Banks Keep the Profits & Stick Tax Payers with the Losses

Is a new financial crisis looming on the horizon? Janet Yellen’s alarming testimony raises concerns about the safety of community banks and the security of depositors’ funds. As community banks across the country face financial struggles, depositors are left wondering if their funds are at risk. What does this all mean for the safety of your money?

CHAPTERS:

0:00 Janet Yellen on Baking Issues

6:14 Dismantling Dodd-Frank

11:47 Solvency & Liquidity Issue

14:16 Application of EPS to BHCs

15:38 Prepare Your Strategy

TRANSCRIPT FROM VIDEO:

Lynette Zang (00:01):

Whew. In 2017, the then Federal Reserve Chief Janet Yellen, expects no new financial crisis in our lifetime. Wow. Thanks to the, largely to the reforms of the banking system since the 2007 to the 2009 crash. But hey, what’s she saying today? Let’s listen.

Speaker (00:30):

I I don’t have time. I need to be able to drill on a couple things. Let me start with some of the banking issues we’re dealing with on it. Will the deposits and every community bank in Oklahoma, regardless of their size, be fully insured now? Are they fully recovered? Every bank, every community bank in Oklahoma, regardless of the size of the deposit, will they get the same treatment that SVB just got? Or Signature Bank just got?

Janet Yellen (00:57):

Bank only gets that treatment if a majority of the FDIC board, a super majority, a super majority of the Fed board and I, in consultation with the president, determine that the failure to protect uninsured depositors would create systemic risk and significant economic and financial consequences.

Speaker (01:26):

So what is your plan?

Janet Yellen (01:27):

That determination.

Speaker (01:29):

Right? So, so what is your plan to keep large depositors from moving their funds out of community banks into the big banks? We have seen the mergers of banks over the past decade. I’m concerned you’re about to accelerate that by encouraging anyone who has a large deposit in the community bank to say, we’re not gonna make you whole, but if you go to one of our preferred banks, we will make you whole at that point.

Janet Yellen (02:00):

Look, I mean we are, that’s certainly not something that we are encouraging

Speaker (02:05):

That is happening right now.

Janet Yellen (02:09):

That is happening because depositors are concerned about the bank failures that have happened and whether or not other banks could alsoum

Speaker (02:20):

Not it’s happening because you’re fully insured no matter what the amount is. If you’re in a big bank, you’re not fully insured. If you’re in a community bank.

Janet Yellen (02:28):

Well, you’re not fully insured. And

Speaker (02:32):

You, you were at signature and it, it just barely met that threshold you were at signature.

Janet Yellen (02:38):

Well, we felt that there was a serious risk of contagion that could have brought down and triggered runs on many banks. And that something given that our judgment is that the banking system overall is safe and sound. Um depositors should have confidence in the system and we took these actions.

Speaker (03:06):

So there’s a special assessment that’s been done on community banks in my state and all banks across the country. Was there any discussion that that special assessment would only apply to the larger banks or was it always assumed the special assessment would cover every bank, including rural banks In my state?

Janet Yellen (03:23):

I, I think I, I’m not certain what the rules are around that that, that’s up to the FDIC to determine

Speaker (03:31):

It. It has been reported publicly that SVB had a large number of Chinese investors that are there, including some that were companies directly connected to the Chinese Communist Party. It will, will those individual, will those individuals, companies, entities, and investors that are Chinese investors be made whole based on assessments in my banks in Oklahoma. So what I’m asking is, will my banks in Oklahoma pay a special assessment to be able to make Chinese investors whole from Silicon Valley Bank?

Janet Yellen (04:07):

Uninsured investors will be made whole in that bank. And I suppose that could include foreign in foreign depositors, but I don’t believe there’s any legal basis to discriminate among uninsured.

Speaker (04:22):

I get it, but I, I’m just saying my community banks are gonna pay this additional fee. It is always fascinating to me as well the conversation that taxpayers are being made whole. And if the taxpayers are not gonna have any kind of consequence on this, I’m sure my bankers are gonna be very excited to know they no longer pay taxes. And their banks no longer pay taxes. Credit unions don’t pay taxes. Banks do. And so they’re definitely taxpayers as well. And all banks make their revenue off of rates and fees and such to their account holders, which means every Oklahoman will pay higher fees in their community.

