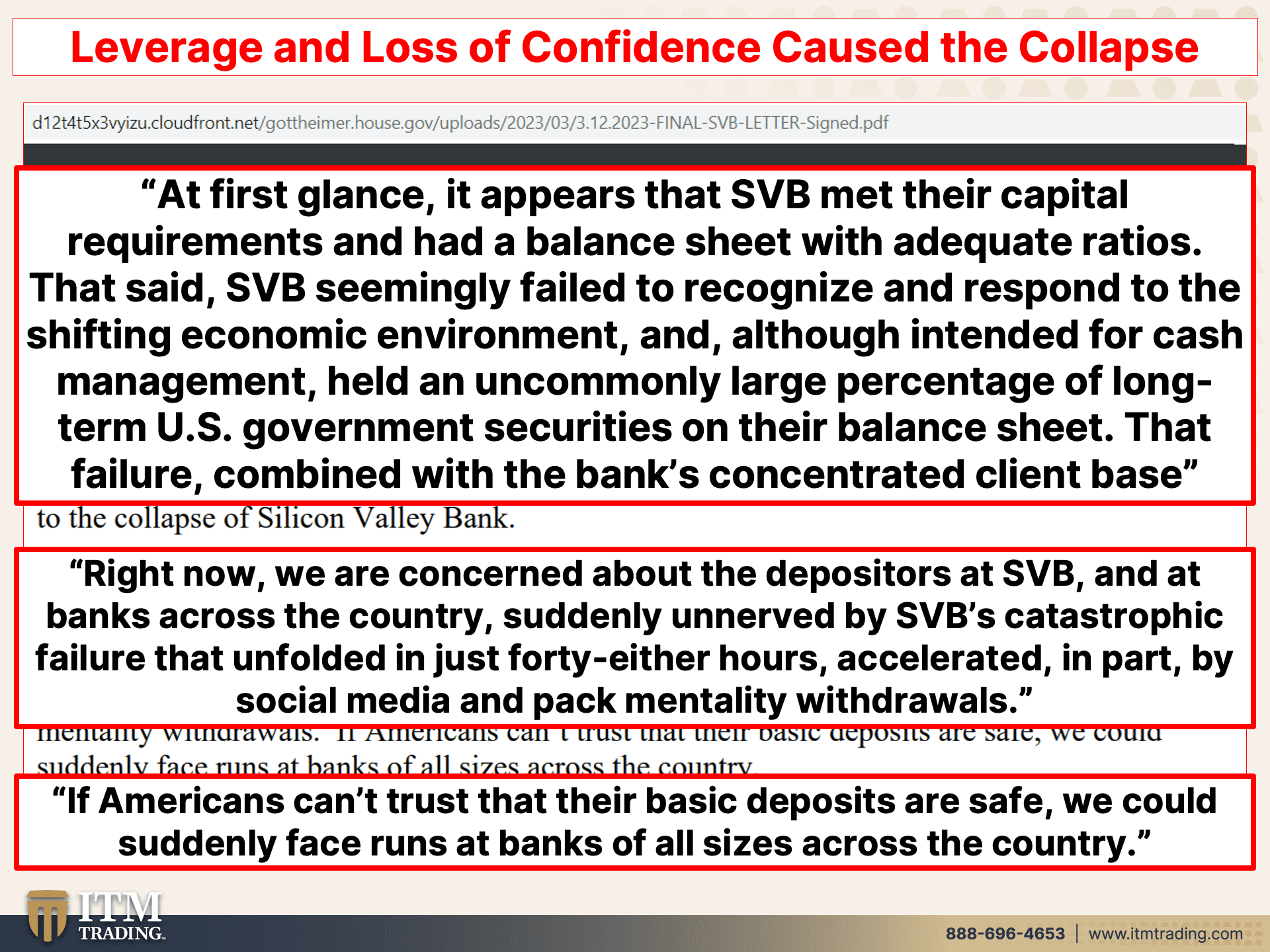

So in the meantime, members of Congress yesterday went to the FDIC, the Treasury secretary, the, let’s see oh, the OCC Office of the Comptroller of the Currency and the Federal Reserve begging them with consumers and businesses worried about the security of their deposits at other institutions. We believe the Federal Reserve Treasury Department, federal Deposit Insurance Corporation and office of the comptroller of the currency need to act swiftly to reassure consumers. Otherwise, we could face a broader run across the banking system in the coming days. And just as a reminder to you guys, remember, I have links to all of this that you can access and read everything for yourself, but it’s leverage and loss of confidence that caused the collapse, right? And leverage means debt upon debt upon debt. And once they instituted after the great financial crisis in 2010, they passed the Dodd-Frank Law and they didn’t even write all of the laws in before they started to dismantle them again, allowing, we’ve talked about this more and more and more leverage, and therefore more and more and more risk inside of the system. And you know, those, those reports that they would do annually on the banks garbage, I told you it was garbage at first glance, it appears that SVB met their capital requirements and had a balance sheet with adequate ratios that said SVB seemingly failed to recognize and respond to the shifting economic environment. Yeah, rising interest rates. So do you think anybody else, any other banks or any other firms that are sitting on large amounts of treasury bonds, which is supposed to be the safest thing that you could do until it’s not? And we’ve also been talking about the lack of liquidity in the treasury bond market that began to rear its ugly head in 2015, but it was already in 2002 that the Fed started buying treasuries from our government. So this is a long-term brewing and understand everything goes slow, slow, slow. It seems like nothing’s happening, although there’s tons happening underneath the service until it happens quickly. And although intended for cash management, that’s what they were using, the treasuries for cash management held an uncommonly large percentage of long-term US government securities on their balance sheet. That failure combined with the bank’s concentrated client base. So let me explain this right here are interest rates. This is when the bond is issued, right? Okay? When interest rates go up, the value of the bonds go down. But you can see that the further out to maturity, the longer duration bonds move a whole lot more than the shorter duration bonds. So what they’re talking about, and this is something else we’ve been talking about for a number of years, is the liquidity mismatch. If this was supposed to be intended for cash management, so hey, you wanna go into the bank and pull out your cash, they wanna manage how much cash they’re holding in there, then why would you do the longer dated securities? Seems to me like you do the shorter dated securities and also the shorter dated securities. You know, again, I can’t emphasize this enough, right? You’re still gonna get movement when the rates rise. But that movement, especially if if you’re in three and six months, is a much a whole lot less volatile. Now look, I am not telling you to go out and buy treasuries of any maturity. Let’s get that clear because that’s a debt instrument and it should be pretty clear to you how fragile and vulnerable this system is. In fact, is this a Lehman moment? Maybe, maybe if they can get the population to buy into their garbage, but what a huge knock this has been to the confidence. And did I not tell you that the last level of confidence is the public to the central bank and the system? Huge knock. Huge. Right now we are concerned about the depositors at SVB and at banks across the country, suddenly unnerved by SVB’s catastrophic failure that unfolded in just 40, oops, looks like I missed a word, but 48 hours accelerated in part by social media. Don’t know about it. If you don’t know, you don’t react. Go ahead, just watch the Emmy’s or Grammy’s or whatever Oscars that were on last night. Far more nothing to see over here. Just watch those Oscars by social and pack mentality withdrawals. So you have fear of missing out on the way up, pushing all of these tech stocks in the stock market higher. And guess what you have now? You have just the reverse. This is a PAC mentality, right? And, and on the way up, it’s a lot of fun on the way down. It’s not so much fun. And that’s where we are at the moment, except, well, not at this moment. I’ll, I’ll show you in a second. If Americans can’t trust that their basic deposits are safe, we could suddenly face runs at banks of all sizes across the country. All right, now I’m going. You, you see I have a lot more stuff on my desk because of everything that’s happening.

So this is from Bloomberg. I get it every day. Good morning. And let’s get you up to speed on the Silicon Valley Bank crisis. The US is backstopping bank deposits. So 2008, what’d they do? They went from a hundred thousand to $250,000. And what do most people say? Well, it’s insured. Hmm, okay, it’s insured. We’re gonna talk about that in just a minute. Bear with me. But backstopping a hundred percent of all banking deposits at this point. Is that going to stick moving forward? Like the 250 was just supposed to be temporary? No. And I hope you got your money outta money markets cause we know they’ve been changing those rules, but markets are seeing some relief after U.S. Authorities took extraordinary measures to shore up confidence in the financial system. Here’s the latest. SVB’s Depositors will be able to access all of their funds. So insured plus uninsured as of let’s see of their funds today. US Authority said the Fed also announced a new bank term funding program. Just create a new program. What are you worried about? We got your back. Oh my God. That offers one year loans to bank under easier terms than it typically provides. So remember all of these under, oops. Underwater principles. They can take those mortgage backed securities and those treasuries to the bank and they can borrow as if they’re at a hundred percent Gee, but don’t call it a bailout. Don’t call it a bailout. It’s not a bailout. We’re not gonna bail ’em out again. Well, I don’t know rose by any other name. We’ll keep going. You’ll see. In New York state authorities closed Signature Bank and said that all depositors there will also have access to their money with a senior treasury official cautioning other banks appear to be in similar situations. Ya think? We’re gonna gonna be talking more about that this week. Regulators top concern is assuring businesses and households, don’t worry, they’ll be made whole on their deposits at the two banks and actually all banks because everybody’s worried about their deposits no matter where they are. And in fact, this is an email from a client of ITMs and she says:

I wanted you guys to know about something that happened this afternoon. I had already made the decision to get my money out of the small local bank in Lafayette, California, but had been lazy about it. After seeing Lynette’s broadcast today, I wrote a check from that bank to deposit into my Chase account, which I set up because at some point Lynette said that that’s the big bank she would use if she had to. The chase ATM took my check and spit out the following receipt, notice of delayed deposit, availability amount delayed, blah until 3/21/23. This is dated Friday, March 10th, 3/21/23. Checks within this deposit may not be paid because of information we’ve received from the paying bank or due to information we have within our files. Further review may result in delayed availability of this deposit. Yep. They know what’s coming. The little guys are folding. It’s the little guys. And I’m not talking about the little banks as much as I am the general public, we are always the one to eat it because we are the ones that are not too big to fail. The little guys are folding in the meantime, I would have most likely been screwed in terms of access, whether I had left them in the original bank or did what I did. Ah, yes. The one second too late syndrome. How many years I’ve been been telling you I would rather be 10 years too early than one second, too late. And so what did the, what did the regulators do? They went in and they said, okay, we are gonna cover all deposits a hundred percent of all. So you have nothing to worry about except you can see the system’s fragility. I’m afraid to blow on this because this would topple, but we are inside of a Jenga economy. Is this the one, is this the one truthfully that topples the whole system? See why I couldn’t fire Edgar the other day? Because he’s gotta pick up all this mess from me. <Laugh>, he’s laughing, but it’s and you gotta laugh a little bit because you know, I, is this a Lehman moment?

