NEW RULES CHANGING: Are You Ready for the Bail-in? by Lynette Zang

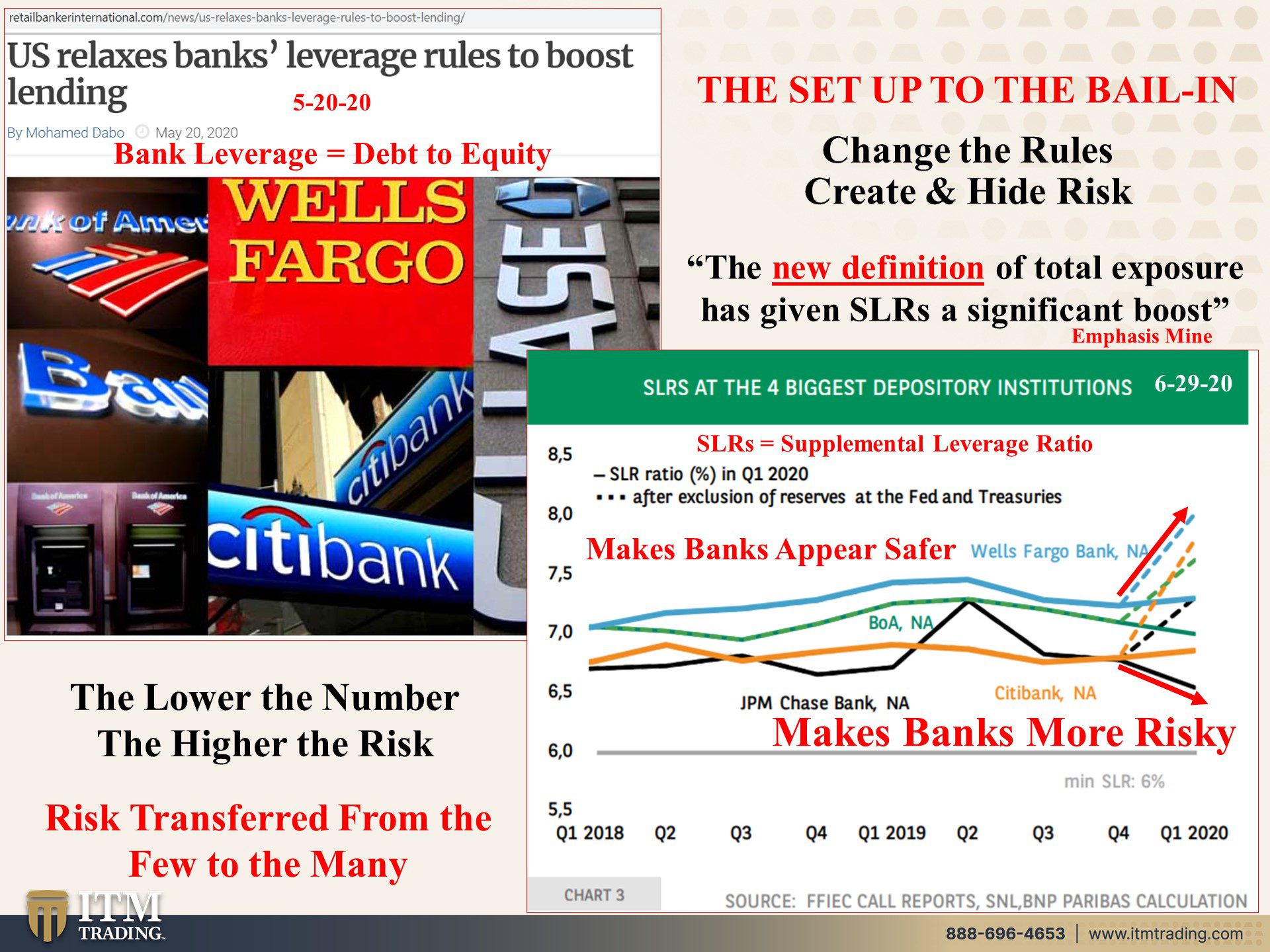

The Dodd-Frank Act was put in place in 2010. This Act was supposed to limit risk in banks, though many of those restrictions have yet to be instituted and many of those that were have been watered down or eliminated over the last ten years. Using the current pandemic crisis as excuse, there are currently a plethora of changes in the works, all of which increase risk in the banking system but make banks “appear†safer. This is a way to transfer the risk from the few (elites) to the many (public).