Janet Yellen (04:58):

We’re gonna have to, we have lapse of the banking system and it’s economic consequences that will have very severe effects on banks in Oklahoma that will also be threatened.

Speaker (05:11):

I’m, I’m just worried about the long, long, we’re gonna have to move on

Janet Yellen (05:16):

Or we’re not gonna get all senators in.

Lynette Zang (05:19):

We are gonna talk about this today and how this came about. And Janet Yellen flip flopping and having a lot of trouble coming up.

Lynette Zang (05:46):

I’m Lynette Zang, Chief Market Analyst here at ITM Trading of full service physical gold and silver dealer specializing in custom strategies. And if you don’t have one click back Calendly link below and set up a time as soon as you can to develop your strategy and execute it. Because time, the let me tell you, the fuse is lit, but how did we get here?

New Speaker (06:15):

Let’s look at that first because that’s what you’re hearing a lot. And they’ll go back to the changes that were made in 2018. But this was history when investment risk taking banks were merged with deposit taking banks. We had the 1929 collapse. And so then they separated those two industry, those two banking entities and they put in that FDIC insurance. Well, that was really about confidence because this is a con game. While this used to back our currency, the only thing that backs it now is the full faith and credit. But this has been coming about for such a long time because that was the beginning and this is the end. So in 99, well they started setting things up. Clinton signed legislation, overhauling the banking laws because hey, we never learn. And after all this time is different. I can’t even tell you how many times I hear it, but it never is. And so what they then allowed the banks to do, and by the way, this is after they, they changed Reg D and, and put in sweep accounts. So you make a deposit, the bank sweeps it into sub-accounts in their name and then they can use that. And it also reduces the reserve requirement that the banks had to hold for your deposits. But this now in 99 allowed banks, security firms, insurance companies to merge and sell each other’s products. Isn’t that great? Cause we don’t learn anything.

