Fed Warns of Housing Bubble…by LYNETTE ZANG

Have you seen the headlines? The same central banking oligarchs who consistently dump money into the economy, sending inflation on a rampage has issued a warning, and it’s made headlines everywhere. The Fed just published a very dire warning for the public. The warning that I’m talking about is around the real estate market. They’re saying that there could possibly be a housing bubble!

CHAPTERS:

0:00 Video Overview

0:36 Intro

1:24 Will Raising Rates Destroy Demand?

6:51 Their Ultimate Goal

9:28 Interest Rates Surge Through Economy

18:19 Rent Control Is Back

23:18 Home Defaults Increasing

26:29 Tips from Lynette

30:47 Outro

TRANSCRIPT FROM VIDEO:

Do yourself a favor. You gotta have a plan.

“The Behavior that we’re seeing with this housing market suggests that a bubble might be brewing and that it will eventually pop.”

If you don’t have a plan you’re really planning to fail. This is not going away. It’s going to get worse.

The Fed just published a very dire warning for the public. And that’s what we’re gonna talk about today. Coming up.

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, a full service physical gold silver dealer. And the Fed just issued a warning about real estate. Now, considering that real estate is roughly 30% of the global economy, and they’ve worked real hard, those global central bankers to reflate that bubble after it popped in 2008. Interesting that they would talk now about a housing bubble, but let’s take a look and see what they’re saying.