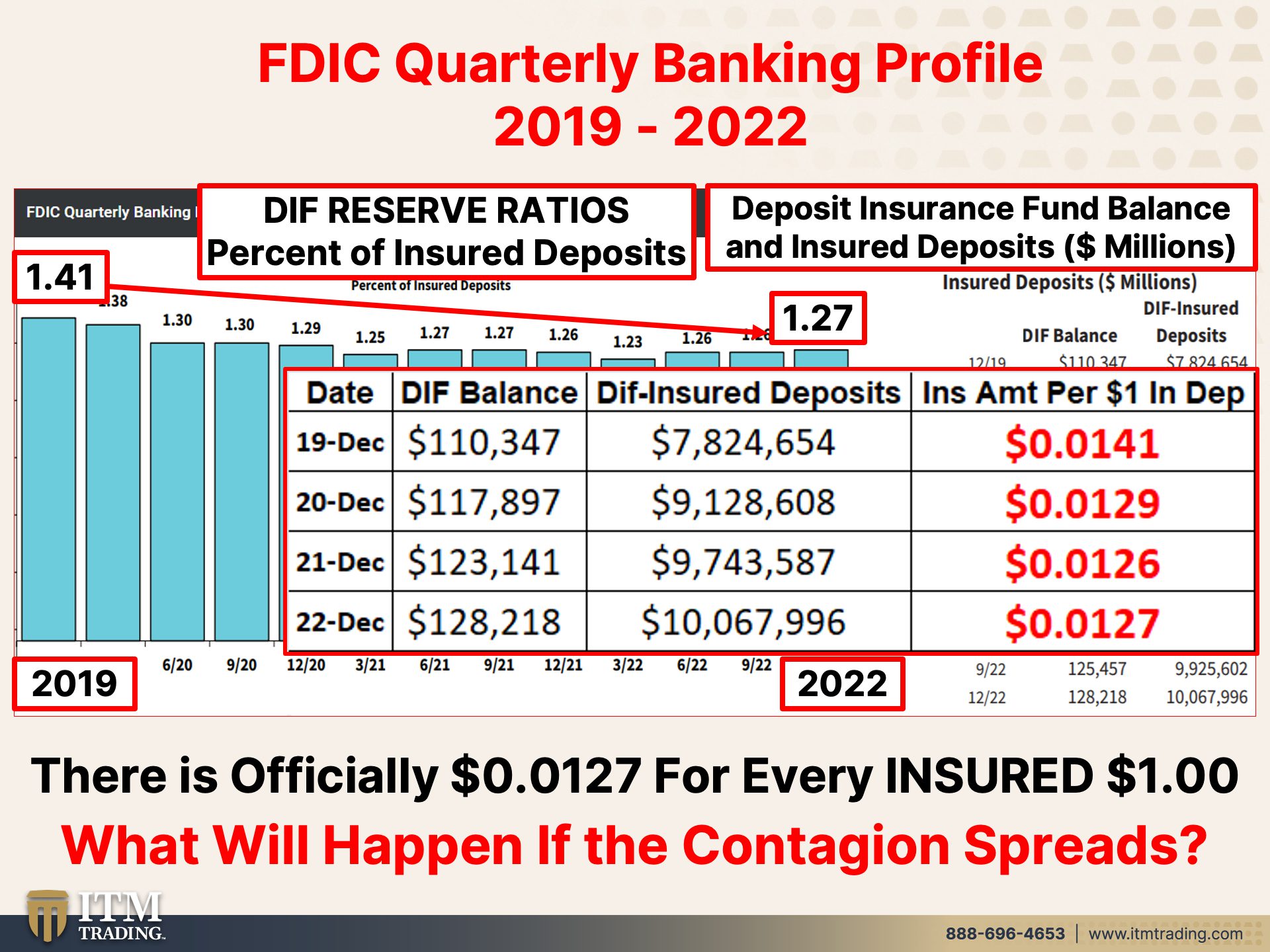

So now let’s take a look at where that money’s coming from because what they’re saying is this is not a bailout because we aren’t gonna ask taxpayers for it. Hmm. Okay, well this is the most current FDIC quarterly banking profile. And this is the DIF report. So this is how much they have inside of the deposit insurance fund to pay for insured deposits. And apparently now uninsured deposits. This is where this money’s coming from. This is the DIF reserve ratio, which is a percent of insured deposits. So let’s take a look at this. This goes back to 2019. This is as this is, was right from that report. And they had, I know it. That’s 1.41%, okay? To ensure all of the insured deposits. So all those deposits underneath the two 50. Now this is through 2022, and you can see that it’s gone down to a, to 1.27% of all insured deposits. How’s that make you feel? Does that make you feel good In the meantime? This is the balance. How much money they actually have in terms of millions. Okay? So I just took from December so that you could see it in a bigger way. December, 2019, they had 110 billion, 347 million to insure $7,824,654 in insured deposits, or $0.0141 pennies. A little bit more than one penny to ensure every dollar you can see where they’re at. And right now, December, 2022, there was $128,218 million to ensure 10,067,996 trillion in deposits or $0.0127. So let’s see. Do you think that it’s possible? I mean, as long as not every bank goes out, right? Are they going to take that money and then use it for the uninsured depositors over at SVB and the new bank that’s gone down? Are they going to use just 128 billion to ensure every deposit in the country had, did they, by the way, did they bring that up when they said, yes, we’re gonna ensure and backstop every deposit in the country, but this is why they’re saying no taxpayer dollars are gonna be used. It’s garbage because the bail-in the bailout. Absolutely. But were they ready to pull the trigger on that yet? I think they were shocked just like they were at the Lehman moment. And you know, that also means that I may be going up to the cabin, but let’s see if they can get the confidence of the public. And maybe this isn’t, but maybe it is. I said there needed to be a really, really big crisis before June 30th. I’ve been saying that. I said 2022 is a pivotal year, and it was in 2023. There had to be a big huge crisis before June. And I’m kind of thinking this qualifies. What do you think? So officially there is $0.0127 for every insured dollar. And what happens if that contagion spreads? Which is what we’ve been seeing. So as a reminder, and Edgar, you’re gonna put this link to this video that I did from an IMF report in, I think it was September or November, something like that, in 2022.