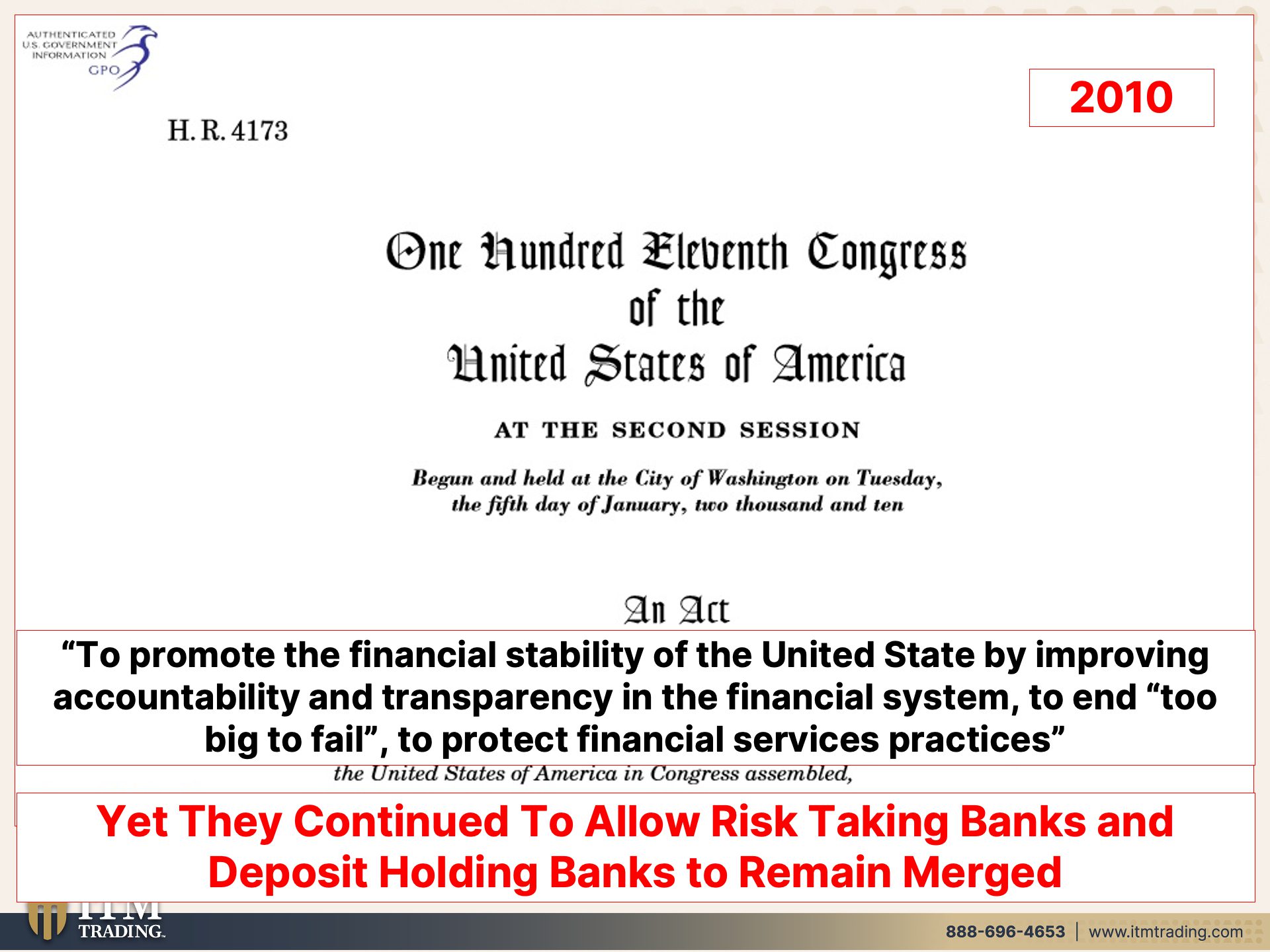

New Speaker (07:56):

But after the crash in 2008, 2000 and that started in 2007, you didn’t see it likely until September of 2008. Then out of that came Dodd-Frank because after all, now we need new regulation. Did they in that regulation separate those two banks? Well, let’s see, because the point of that regulation was to promote the financial stability of the United States by improving accountability and transparency. They love those words. I just wish they would actually like use them, in the financial system and to end too big to fail to protect financial services practices. I think we just saw that boy too big to fail has gotten a whole lot smaller when we just bailed out all insured and uninsured depositors. And there’s so much more to to that. So you definitely don’t wanna miss part three. Part three is, which is you’ve already gotten a chance to see because it was too important to hold back quite honestly. But yet they continue to allow those risk taking banks and those deposit taking banks to remain merged. Do you feel safe? Because six years later, only 70% of Dodd-Frank rules had been written and many more had not even been executed. So it’s a joke of the 390 new rules required by the sweeping law 274 have been finalized and 36 proposed. It was a joke. It was just about making you feel secure. That is so much what central banks and governments, that’s really what they’re about is keeping your confidence, because this is a con game. Is it not visible now?