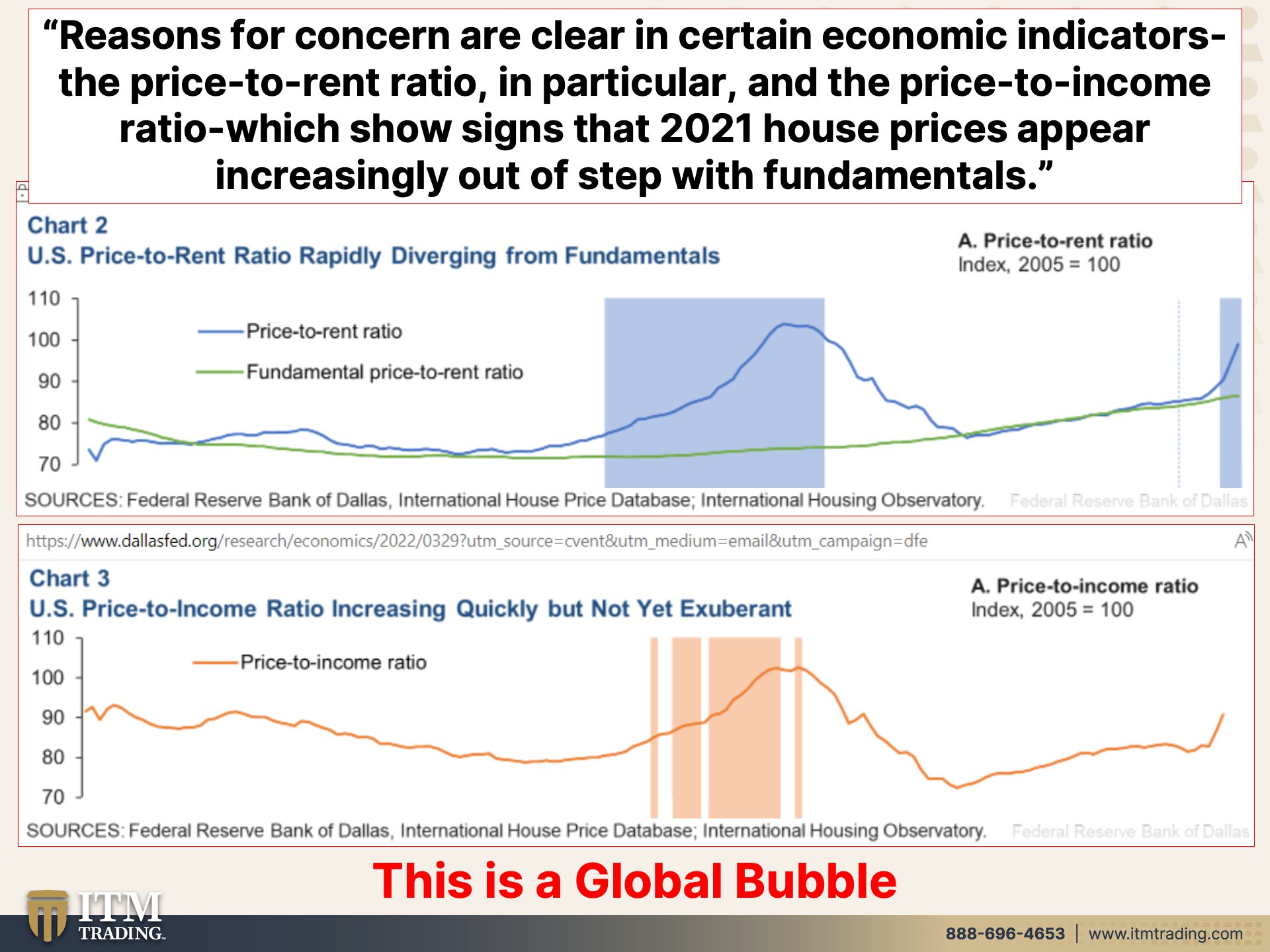

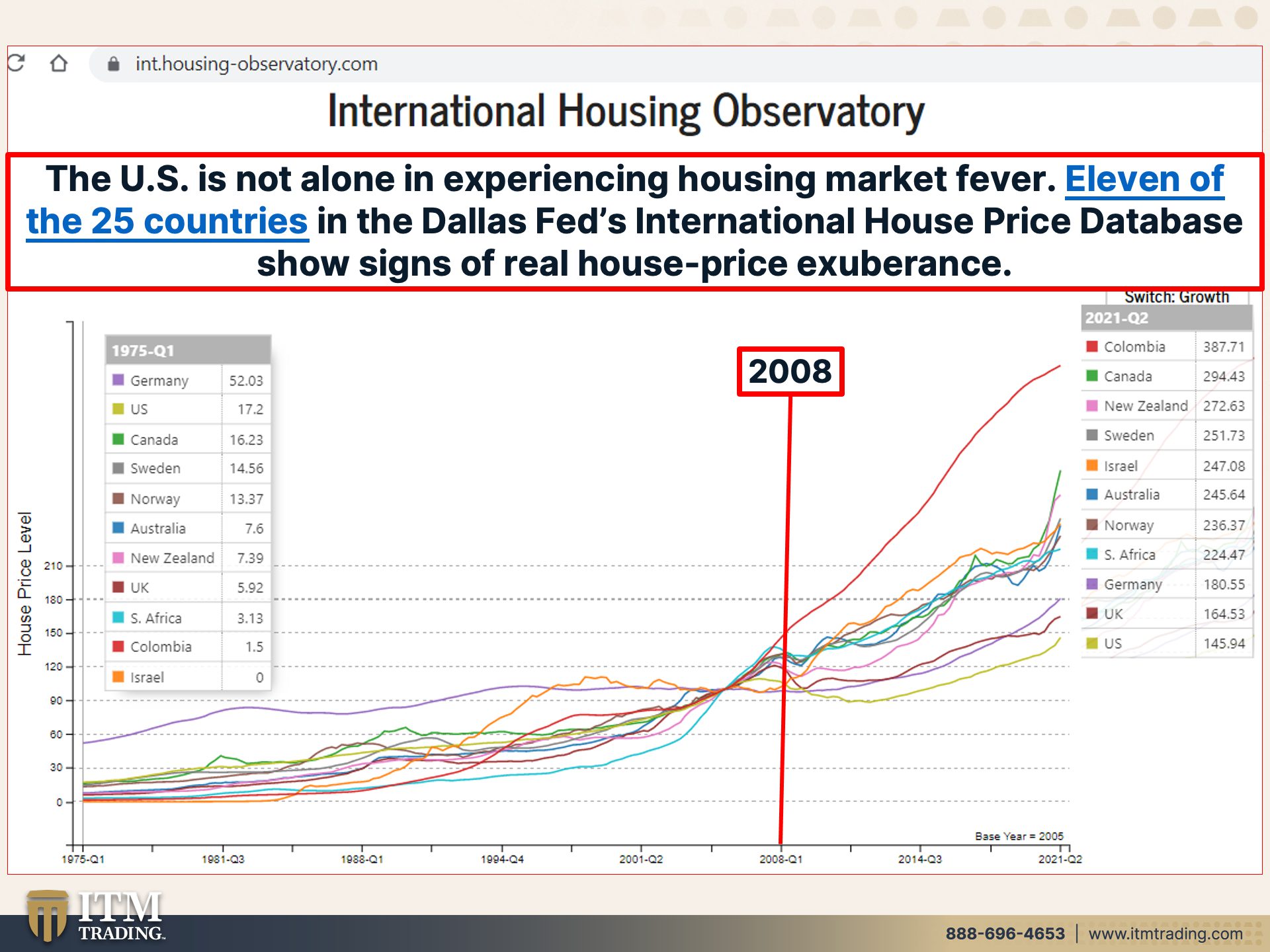

Because really the question is, if they’re raising rates to combat the inflation that they created to destroy demand. I mean, inflation is a lot of money chasing too few goods. And with the central banks, it’s pretty. We know how much money they’ve just been creating and creating and creating poor Edgar <laugh> he’s always gotta deal with this gun now, but it’s true. And it just makes the point. So here is that report from the Federal Reserve Bank of Dallas real time market monitor find signs of brewing U.S. Housing bubble. I, you know, one of the things that I always love is how they never, ever, ever accept responsibility for the manipulations. And then the subsequent unintended consequences that come from that. But they say, our evidence points to abnormal U.S. Housing market behavior for the first time <laugh> oh my God. Since the boom of the early two thousands, which they created as well. They also say they do in this article, admit that easy money policies have led to higher house prices may have fueled a fear of missing out wave of exuberance involving new investors, who’s gonna be most hurt, and more aggressive speculation among existing investors, shocker! You’ve had interest rates anchored at zero while you’ve been pumping as much money as you possibly could into the system. Why in the world would any of the real estate behavior and the prices that are so unaffordable for most people anyway, locking those over valuations. And now they’re popping the bubble and they don’t really have, at least initially they don’t really have any choice. So it’s gonna be very interesting to see when all of this turns around, but let’s just stay on, on housing for now. Reasons for concern are clear in certain economic indicators, the price to rent ratio, shocker, and the price to income ratio. Also, big