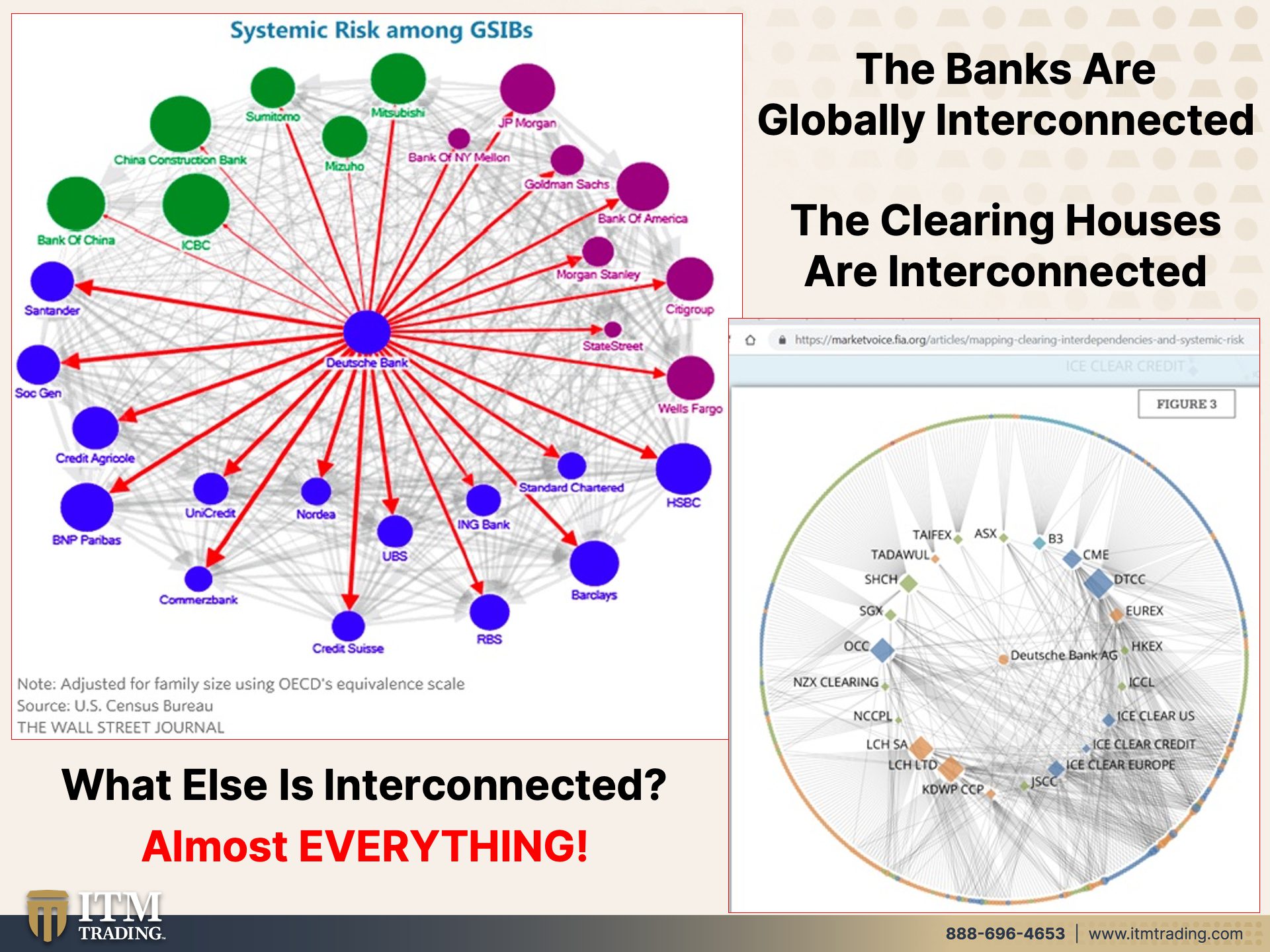

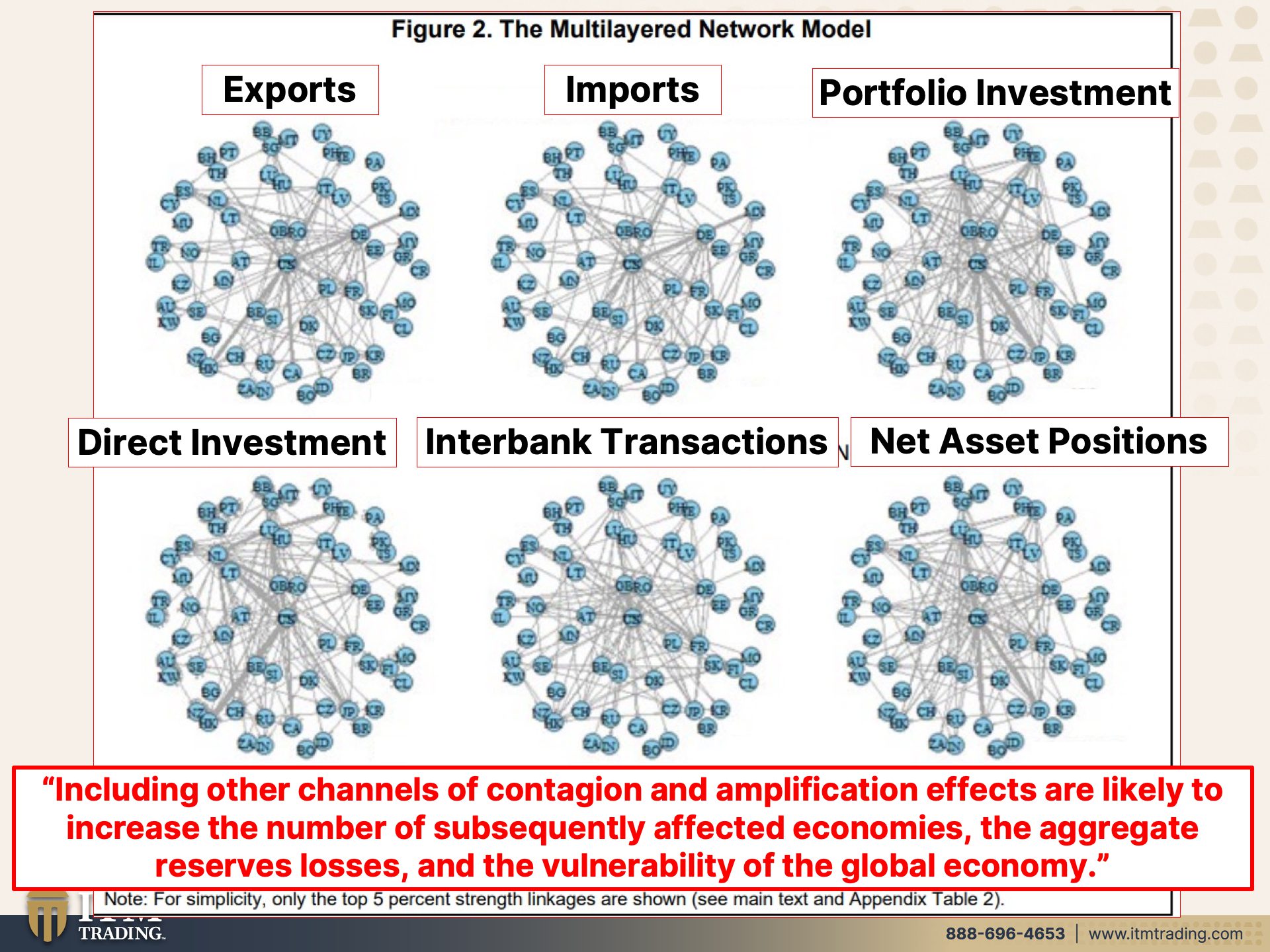

Okay? So you see these, all these little gray lines in between the red and all this. This is the global banking system, systemically important banks. But all these little grain lines are all of the interconnections that we see. So it doesn’t matter where this starts, it royals the entire system. Global banks are incestuously interconnected, and the clearing houses are also incestuously interconnected. So all of those derivative bets that are out there, just go through a few of them and look at this, all that gray, all these lines, incestuously, interconnected. And oh, by the way, that ION hack, which is one of these these clearing houses that ION, from what I can tell, we’re still not getting full reporting. They’re starting to report back February 21st. So all of this trading and all of these derivatives, they’re all happening in the dark, in the freaking dark. You gotta ask yourself how safe you feel, Food, Water, Energy, Security, Barterability, Wealth Preservation, Community and Shelter. I hope you got it done, or at least at the minimum that you’ve got some kind of basis and foundation. But what else is interconnected? Almost everything. Okay. So what we’re looking at here is exports are interconnected, imports are interconnected, portfolio investments, center connected, direct investment, interbank transactions, net asset positions, including other channels of contagion and amplification effects are likely to increase the number of subsequently affected economies, the aggregate reserve losses, and the vulnerability of the global economy. This is from the IMF report. Go back and watch that video. Edgar will make it easy for you and give you the link. This wasn’t that long ago that they did it, but that’s why I said this very well could be the Lehman moment because we are seeing contagion and of course, first they come out, no, no, this is just over there. Oh, don’t nothing to look at. Nothing to look at, move along, move along. We don’t want you to understand what’s really happening.