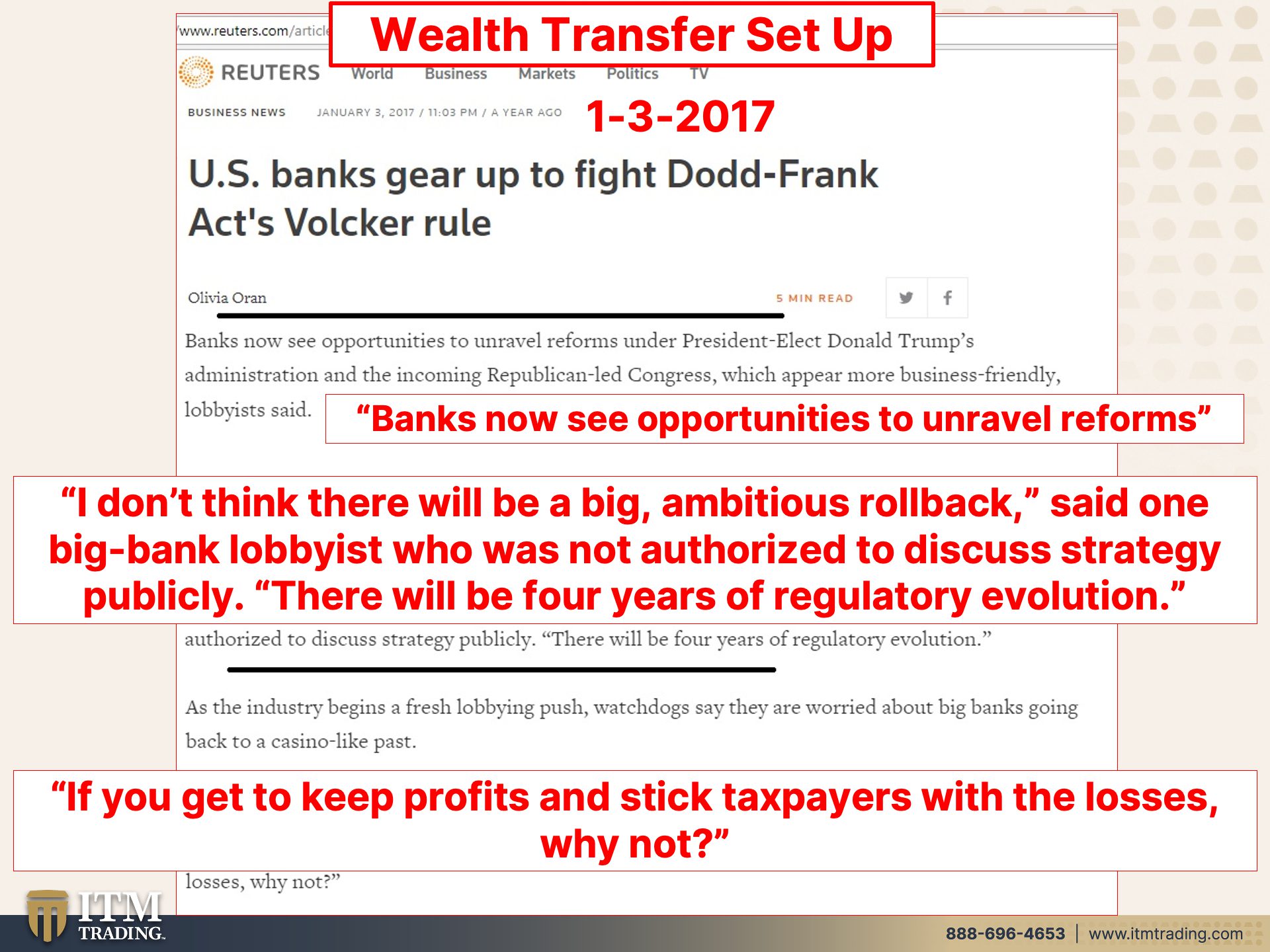

New Speaker (09:56):

But the setup was there. US banks gear up to fight Dodd Frank Act’s Volcker rule. Oh, okay. So they now see opportunities to unravel reform. While I don’t think there will be a big ambitious rollback said one big bank lobbyist who is not authorized to discuss strategy publicly, there will be four years of regulatory evolution. Because if you do it too quickly, the public notices, do you want the public to understand what’s going on? No, you do not. Because once they do, they make completely different choices. If they understand what’s truly at stake and what this government, what these central banks are actually doing to you. The Central bank’s job is not to protect you or me, it’s to protect the banking system. And the banking system is what they use to distribute their policy. So really, if you get to keep profits and stick taxpayer with the losses why not? So even though they’re telling us that this wasn’t a bailout, and again, we’re gonna talk so much more about this in part three. So if you haven’t seen it yet, go back and look. And I would probably listen to that one <laugh> more than once. But because the reality is, is that there was not enough money in the DIF to pay for what they just bailed out in SVB and Silvergate. So taxpayers, you’re gonna pay as you heard.