shocker. And this is happening a, on a global basis. It’s quite simple. People cannot afford the rent and, you know, world economic forum, you will own nothing and be happy and, and have the experience. Well, if you don’t own your home, even if you have a mortgage, as long as it’s a fixed rate mortgage, you know what those mortgage payments are gonna be every month, month after month. But when you’re renting, yeah, that’s a different deal. And guess what? If you owe nothing, well, that means you’re renting everything, that doesn’t work very well. The U.S. Is not alone in experiencing this housing market. I mean, this is such new news, isn’t it? I mean, what are they talking about a bubble? And you could tell, it annoys me so much when they come out way after the fact and they go, oops, we might have a little bubble here.

Okay. Let’s take a look at that a little bit on a global basis. This is back in 1979 and there’s 2008. You think all of this money printing with interest rates down at zero might have possibly? No, no that could not have nearly led to a housing bubble. Additionally, we have a lot of new entrance into this market. So when they’re talking about speculation, we certainly know that a lot of what’s happening in real estate. Well, you know, big corporations can borrow money for almost zero. Now that is changing now, but basically since 2008 at zero anchored at zero, and then what’s happening with them. Well, then they build these behemoth. They build this real estate and either they lease it out, well, actually they may lease it out and generate income, but they take any of the debt and they securitize it. In other words, turn it into a financial product and sell it to you. You for your, I don’t know, where would you, oh, how about your retirement plan? We’re gonna be talking about that next week, by the way, cause we gotta talk about what’s going on there.