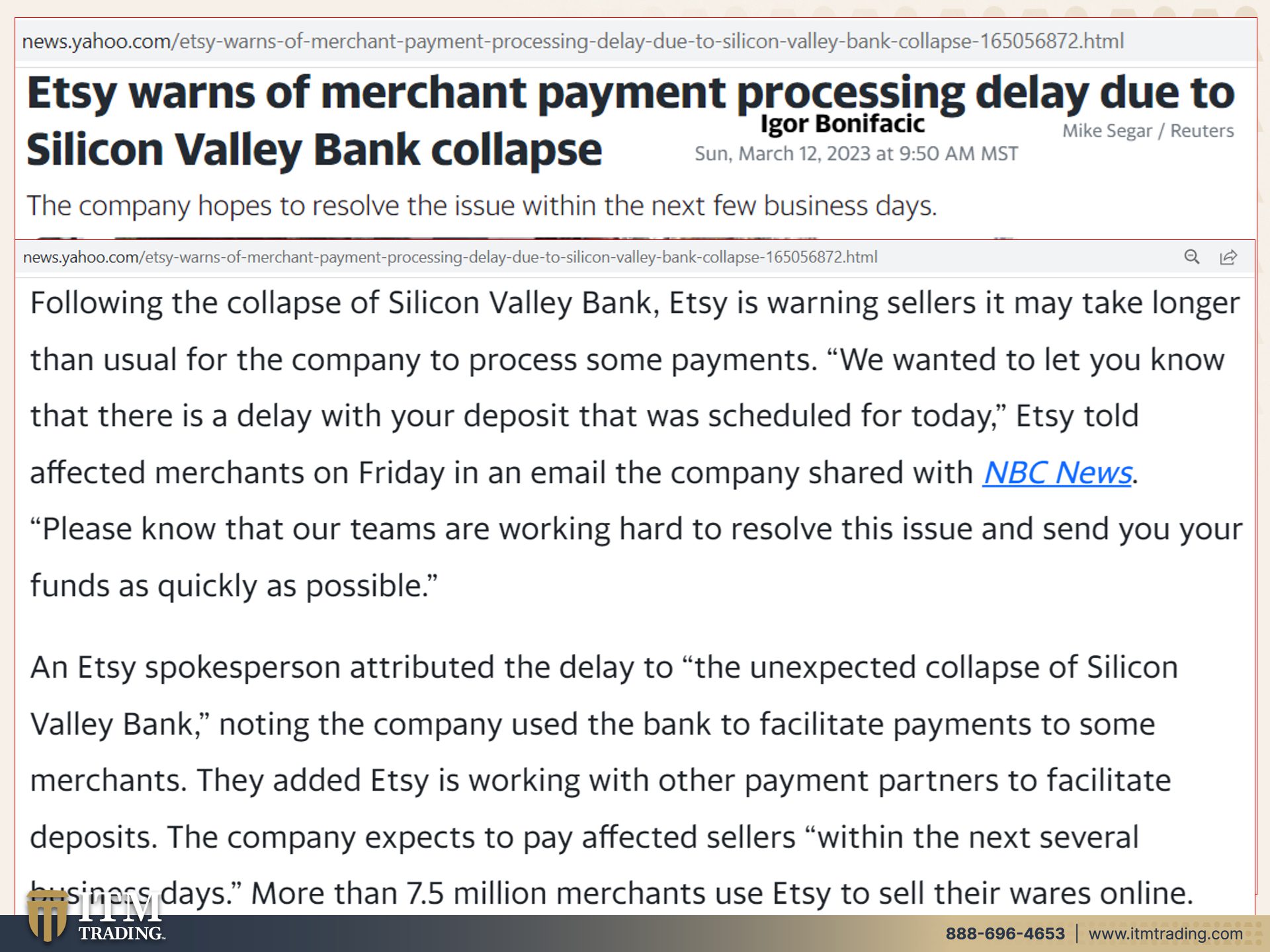

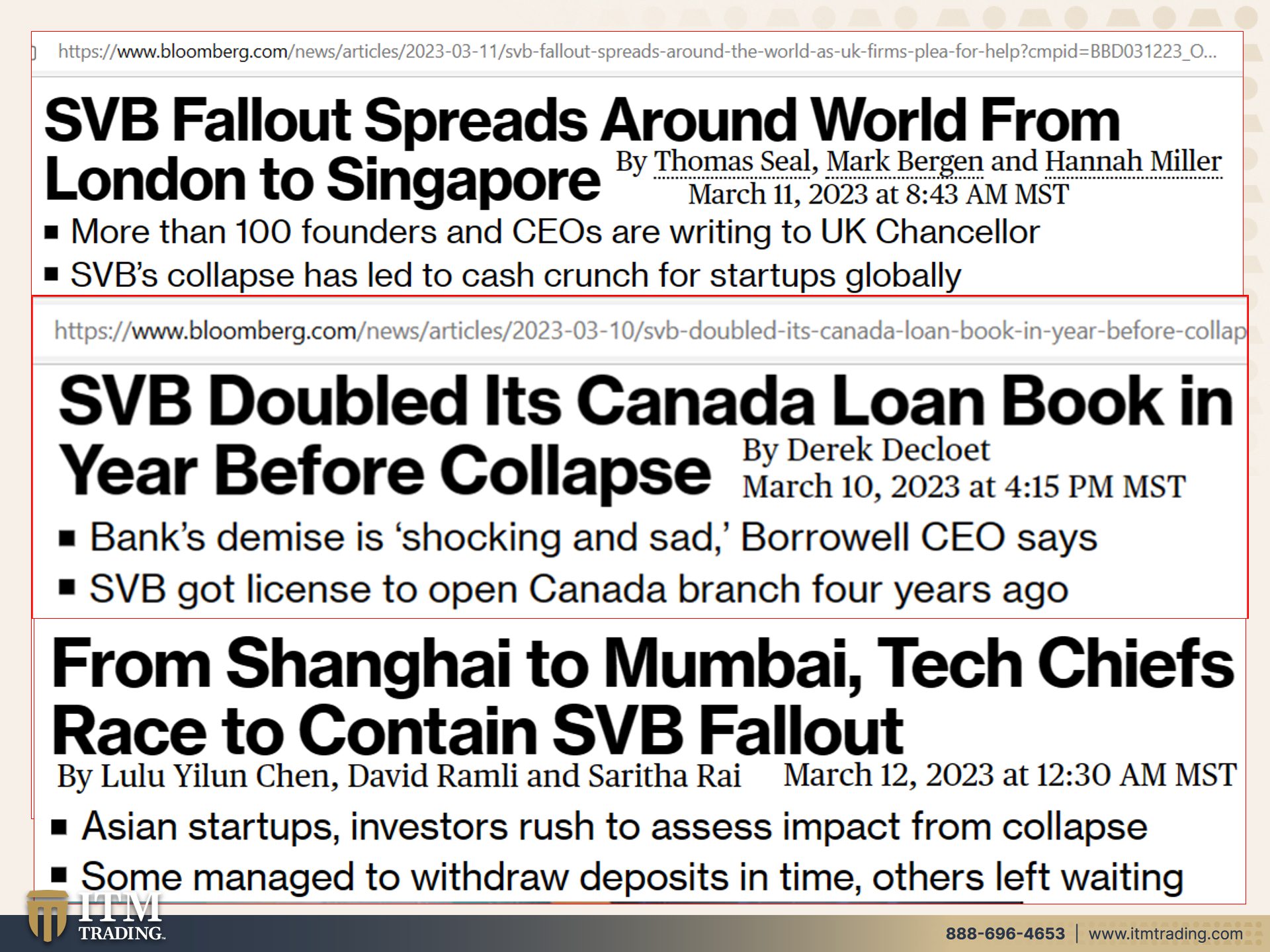

But even for day-to-day people, Etsy warns of merchant payment processing delay due to Silicon Valley Bank collapse following the collapse of Silicon Valley Bank. Etsy is warning its sellers. It may take longer than usual for the company to process some payments. We wanted to let you know that there is a delay with your deposit that was scheduled for today. Now what if these people are counting on those to live? It’s a problem. But please know that our teams are working hard to resolve this issue and send you your funds as quickly as possible. Yeah, okay? And that’s not the only thing. SVB fallout spreads around the world from London to Singapore. More than a hundred founders in c CEOs are writing the UK Chancellor SVBs collapse has led to cash crunch for startups globally and it just doubled its Canadian loan book in a year before the collapse. So there you go, around the world, London to Singapore, from Shanghai to Mumbai, tech Chiefs race to contain the SVB fallout. Can they do it? We’re gonna know this week. Can they do it?

Now SVB’S collapse is a headache for more than 190 firms worldwide. So as I just showed you from the IMF, everything, everything, everything is incestuously interconnected. This is why it is so critical for you to have money, real money out of the system. And how about money they can’t take away from you because they hold it too. If you can hold it in an ira, why are you buying it? That alone tells you it’s in a different classification. I’m sorry cause I can hear myself yelling. Let me take a breath. Let me take a breath. Okay. So treasury yields plunge the most since the 1980s. That is a flight to safety that is freaking insane. You’re jumping outta the, out of the frying pan into the fire. Those treasuries are debt and they’re backed by the ability to grow more debt. Full faith and credit. Are you kidding me here? This no counterpart risk, no counterparty risk. The only financial asset, the only financial asset that runs no counterparty risk. And it’s completely out of the system. It is in your possession and it is real money saves your butts. And even First Republic, Schwab, Pack West, all trading halted. How do they control a run? Boom. You can’t get your money, boo. So sorry. Too bad. So sad. Edgar was telling me earlier that he went to deposit $120 in cash at his And what happened? Would you tell them because you were there, you know it. They gave me a hundred dollars bill back, but kept 20 and now I have to figure out how to get my $20 back because it’s a third party entity that owns that atm. Mm-Hmm <affirmative>. And when you went into the bank to talk to them, how helpful were they? They were like, figure it out, call ’em and they’ll help you out. Too bad. So sad. Who you gonna call? What you gonna do? Let’s see. Yeah. Sweden’s, Alecta set to lose a billion on soured US Bank bet. Yeah, this is flipping global. And look at how fast it’s spread. 48 hours the bank collapsed and now you’ve got all the dominoes that are falling. Emerging markets get whipsawed as SVB woes offset fed repricing swings, gripped emerging markets. Monday as investors were split on the impact of the US banking crisis with some touting lowered expectations for, I love this one for federal reserve interest rate hikes and others fretting over the rush to havens. So let’s think about that for a minute. Okay? The Fed is due to raise rates to fight inflation. Of course, the raising of the rates is what triggered this crisis considering the fact that they got everybody used to such low rates for such a long time, right? So they created this crisis and who couldn’t see that coming? I’ve been telling you forever. They’ve been between a rock and a hard place. We’re at the end. There is no more kicking this can down the road.