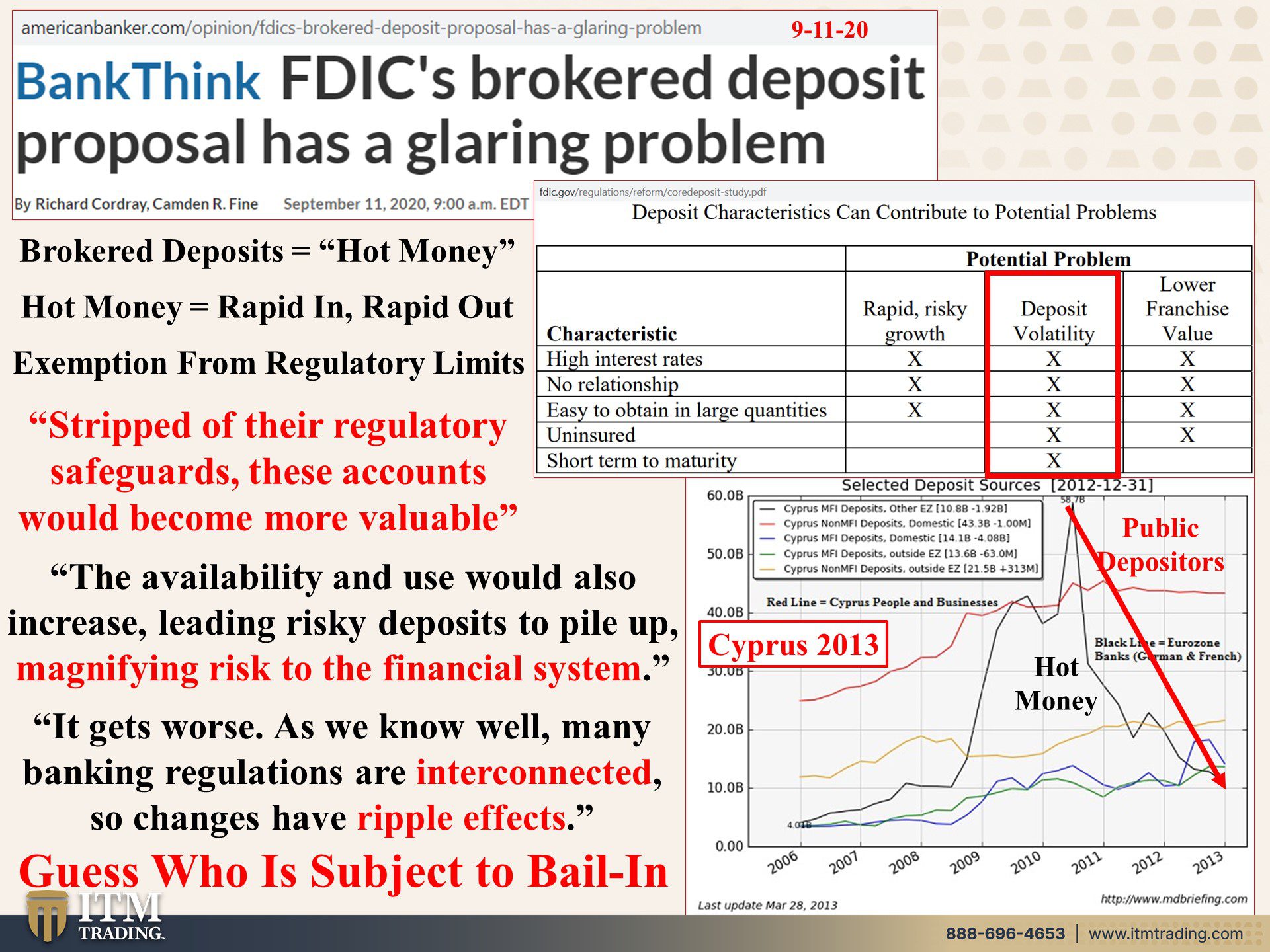

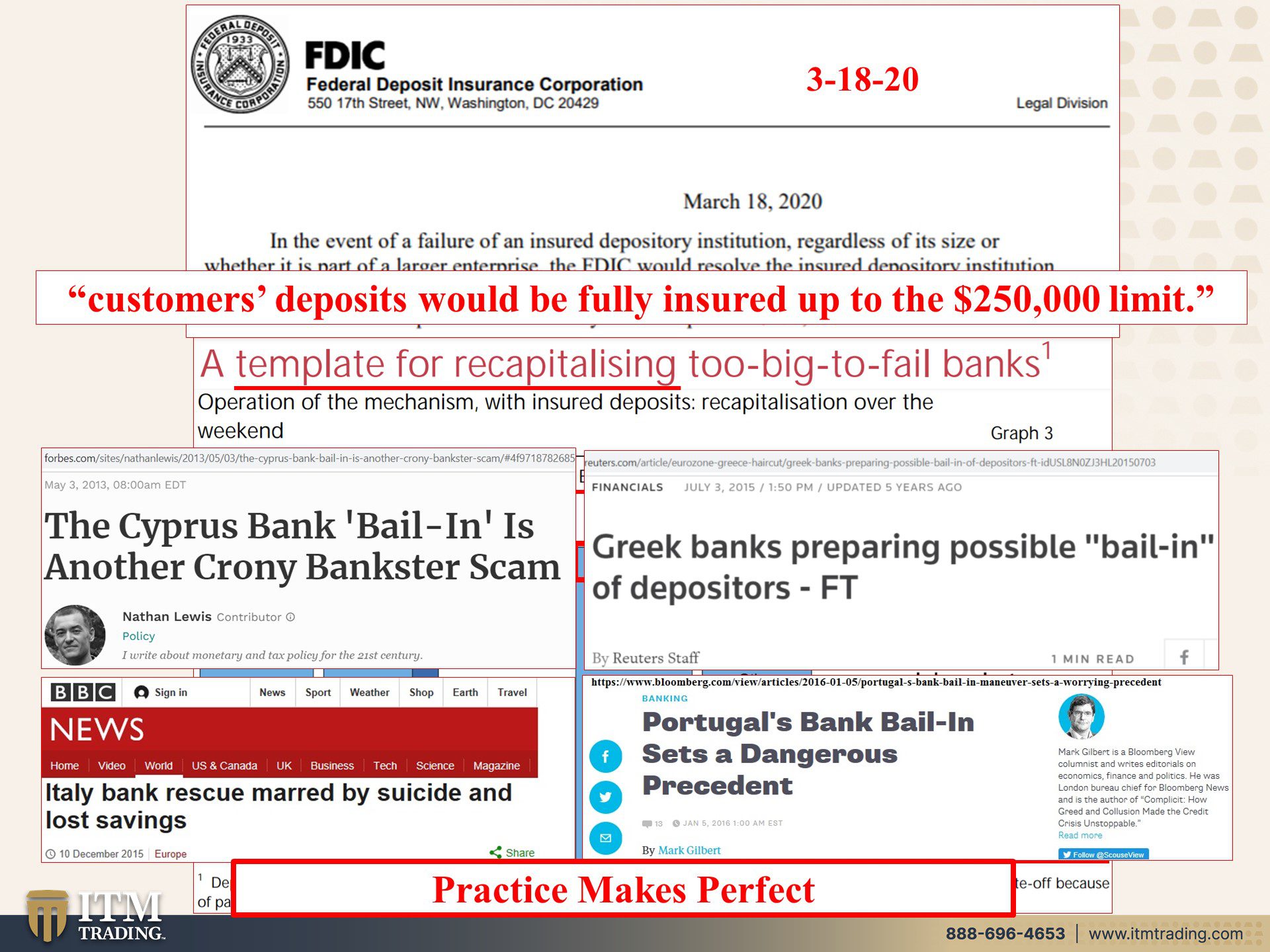

There is, however, one rule written into the Dodd-Frank Act that has not changed, the Bail-In rules. First tested in Cyprus in 2013, then in Greece, Italy, Portugal and more. This is touted as a way to avoid taxpayer funded bailouts. In Europe, they created bail-inable bonds, but depositors are also considered creditors and thus, subject to bail-in.