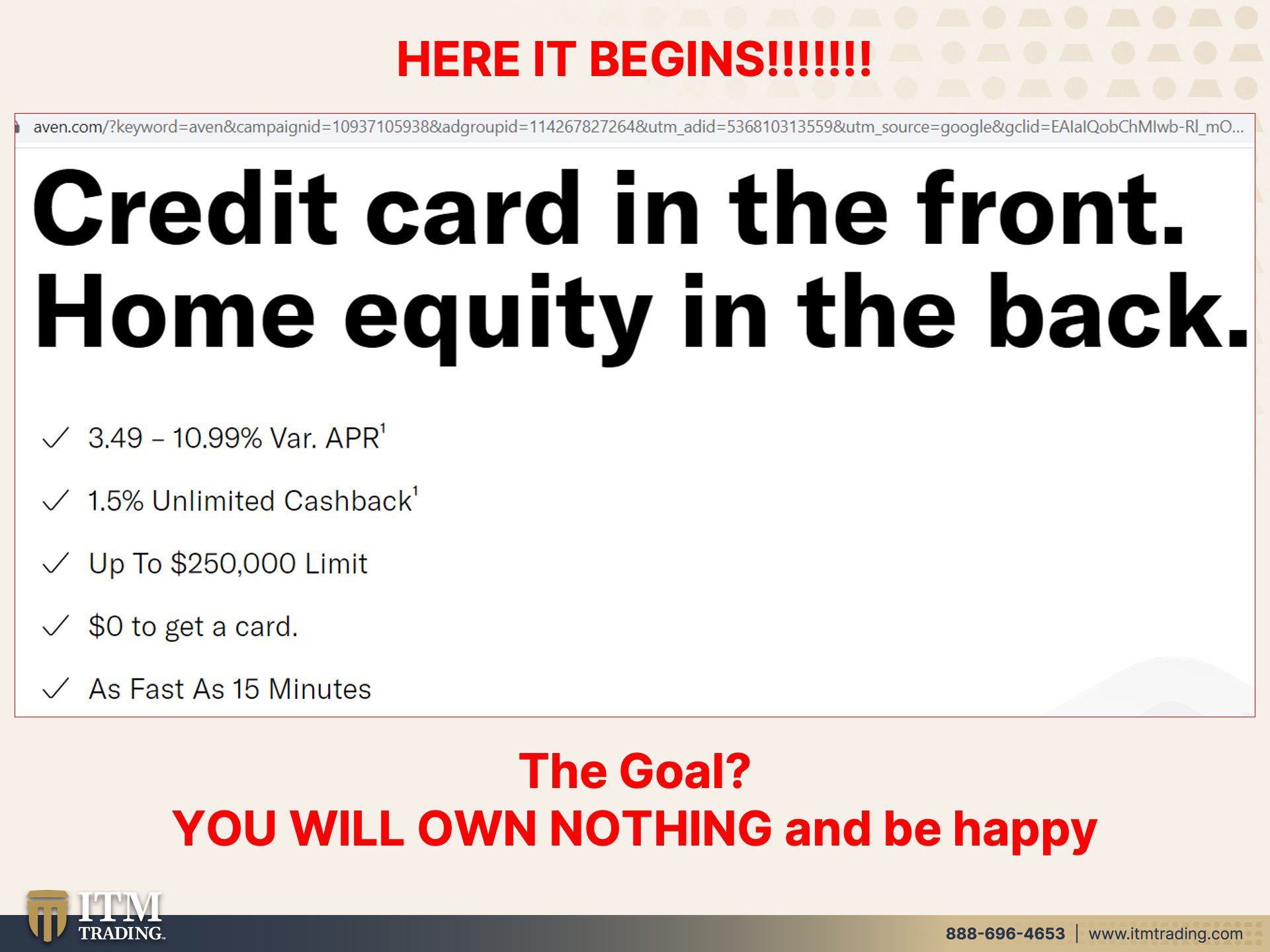

But here it begins. Do you remember a while ago? And I’ve mentioned this in number of times that one of the goals was to have all assets held on a token. So, and then broken down into little itty bitty pieces so that it was easy to spend. Okay, well here’s the forerunner of it. There is now a credit card and if you don’t make a payment, you miss a payment. Well that’s okay. They’ll just pull it from your home equity. Good. Now for those that do actually own their own home, they can use the equity in it. Of course it has to be high. Like we’ve just seen what happens if this bubble bursts and the equity evaporates? Oh, that couldn’t could it could that happen? But remember we’re told you will own nothing and be happy, but you will be ruled by those that own everything because wealth never disappears. It merely shifts location that my friends is the importance of gold of having sound money that holds its purchasing power value. Because this, most likely, I mean, obviously I, I mean, I do have some crystal balls, but they don’t really tell me very much. However, as this housing market bursts, this bubble bursts you or real estate, not just housing real estate, you wanna be in a position to take advantage of it. Like the wealthy have 2008, there was a massive transfer of wealth in real estate from the individuals to the corporations. Well, corporations are doing all of this on debt and the debt bubble has already popped. Now it’s, they’re trying to moderate how that whole thing is imploding, but the big long debt debt boom is over. Cause you know, we’ve been anchored at zero since 2008.