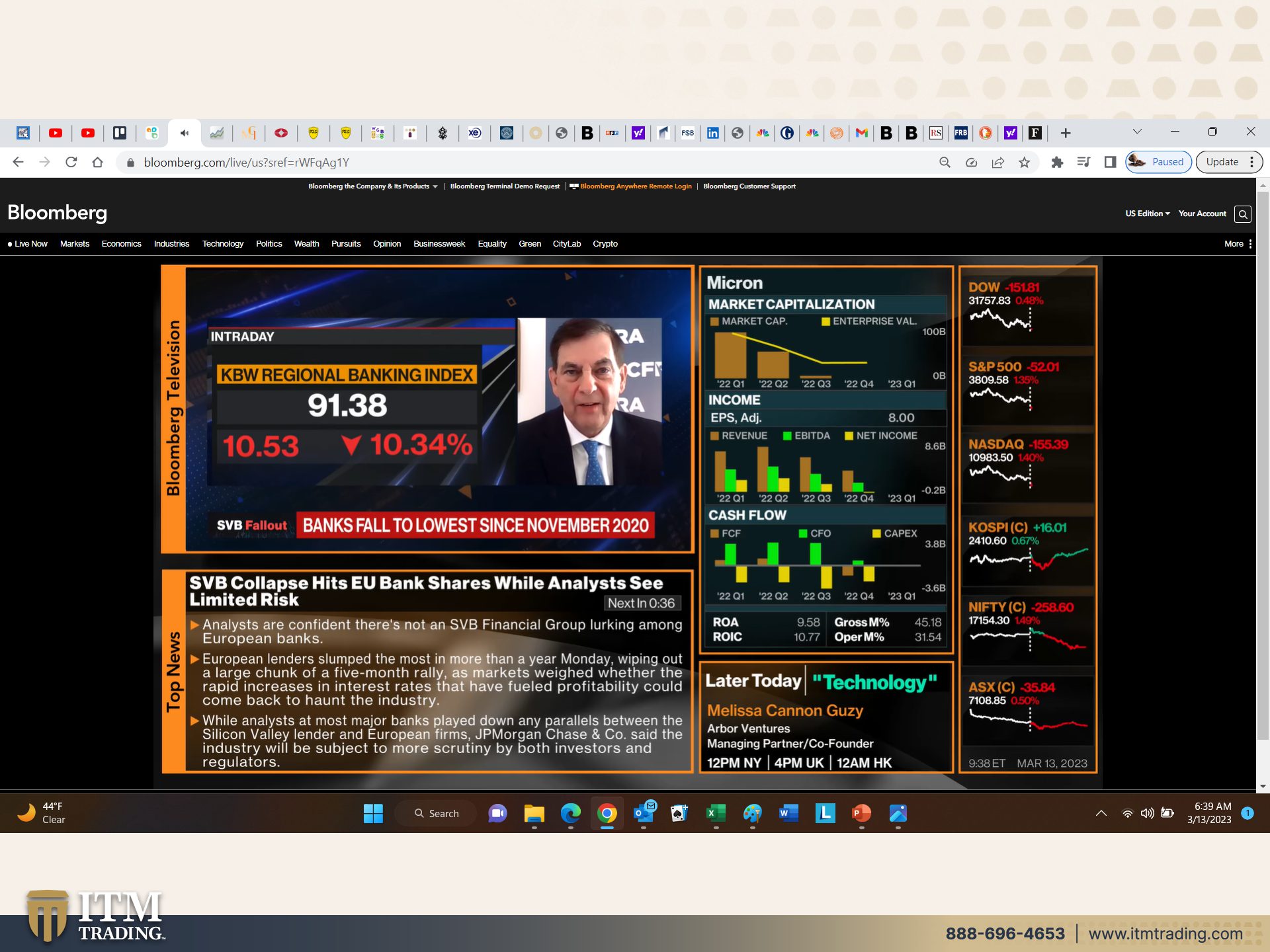

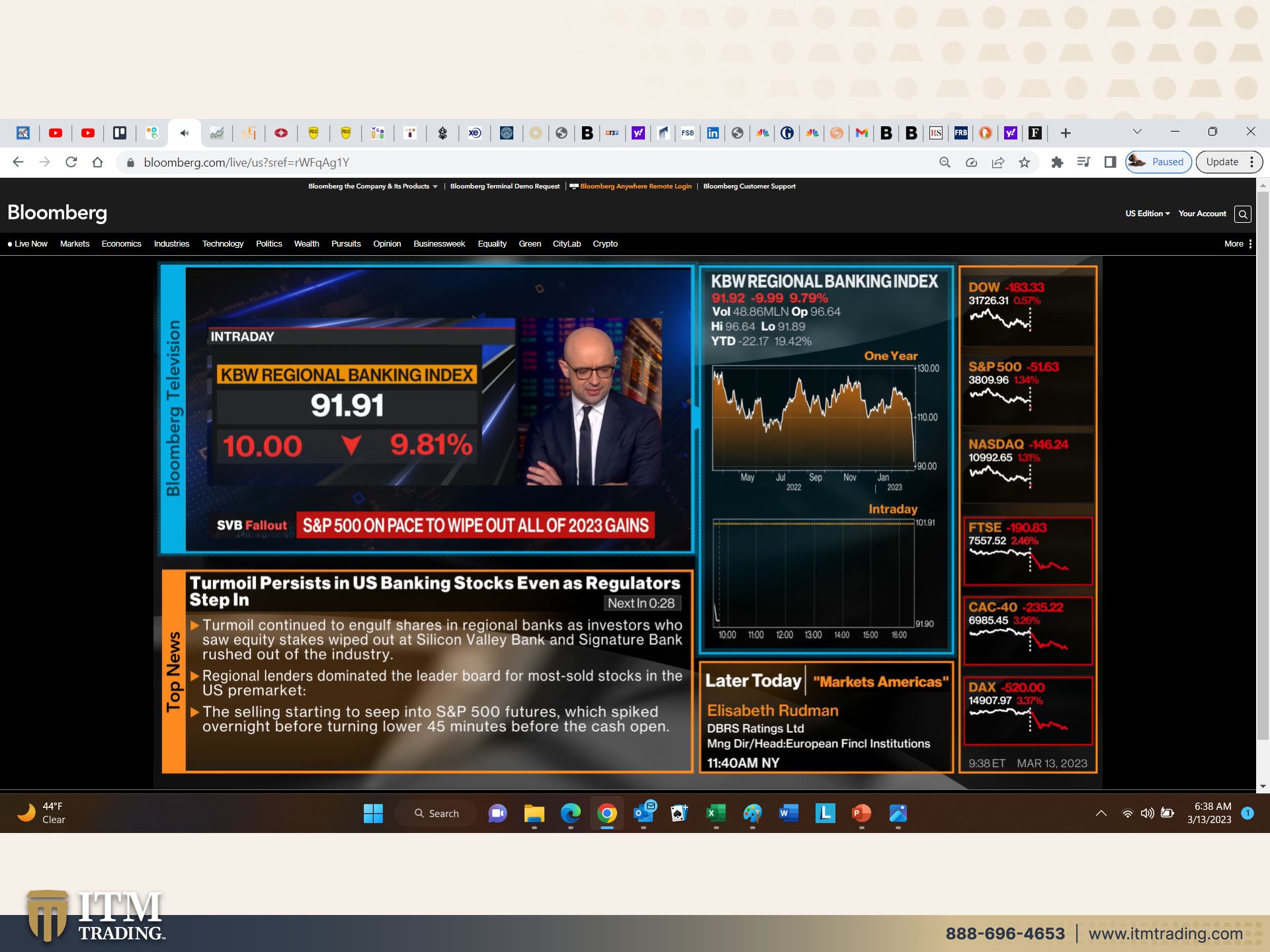

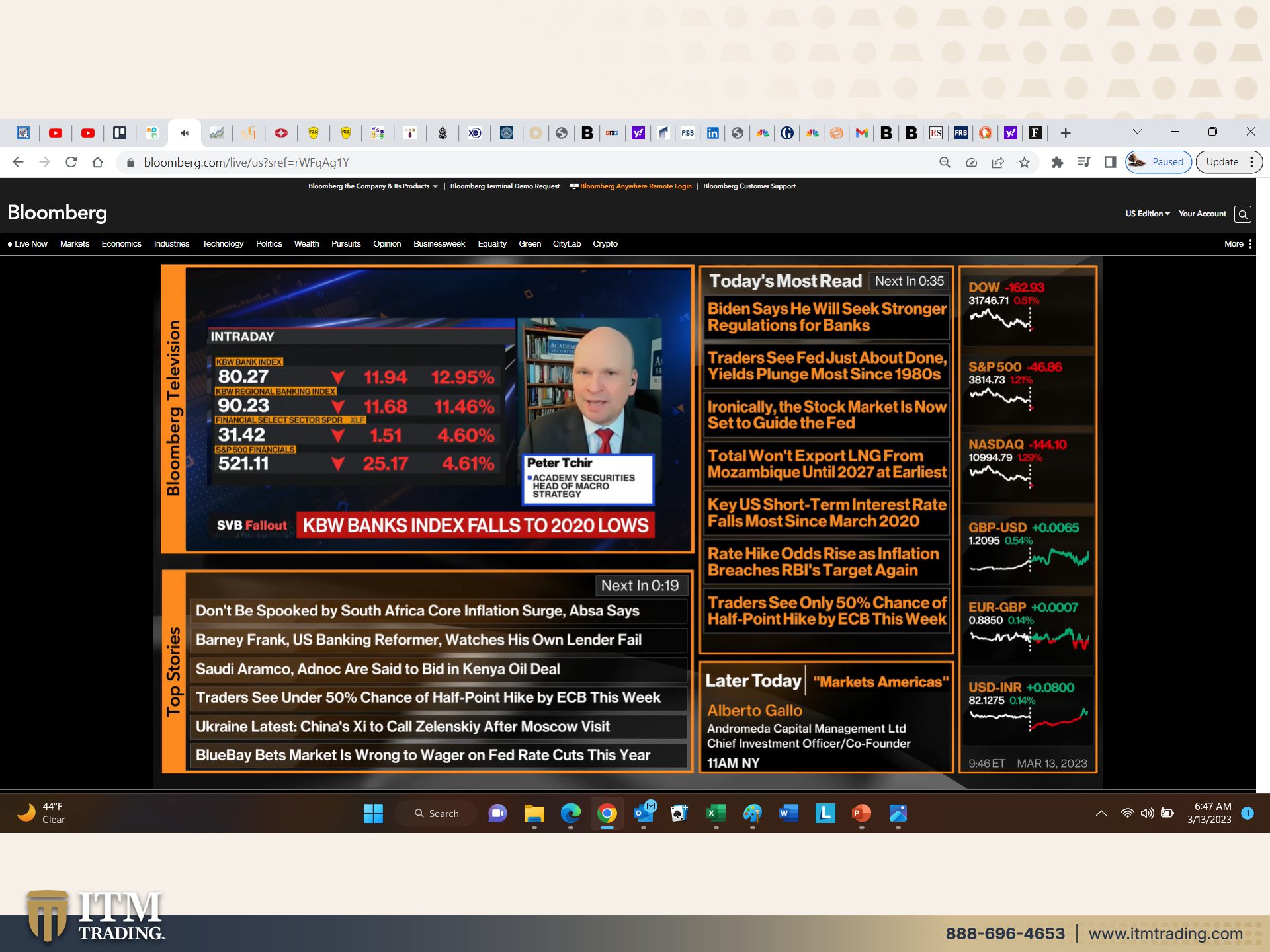

And what is this? Oh, this is is the regional bank index. Banks fall to lowest since November, 2020. What was happening in 2020? Oh yeah, there was another crisis that emerged, didn’t it? SVB collapse hits EU bank shares while analysts see limited risk. While I’m glad that those analysts see that limited risk, and when I look at many of them, they’ve never actually lived through a crisis. And how many have come on board after 2008? I was there on black Monday in 1987, I was there. I know what it looks like and tastes like and smells like. And I gotta tell ya, I I’m getting some deja vu. And that’s what makes me think this is really, really, this could be the Lehman moment. This could very well be turmoil persists in US banking stocks, even as regulators step in. So that’s that confidence piece and how critical it is. Oh, you know, look, if you really think that the Fed has your back, that they’re gonna make you whole, how are they ultimately gonna make you whole? This is how they’re gonna do it. They don’t have any tools, they don’t have interest rates. All they have is money printing. That’s all they have.