Cyprus taught bankers that they had to honor deposit insurance schemes (though they can still limit access to bank held funds), so taxpayers might still fund those balances, but we are assuming there is enough set aside in those schemes to make depositors whole when a bank fails.

Put in place to alleviate depositor fears in 1933, the truth was almost visible as the 2008 financial crisis unfolded and bank failures spiked. This pushed the DIF (Deposit Insurance Fund) toward insolvency. In fact, according to the most current DIF report (March 20, 2020), there was a little more that 1 penny to insure each “insured†deposit. If bank failure flow can be controlled, this fact and the risk to all depositors can be hidden.

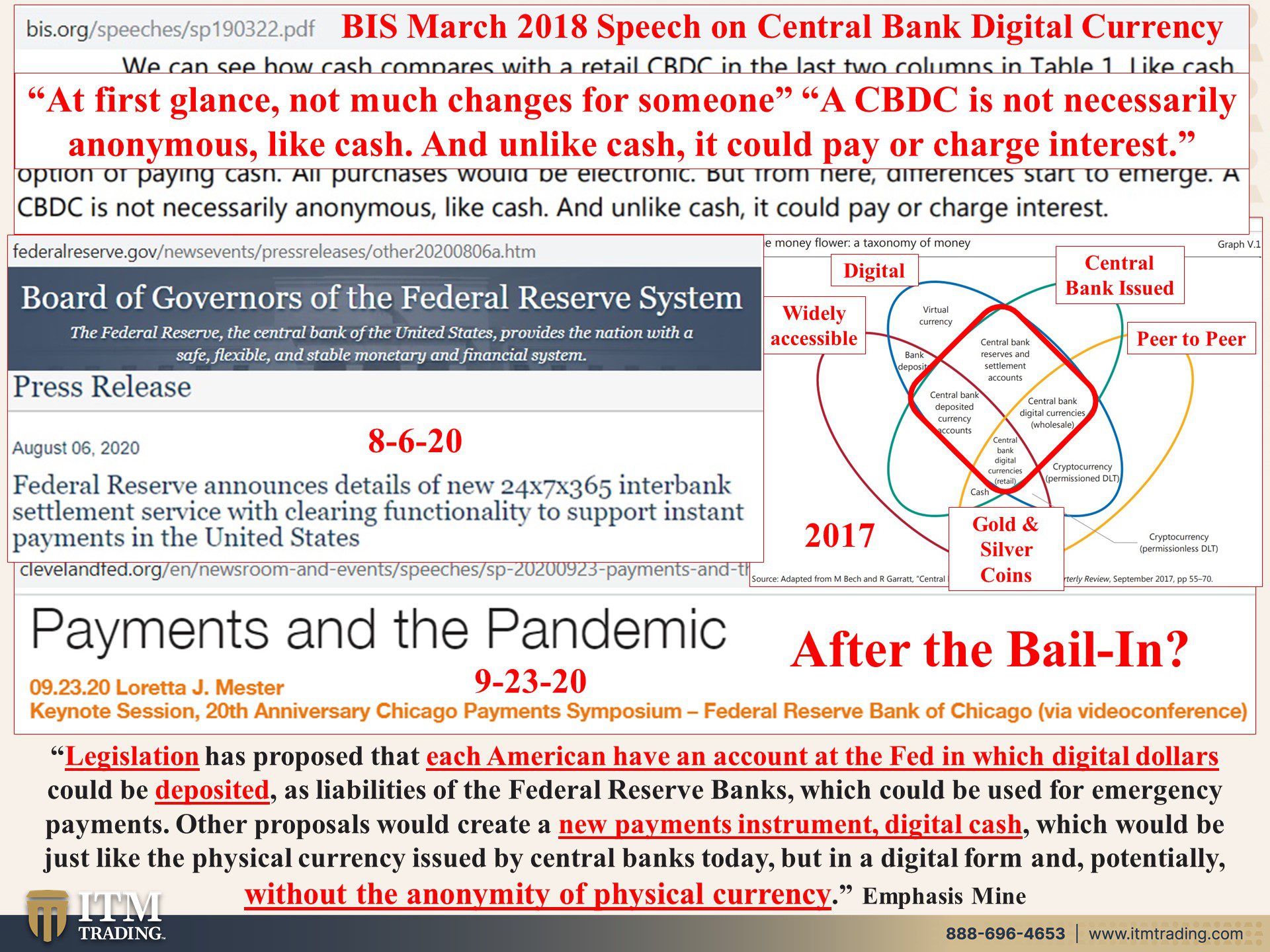

Could this be why there was such a rush to print new cash for banks to distribute last March and April as a bank run began because of Covid-19? Could this also be part of the push into CBDC (Central Bank Digital Currency) and away from “dirty†cash? Once everything is intangible, a bank run becomes much easier to stop, just a keystroke.

Of course, there are many other benefits of CBDC for governments and central banks. For governments, those benefits are around taxation, for central bankers, those benefits are around policy execution control. For you those benefits are about convenience. Who do you think have the biggest benefit?

Listening to central bank rhetoric, it should be clear that the reset has already begun, though when it will become clear to you (with the official overnight currency devaluation) is still in the future. But these things, and more, are what makes holding physical gold and silver so critical. And the sooner the better.

Some people try to time the markets, believing wall street’s spot gold and silver contracts. But this is short sighted. Don’t you remember what happened in March and April? Choices in the kinds of gold and silver became very limited and premiums exploded.

Further, because there is finite amount of physical metals, those taken off the markets then, are most likely to be unavailable during the next rush. I know I’m not selling my gold and silver. So this next rush will likely see premiums at an extreme level and availability even tighter.

This becomes important if you are executing the ITM Strategy because not all gold and silver are created equal. It is really all about your goals and which metals in what form are most likely to support your goals the best.

Just keep in mind, those that understand money own gold, which is why central bankers have been voraciously accumulating gold since 2008. If they are, don’t you think you should too?

Slides and Links:

- https://www.ft.com/content/99988a6a-901a-4992-abaf-1c9478a2fd55

https://www.retailbankerinternational.com/news/us-relaxes-banks-leverage-rules-to-boost-lending/

https://www.davispolk.com/files/09.12.14.Supplementary_Leverage_Ratio.pdf

https://economic-research.bnpparibas.com/Views/DisplayPublication.aspx?type=document&IdPdf=39130

- https://www.americanbanker.com/opinion/fdics-brokered-deposit-proposal-has-a-glaring-problem