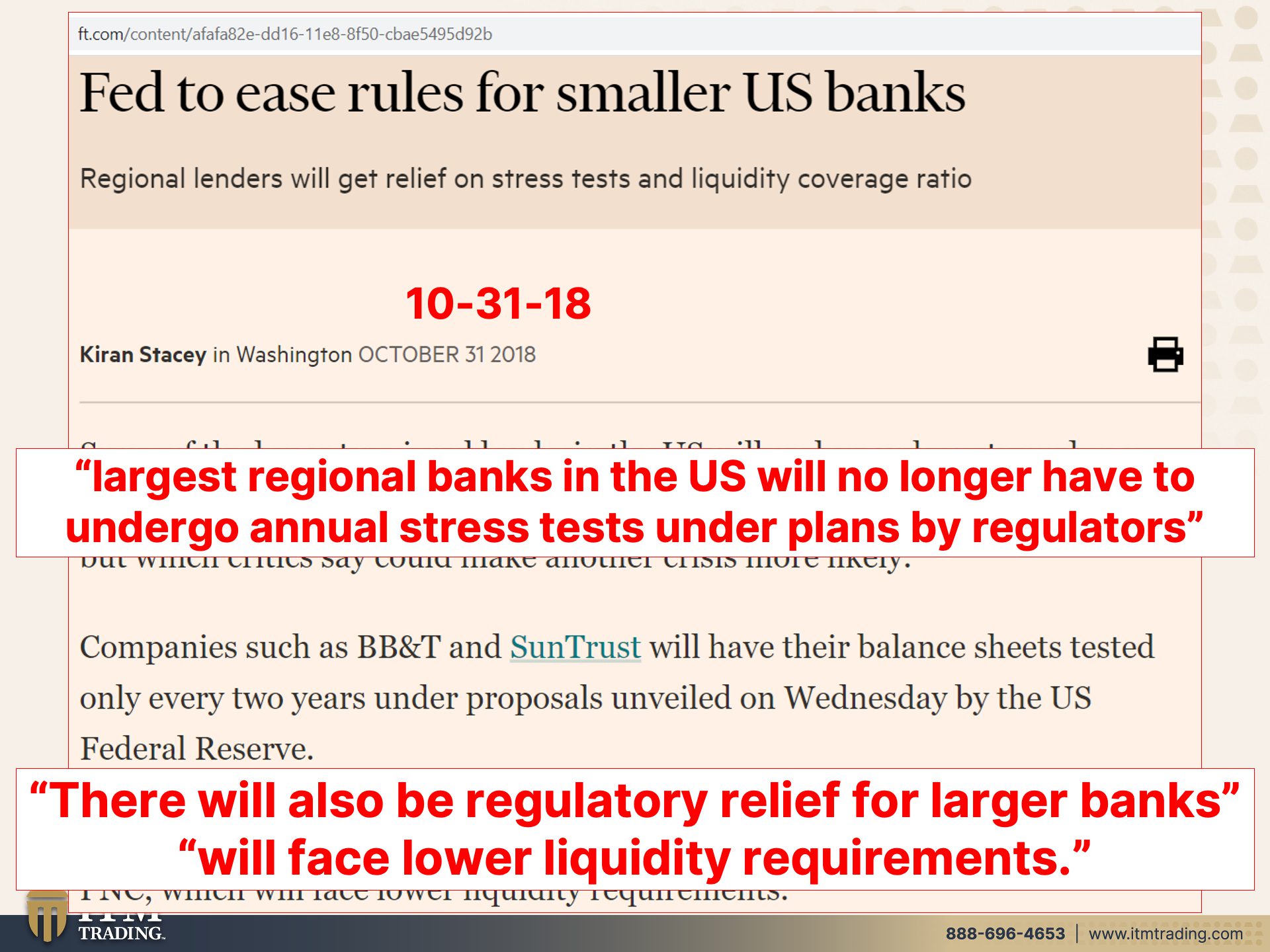

New Speaker (11:40):