You ready for the hyperinflation? Because right now in this flight to safety, right, they’re buying the bonds that’s pushing the interest rates down. But that is temporary. This is temporary. And what’s happening to the value of the dollar in the meantime? And I’m talking about the purchasing power value, which is the one that matters to you and me. You think you think prices at the grocery store are gonna start coming down? I don’t think so. All they’ve been trying to do is slow them, not get rid of them. So this is a very big deal that the turmoil persists in US banking stocks, even as regulators step in. Because what that’s really showing you is that loss of confidence. Now the public confidence is being tested. That’s the piece that we have to see. And by the way, this is that KBW regional banking sector index. Look at that plummet. I’m sorry to have time to do all my fancy stuff on these. This was coming at me this morning hot and heavy. Here we go. We’re showing the lows, but we’re also, that’s the index. And I can’t even see that I should wear my new glasses because then I could see much better. Sorry, but this is, oh wait, that was the one that I liked. Okay, so don’t be spooked. Yeah, I some of these headlines, I mean nothing to see here, folks. Everything is just fine and dandy. Don’t be spooked by South Africa’s core inflation surge. Yeah, don’t worry about it. Yeah, prices are going up. They have it. They could be a failed state, but I just had to read that because don’t be spooked. And what, what did the, the head of SVB Bank come out and say, just the day before it was taken over by the FDIC? Yeah, well just stay calm. Everything is fine, even though he sold a whole bunch of stocks just a couple of weeks ago. But don’t worry about a thing. Oh yeah.

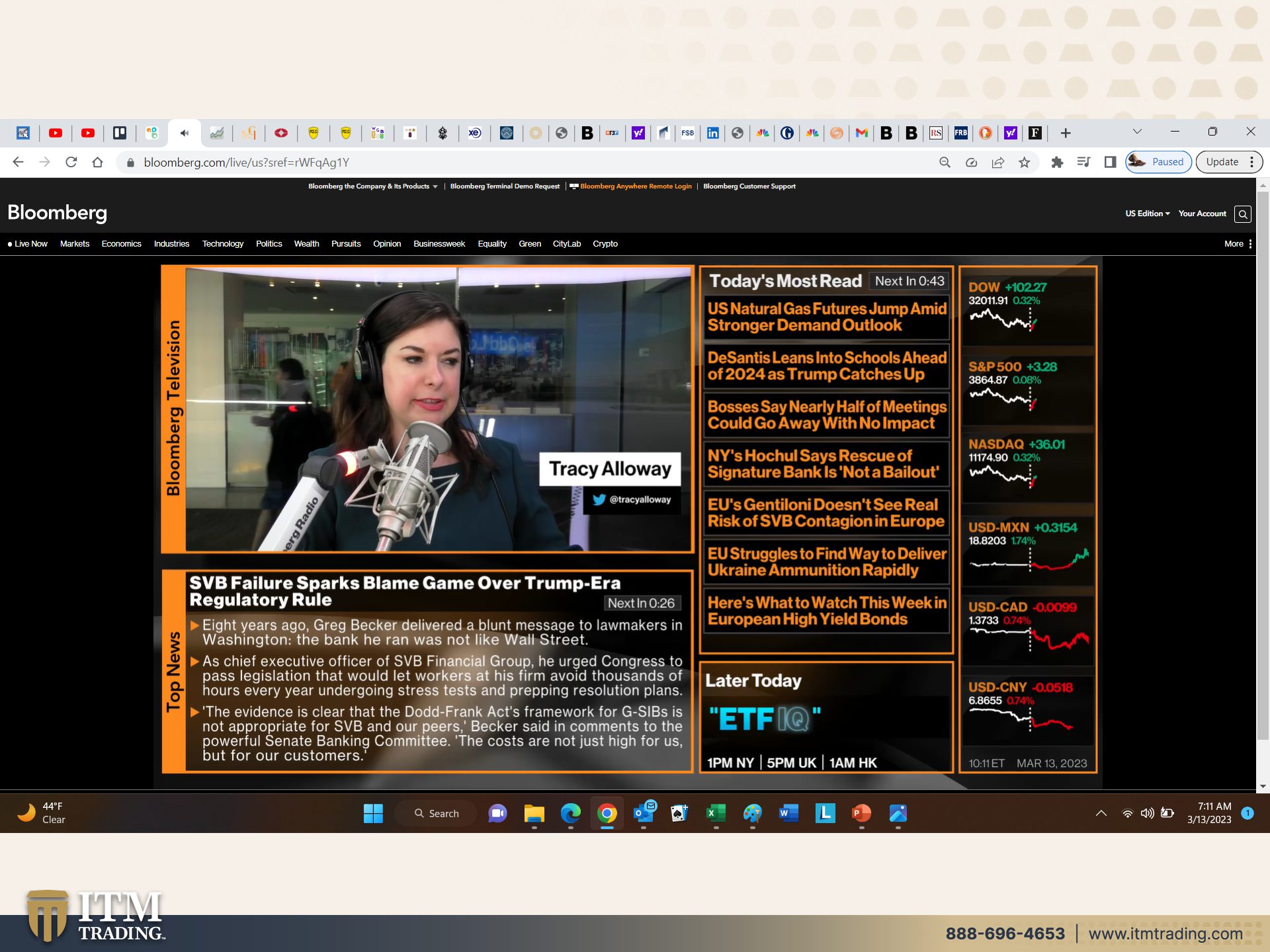

And this is the one Barney Frank, US banking reformer watches own lender fail. It was a seemingly unthinkable scene. Barney Frank, co-author of the Dodd-Frank Act, the radical overhaul of the banking system after the 2008 global financial crisis was having his very own dick fold moment. So Dick Fold was the head of Lehman. There was none of the fold style shouting and ranting. But Frank, just like the foreman, Lehman Brothers top executive had famously done, was talking to the phones to lament how authorities had unnecessarily shuttered the bank. He helped oversee. Now look, Dodd-Frank was put in place and rushed through the, the legalization was rushed through before all of the laws, let alone most of the laws in the Dodd-Frank bail had ever been written. And as soon as they wrote them now, they did not remove the bail in mind you. But, and over the years, if you guys have been following me, you know this, they have systematically taken out all of those investor protections. And not only that, but all of the debt instruments that are at the out there, we just talked about it, what last week? Covenant light. Maybe it was the week before where investor protections have been removed from the system. But don’t worry, stay calm. It’s okay. You know, and it happened to Barney Frank, which is really interesting, and I know I’m probably going overtime, but should we start and stop again? Or how, how do we just keep going? Okay. I’m, I’m sorry you guys, but there’s just so much to talk about. SVB failure, sparks blame game over Trump era regulatory rules where eight years ago, Greg, Greg Becker delivered a blunt message. So that’s the head of SVB Bank, a blunt message to lawmakers in Washington. The bank he ran was not like Wall Street <laugh>. Yeah, no, no. Like Wall Street. Okay, we’ll take your word for it. As Chief Executive Officer of SVB Financial Group, he urged congress to pass legislation that would let workers at his firm avoid thousands of hours every year undergoing stress tests and prepping resolution plans. Frankly, I don’t think it really matters. There is so much leverage and garbage in this system that failure is inevitable. And we’re at the end. The evidence is clear that the Dodd-Frank Acts framework for GSIB so those are systemically important banks. G is for global is not appropriate for SVB and our peers, Becker said in comments to the powerful Senate Banking Committee, the costs are not just high for us but for our customers. It’s about the children, which is how they always position these things, right? But what we’ve witnessed with the dismantling of all the Dodd-Frank Act reforms is that again, those investor protections have been removed and the leverage has been ramped up. So the banks have to hold less and less and less and less and less in reserve. But they trade, they use your deposits, they use that money to trade for securities and derivatives on their behalf, not your behalf. And so did SVB Bank, but so does Chase and Wells Fargo and Bank of America, yeah. Safe? I don’t think so.