https://www.fdic.gov/regulations/reform/coredeposit-study.pdf

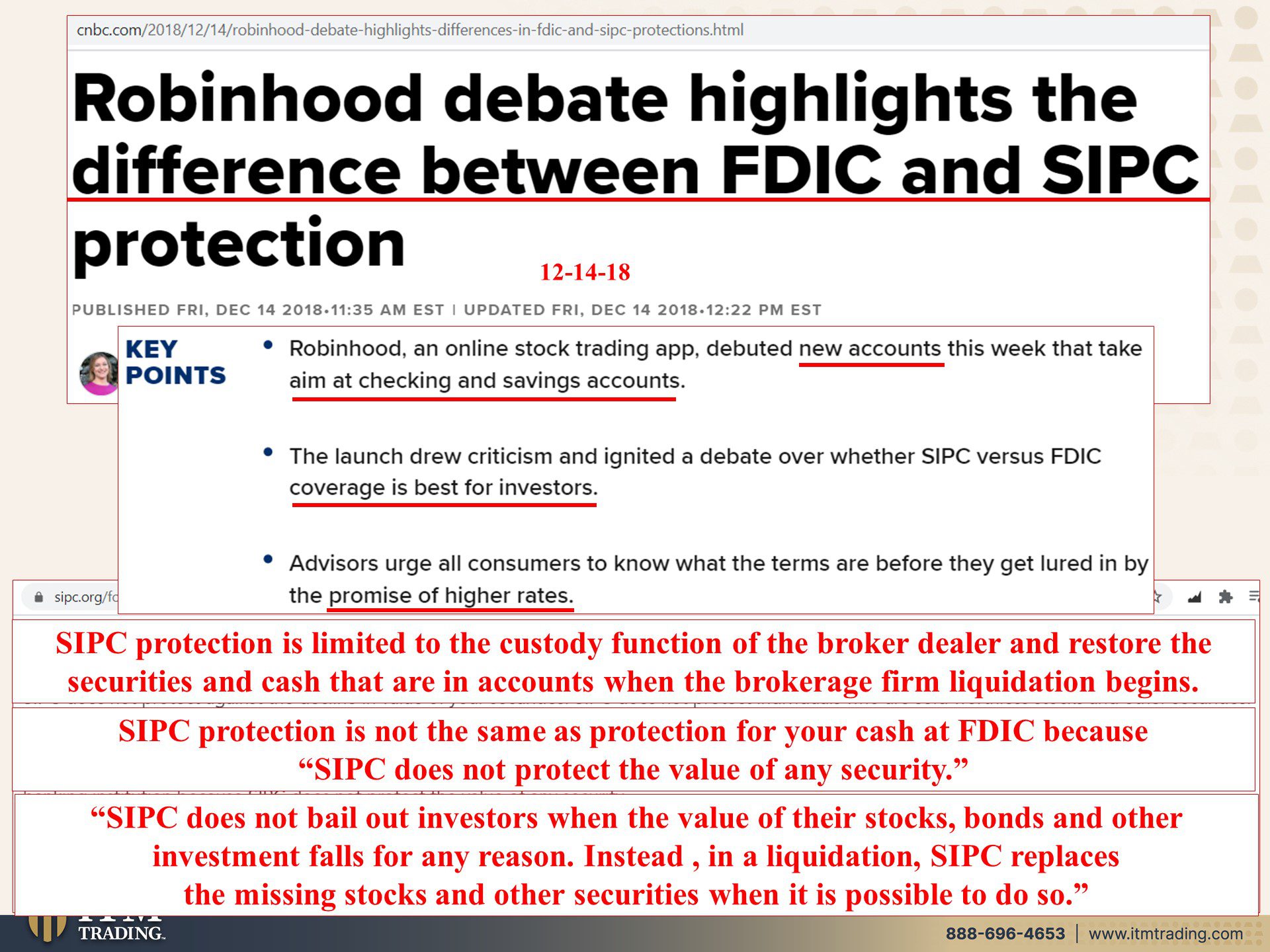

- https://www.sipc.org/for-investors/what-sipc-protects

https://www.cnbc.com/2018/12/14/robinhood-debate-highlights-differences-in-fdic-and-sipc-protections.html