So they dismantle the Dodd-Frank rules for banks, whoopty do, and the reforms are rolled back and that’s what really set up this crisis. That’s why you’re hearing all of that. But again, they did not separate risk taking from deposit taking. Do you feel safe? They’re talking about ensuring it. Maybe to a hundred percent raising that FDIC insurance. We’re talking more about that in part three two. Does that make you feel safe? Well, it’s insured. Yeah, only as good as the counterparty. That’s all. It’s as good any contract. Fed to ease rules for smaller banks. Well, we just saw the result of that, didn’t we? Largest regional banks in the US will no longer have to undergo annual stress tests under plans by regulators. And I got news for you, those stress tests were a joke anyway, but good to know that they don’t have to go through those stress tests anymore. There will also be regulatory relief for larger banks and larger banks will face lower liquidity requirements. So what are we hearing on the news? Oh, this is a liquidity issue. It’s not a solvency issue. I got news for you. It’s a solvency and a liquidity issue. And with all of that money that the Fed has pumped into this system over all of these years, why are we having a liquidity issue? And with all of the changes in regulations that enable banks to hold less and less, why are we having a solvency and liquidity issue?

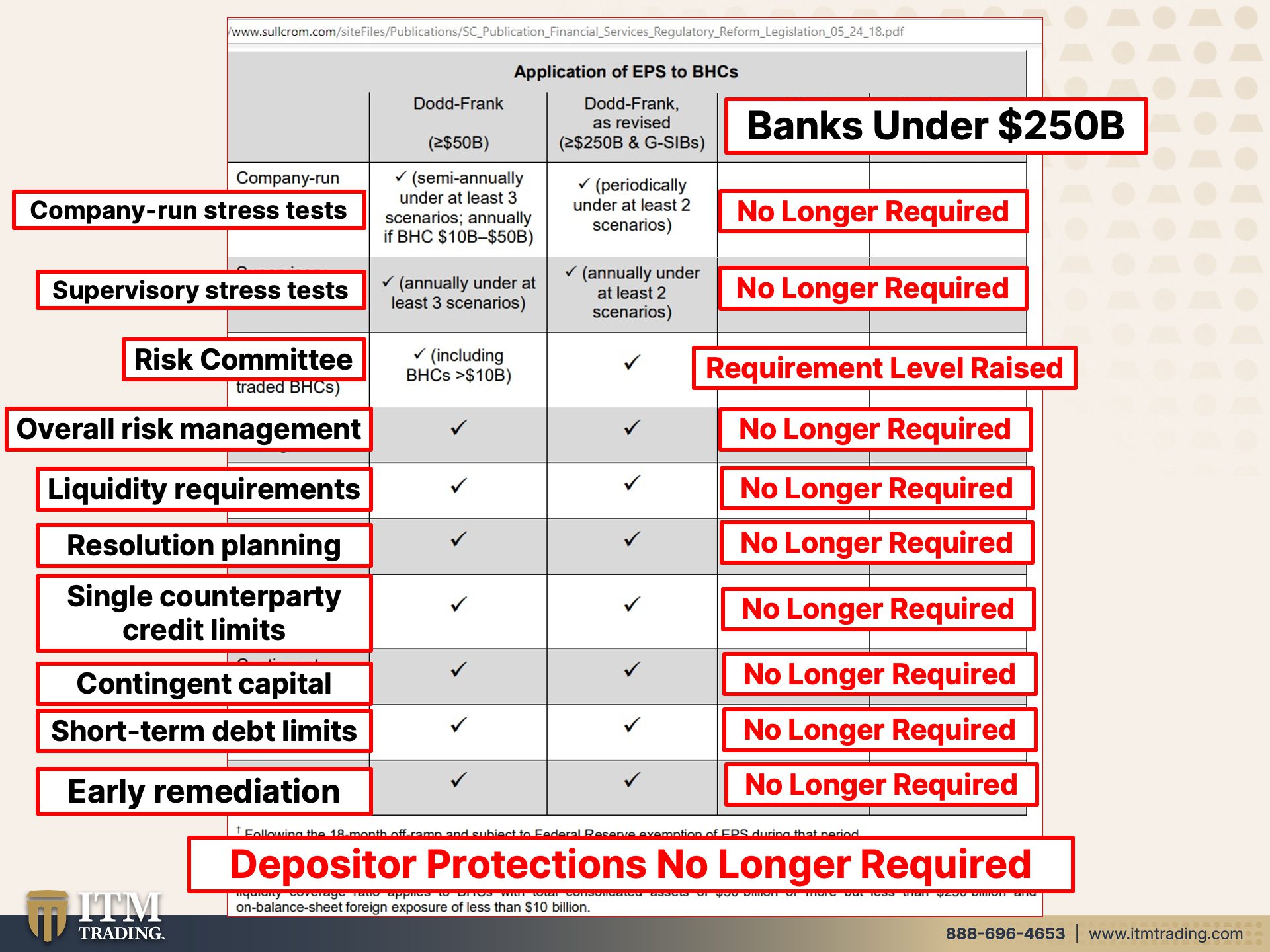

Lynette Zang (13:28):

Well, let’s take a look at the changes for those smaller banks because this is what they were running. You know, stress test, supervisory stress test risk committees, overall risk management, liquidity requirements, resolution planning. That means if they fail, what’s the next step? Single counterparty credit limits. So that means limiting those counterparties contingent capital, where are you gonna get money from if you need it? Short term debt limits and early remediation. So that’s a pretty hefty list. What did they do? And these were for all banks under 250 billion. There you go. No longer required. No longer required. What does that really mean? Deposit or protections no longer required.