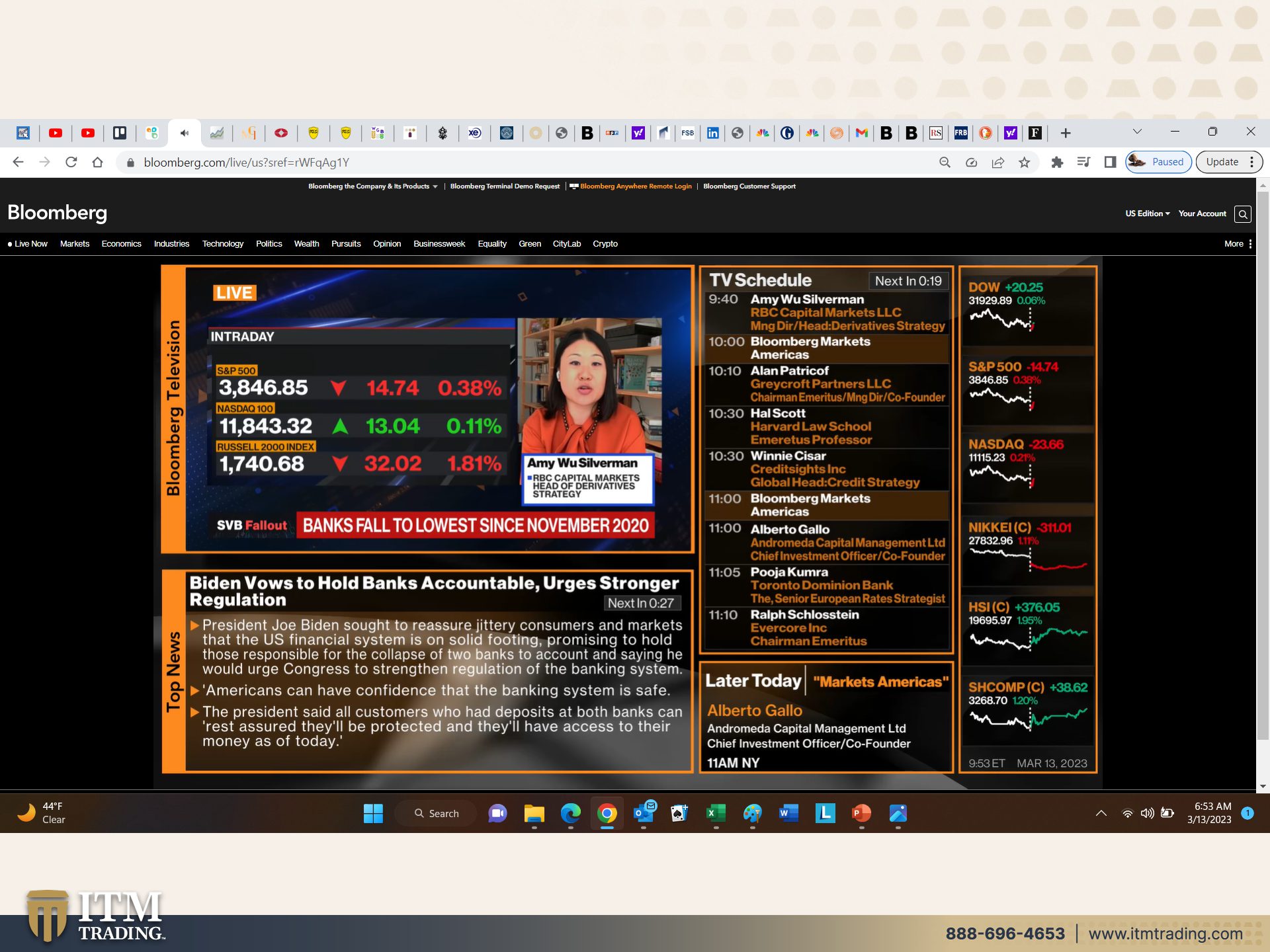

Biden vows to hold banks accountable and urges stronger regulation. Oh my God. Of course, all of this happens after the crisis has happened. And is it gonna, is it gonna really matter? No, but what he’s trying to do is reassure jittery consumers and markets that the US financial system is on solid footing promising to hold those responsible for the collapse of two banks to account and saying he would urge Congress to strengthen regulation of the banking system. Americans can have confidence that the banking system is safe. I don’t have confidence that the banking system is safe and not just because of what happened at SVB, but because of what I’ve been watching over the years. So you have to ask yourself, do you think they’re safe? And oh, by the way, with global central banks buying more gold than they did since 1967, do they think it’s safe? And oh, by the way, don’t you remember that little audio clip from the November 2nd, 2022 meeting of the FDIC resolution committee? And they’re like laughing because the public certainly thinks banks are a whole lot safer than those guys in that room. But you don’t need to know about it because you would make different choices that could cause a run on the bank. No. Leave your wealth in there. Let them take it. But wait, since that happened, we’re gonna step in and we’re gonna backstop everything. Well, who, who is the ultimate payer? It’s the taxpayer. So this not a bailout? Yeah. Arose by any other name.

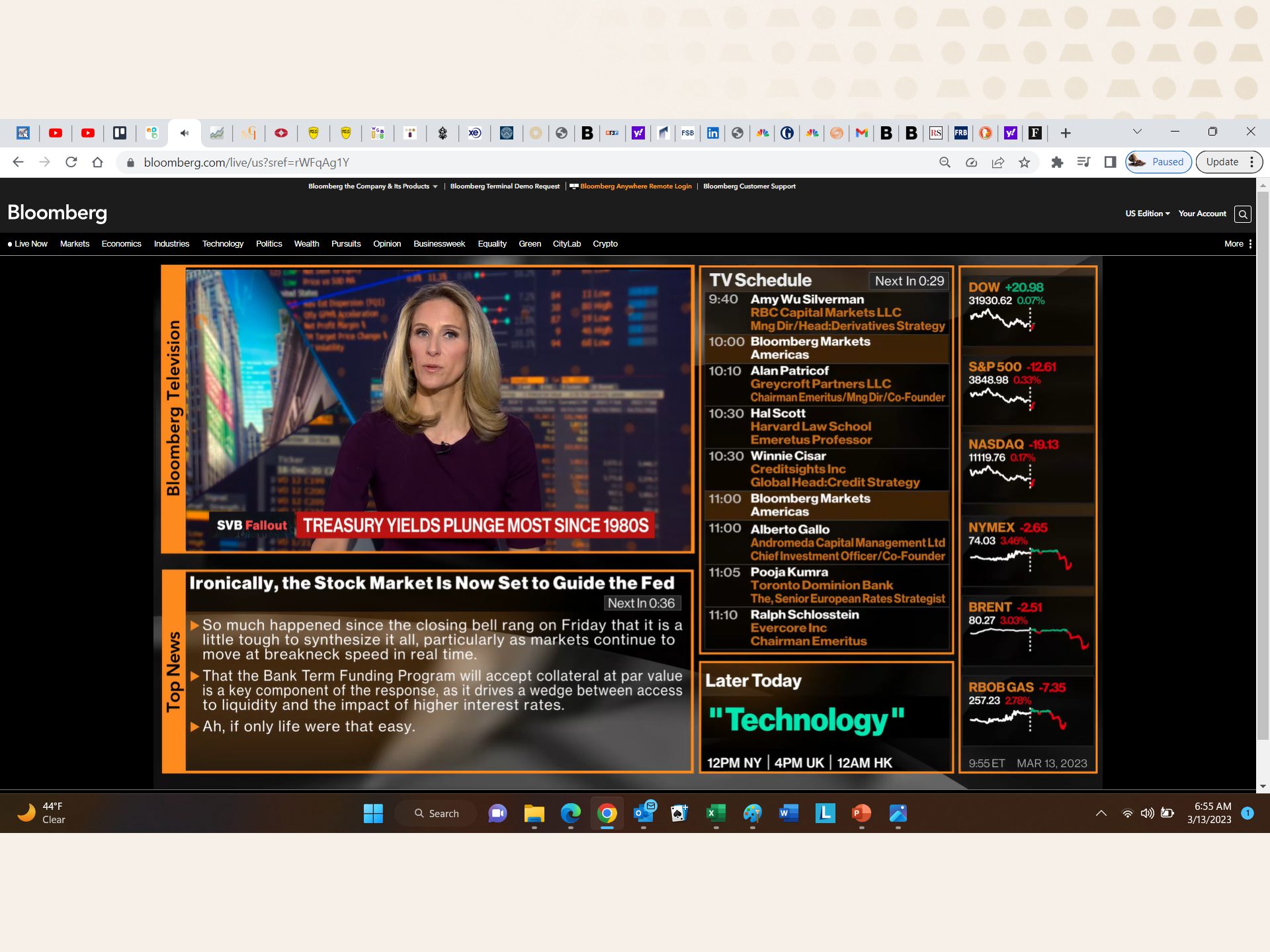

Ironically, ironically, the stock market is now set to guide the Fed. So the Fed was telling the stock market we’re gonna keep raising rates, we’ll do it even more. We’ll go above 6%. Are they gonna? So the really like that because now they have the fed by the cajones again. And the anticipation is, is that interest rates will drop, the fed has done with its tightening cycle, maybe? Turmoil slang slam. Okay, let’s see. Yeah, turmoil slams, slams, bank stocks, even as they go in,oh, I like this one. SVB bonds, so they’re, excuse me, their debt instruments are rising despite treasuries wipe out warning. So the treasury said, came in and said, yeah, we’re gonna backstop all deposits, but we are not going to back stop stockholders or bond holders. They will be wiped out. So why, why would the bonds that plunged in value be rising? Oh, maybe it’s because interest rates have been falling. See, I mean, it’s simple. This is not complicated. And Bitcoin climbs to almost one month high because now the markets have the Fed by the cajones. That’s not an escape, that’s not gonna protect you. This is what’s gonna protect you. This is the first test of this since 2009, really? And it, it is a domino effect. Signature bank closure deals. Another blow to the crypto industry. Lender had relations with the likes of Circle and Coinbase and closure comes days after the collapse of SVB Silvergate. So we had the crypto market, the, the tokens decline, right? That triggered a fallout with FTX. FTX is creating a fallout for SVB and Signature Bank and on and on and on. The dominoes be fallen people, the dominoes be fallen. If Cigna goes outta commission, users may have trouble getting rapidly in and out of exchanges, dramatically impacting crypto market liquidity. Coinbase integrated cignet to allow clients to instantaneously transfer funds last October back in 2021, stablecoin true USD integrated into Cignet for instant settlements. So, you know, Wall Street adopted all of this.

And when Wall Street gets into it, you really think it’s as private as you wanna think it is because it’s not. It is not gold. It may be pictured in terms of gold, but it is not gold. This has broad-based demanded every single sector of the global economy. That’s why it holds its value regardless of what they do in the spot market, which is just a paper contract. But the Feds shut them down citing systemic risk after receiving a recommendation. Regulators promise both SVB and signature depositories and oh, by depositors, oh by the way, everybody else would have full access to their money come Monday. You don’t have to worry about a thing. The Fed is gonna backstop everything except that we are the ones that backstop their balance sheet, by the way. And also by the way, they were supposed to be selling off mortgage backed securities and treasuries.