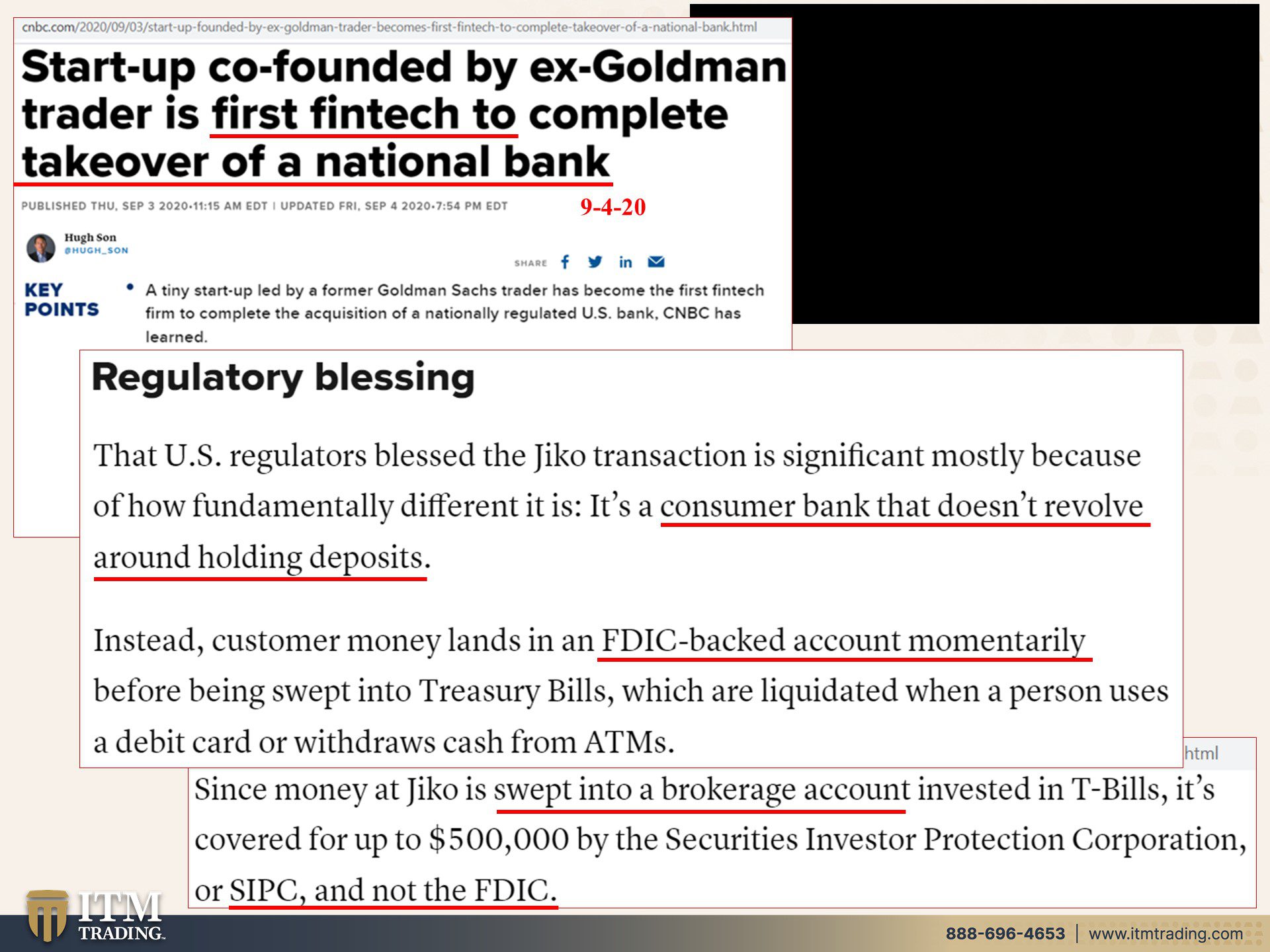

- https://www.cnbc.com/2020/09/03/start-up-founded-by-ex-goldman-trader-becomes-first-fintech-to-complete-takeover-of-a-national-bank.html

https://www.clevelandfed.org/en/newsroom-and-events/speeches/sp-20200923-payments-and-the-pandemic.aspx#U3

- https://www.fdic.gov/regulations/laws/rules/2000-9400.html#fdic2000part380.31

https://www.govinfo.gov/content/pkg/PLAW-111publ203/pdf/PLAW-111publ203.pdf

https://www.bis.org/publ/qtrpdf/r_qt1306.pdf

https://www.forbes.com/sites/nathanlewis/2013/05/03/the-cyprus-bank-bail-in-is-another-crony-bankster-scam/#4f9718782685

https://www.reuters.com/article/eurozone-greece-haircut/greek-banks-preparing-possible-bail-in-of-depositors-ft-idUSL8N0ZJ3HL20150703

https://www.reuters.com/article/italy-banks-bail-in/italy-approves-eu-bank-bail-in-measures-idUKL8N1384JR20151113

- https://www.fdic.gov/bank/analytical/quarterly/2020-vol14-2/fdic-v14n2-1q2020.pdf

https://fred.stlouisfed.org/series/DPSACBW027SBOG

- https://www.clevelandfed.org/en/newsroom-and-events/speeches/sp-20200923-payments-and-the-pandemic.aspx#U3

https://www.bis.org/cpmi/publ/d174.htm

https://www.bis.org/publ/qtrpdf/r_qt1709z.htm

https://seekingalpha.com/news/3610101-16b-ohio-police-fire-pension-fund-buying-gold