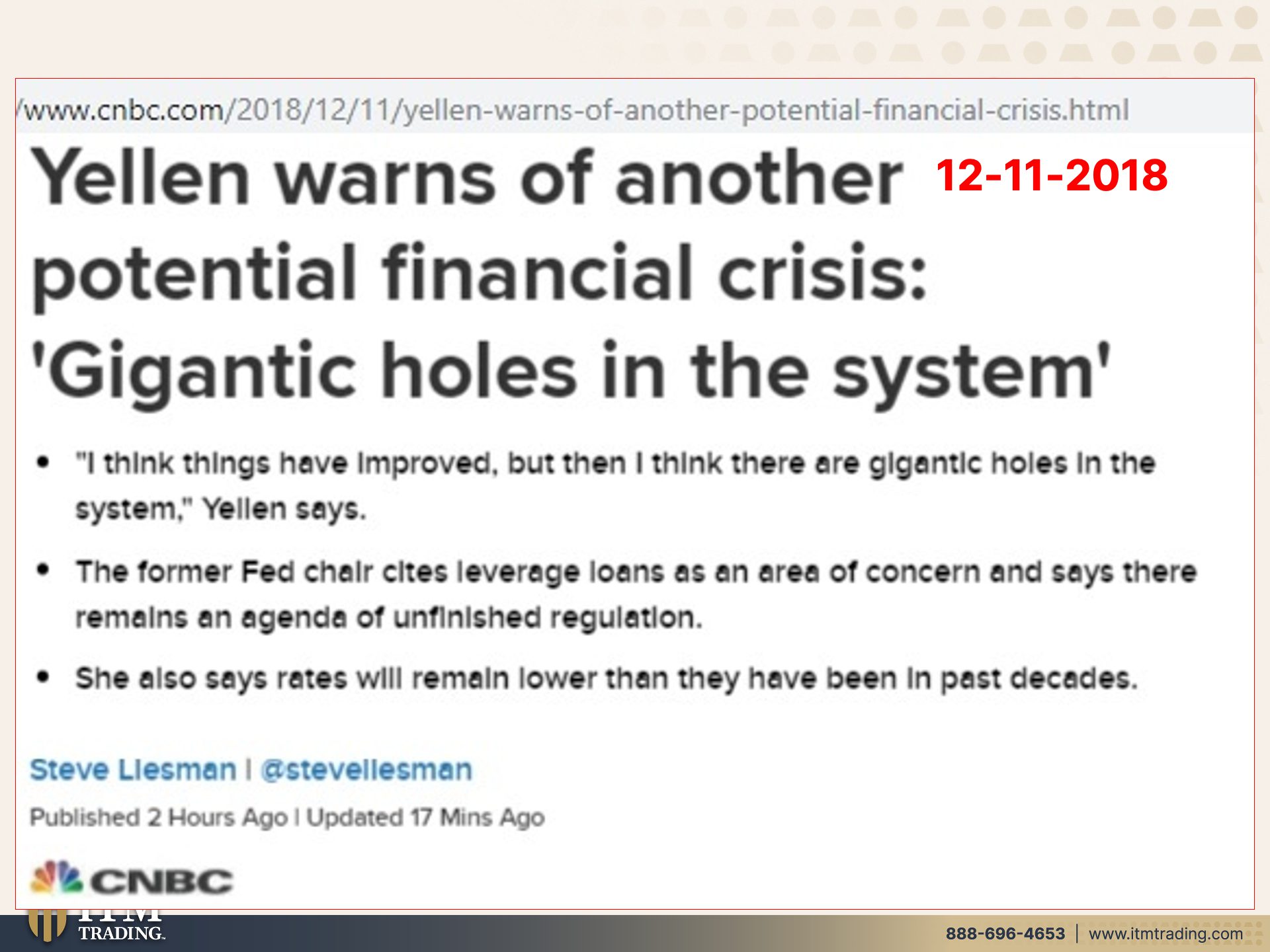

New Speaker (14:16):

Do you feel safe? We’ve talked about this before because all of a sudden where she said, never gonna see another financial crisis in our lifetime. I mean, can you believe the stupidity of her coming out and saying that? The hubris of her coming out and saying that it was mind blowing when she did it. And I’m sure it’s pretty mind blowing now. And I’m also sure that she probably regrets saying that. I mean, if I were in her position, I never would’ve said that. That’s just stupid <laugh>. It’s just stupid at any rate, because by the next year she was warning of another potential financial crisis, gigantic holes in the system. I think things have improved. But then I think there are gigantic holes in the system. Yellen says the former fed chair sites leverage loans as an area of concern and says there remains an agenda of unfinished regulation. Oh, well they’ll talk a lot about the regulation now, won’t they? She also says rates will remain lower than they have ever been in past decades. Yes, indeed. So this is the setup, and I could have gone into it even more, but what you really need to understand is how vulnerable you are. You are just the right size to fail. And quite honestly, the reason why they bailed those two en, there are a number of reasons, but one of the reasons why they bailed those entities out was because it was too big to hide. And if they didn’t bail out uninsured, depositors, it would’ve caused more bank runs. Their job is to keep this system whole. Your job is to make educated choices that put your best interest first. And we vote with our purses and our wallets.

Lynette Zang (16:23):

This my friends, is my vote. It is completely out of the system. It has use across the entire lobe in every single sector. So there is always demand. This is your wealth shield. It’s made of gold, it’s made of silver, physical in your possession. Get it done. Get it done. Now along with Food, Water, Energy, Security, Barterability, Wealth Preservation, Community and Shelter. Stay tuned for part two and make sure you watch part three. And if you haven’t watched this yet, because frankly what happened last September with the Bank of England was when that fuse was really lit. And we talked about that on the Coffee with Lynette, with my good friend Mario, Innecco. So you definitely wanna watch that video as well. Also, on the Spanish speaking channel, make sure that you share this. It’s broken down into even smaller pieces, but it’s critically important that everybody understands. Again, if you haven’t clicked that Calendly link below, set a time to get your strategy in place. Make sure that you subscribe, leave us a comment, give us a thumbs up and share, share, share. And until next we meet. Please be safe out there. Bye-Bye.

SLIDES FROM VIDEO:

SOURCES:

https://www.ft.com/content/afafa82e-dd16-11e8-8f50-cbae5495d92b