Hmm, guess they’re not gonna do that into this. They say that no losses will be born by the taxpayer. And I’m sorry that this is kind of disjointed because I was just grabbing stuff as it was coming up, but uninsured deposits, I said, okay, that’s interesting. Will be covered by the DIF fund, which I already showed you, has virtually no money in there. But don’t worry about it, it’s okay as long as they can contain these bank failures. And that’s what they’re rushing to do right now because it becomes very obvious once more, more and more banks fail. Signature was almost exclusively a cryptocurrency firm. So I’m sorry you guys. I said I needed to see who was going to survive before I would go in that direction. And personally, I’m glad that’s the choice I made. I don’t care about the gains, I do care about the losses.

Bitcoin rally cools after jumping the most in almost a month, right? Why? Because they’re more correlated with stocks and the markets now see that they have, they have the Fed by the cajones in terms of raising rates. But is it really gonna matter whether the Fed raises rates, lowers rates, whatever it is that they do? There’s virtually no purchasing power left in the currency. It is hanging on by a thread of confidence this is going to shake. It is, it’s shaken that public confidence of the Fed 2008, it was bank to bank confidence in the interbank lending. 2015, it was Central bank to Central Bank with a Swiss price. August 2022, it was the markets to the fed loss of confidence. And is 2023 gonna be the year that it’s the public to the Fed? It very well could be.

And in the meantime, we’re not going to do that again. We are not going to bail them out. Yeah, they are bailing them out and I don’t care what they call it. And that’s, that’s it for the moment. But we’re gonna be talking about this all week long.

So if you have not yet done it, make sure that you subscribe because I’m staying on top of it. And even when I have to come on with no makeup, sorry you guys, you’re gonna get me as I am in those circumstances because you need to know if this is the Lehman, what I would suggest to everybody if you haven’t done it yet, Food, Water, Energy, Security, Barterability, Wealth Preservation, Community and Shelter. If you are shy on food in your cabinets, then you need to stock those cabinets, rice, beans, meat in your freezer, chickens. If you can go get some chickens, I would go get some chickens and throw ’em in your backyard. They’re really easy to take care of and at least you’ll have eggs, you’ll have protein. If you haven’t set your financial base yet and you’ve got, especially if you’ve got money in those markets, get it done. Click that Calendly link below, make an appointment. But I’m telling you, we’re swamped right now. So just get it done. Just get it done, please get it done. Make sure to subscribe, make sure to leave us a comment, give us a thumbs up, share, share, share, share, share, and then tell tomorrow. Please be safe out there. Bye-Bye.

Do we have questions that came in live? I know I don’t usually do that, but I’m gonna do that based on these circumstances. Yeah. Okay. So Lana S asks: if people start pulling their money out of many banks that will cause more bank failures correct? Correct. That’s what going in and saying we’re back stopping everybody a hundred percent. That’s what the Federal Reserve and the government is attempting to do is to calm you down so that you don’t do that. But go ahead and do it. You remember in 2020 we had all those central banks come out and say, you don’t have to worry about it because we’ll just, we’ll just print the money that we need if you wanna take cash out of the bank. So you’ll see that they’ll do that again. But yes, that’s exactly what that means.

And Linda S. Lane s oh, that’s the one. Perfecto G asks: if banks are collapsing, will people still owe debt? Yes, they will. That never goes away. And even when we go into hyperinflation, typically what they do is they index that debt to interest rates so that you end up owing even more. So. Yes, but that’s also the beauty part about gold and that’s part of the strategy is, is particularly if it is fixed rate debt, to repay that debt, there is a window of opportunity. So talk to us about it. We’ll explain it.

And Crypto m asks: if credit unions fail, what happens to people who have loans? You will still have that debt because they will be transferred to another financial institution. You don’t get to not pay them.

Stephanie w asked: with the price of gold and silver raising, when should I buy? Yesterday! <Laugh>? But if you didn’t buy it yesterday, today and tomorrow, and as long as you can get your hands on it, because in this physical world, once it comes off the market, it’s not going back on. And we’ve seen central banks buying more gold than they have since the last time we went through a major shift.

So yeah, now as soon as you can, is that it for the questions? Okay. And I don’t know if I’m gonna be able to take questions all week, but I’ll do my best. And otherwise just send them in to questions@itmtrading.com and we’ll tackle ’em on on Wednesday, which I’m gonna be a little bit late because I have that other interview I’m gonna have to do at 1:30. So maybe we’ll be early. I’ll talk to Eric about making Q&A early, but send them in to questions@itmtrading.com and we’ll try and get all of your questions answered. And until next, next we meet seriously, get as prepared as you possibly can and be safe out there. Bye-Bye.

VIEWER QUESTIONS:

Question 1:

If people start pulling their money out of many banks that will cause more bank failures correct?

Question 2

If banks are collapsing will people still owe debt ?

Question 3:

If credit unions fail what happens to people who have loans?

Question 4:

WITH THE PRICE OF GOLD AND SILVER RAISING, WHEN SHOULD I BUY?

SLIDES FROM VIDEO:

SOURCES:

https://markets.businessinsider.com/commodities/gold-price?op=1

SVB (SVIB) Failure Was Because of Treasury Bets in Pandemic – Bloomberg

https://www.fdic.gov/analysis/quarterly-banking-profile/qbp/2022dec/qbp.pdf#page=1

https://www.fdic.gov/resources/resolutions/bank-failures/failed-bank-list/

SVB Fallout News: Spreading Problems Around the World – Bloomberg

SVB Doubled Its Canada Loan Book in Year Before Collapse – Bloomberg

SVB (SIVB) Bank Failure and Tech Sector in Asia – Bloomberg

SVB Fallout News: Spreading Problems Around the World – Bloomberg

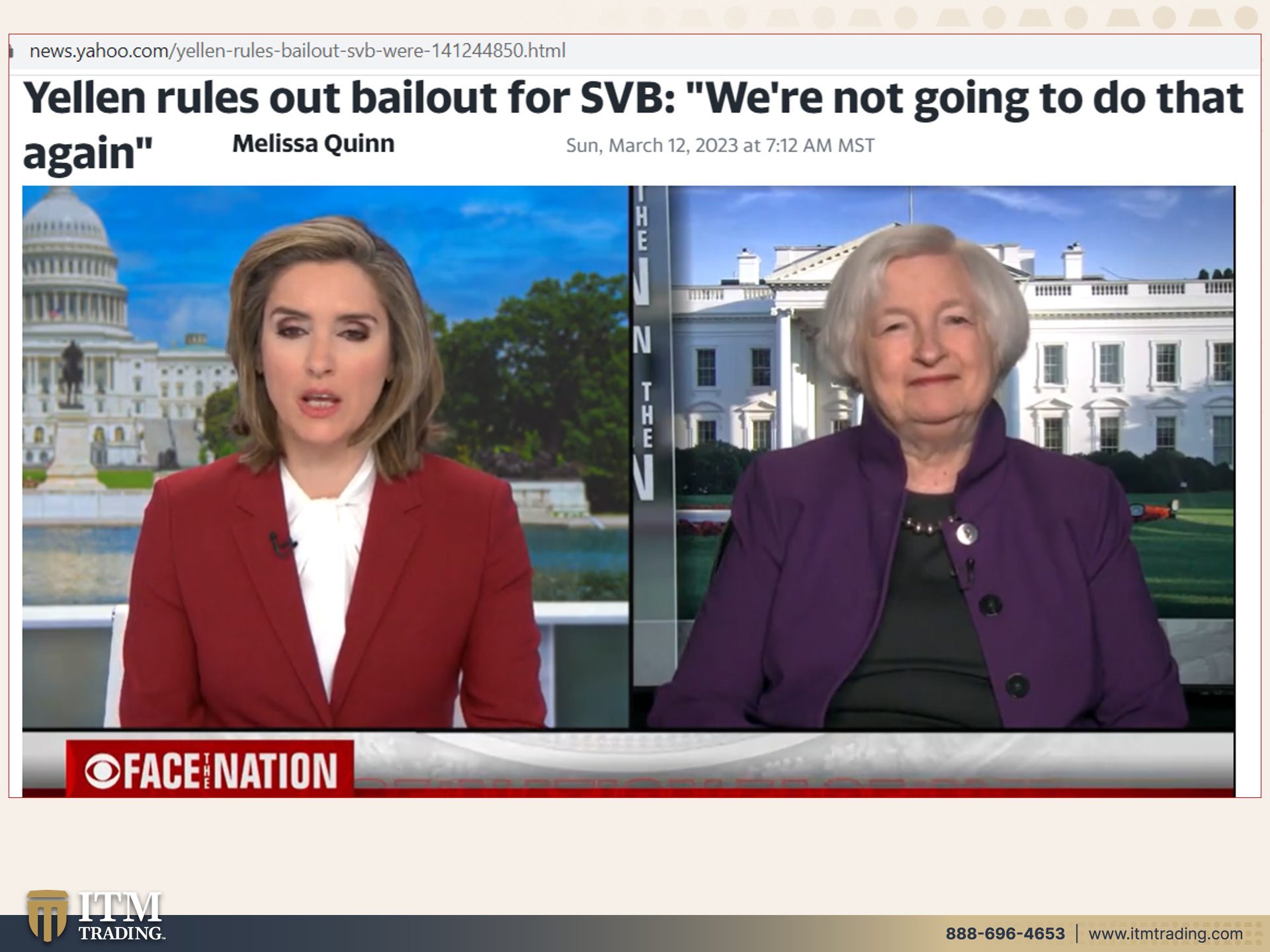

https://news.yahoo.com/yellen-rules-bailout-svb-were-141244850.html