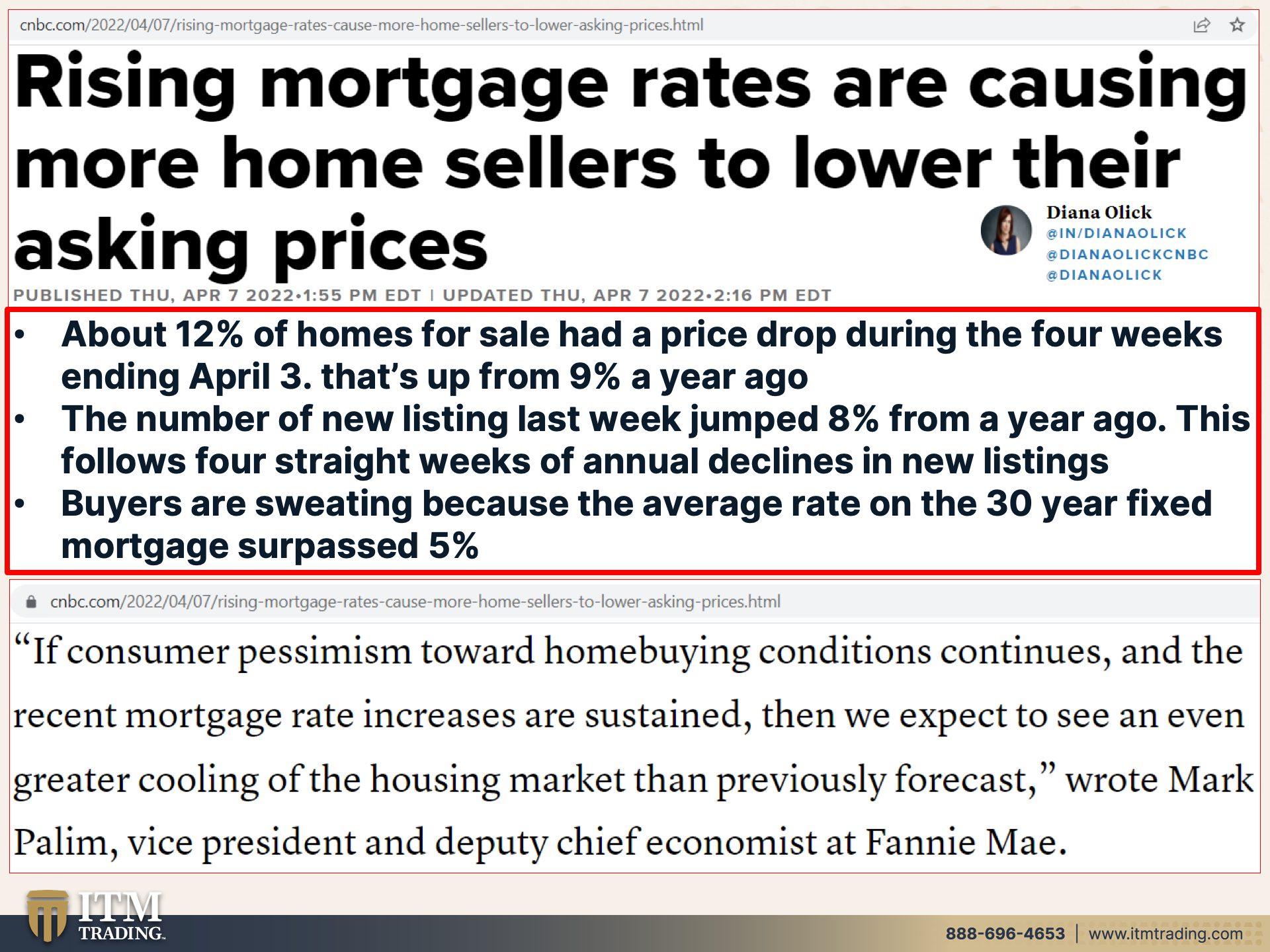

And here is that surge. And because of that surge in mortgage interest rates, total mortgage demand, which would include refinancing, which have virtually dried up, but total mortgage demand plummets 41% year-over-year based on these rising rates or because of these rising rates is a better way to put it. Now, do you think that might have an impact on prices? Because people want to think that this can go on forever, but it can’t, nothing, a tree does not grow through the sky. Everything that goes must come down and now even some sellers are lowering their asking prices. Not a lot yet because people don’t wanna believe that this game is over, but they’re gonna know it pretty quick. About 12% of homes for sale had a price drop during the four weeks ending April 3rd, that’s up from 9% a year ago. So more price drops. The number of new listings last week jumped 8% from a year ago. This follows four straight weeks of annual declines in new listings. So as the housing prices were going up, fewer people were wanting to sell because they wanna get the most out of the real estate that they can. And plus the fact that if they sell it, they’ve gotta replace it at that really high rate as well. So that had been new listings had been declining now that the interest rates are rising. Well, the number of new listings last week jumped just like we’ve seen in IPOs on the stock market when there was a threat of them, of the markets falling apart before that high. And they want to get that out there so that they can capture the most money possible for those suckers that don’t realize what’s happening, but you’re watching you realize what’s happening. I don’t hate real estate, but I do hate it at these price levels. You gotta have a place to live, but you don’t have to speculate in it. You’ll be able to buy it a whole lot cheaper. Buyers are sweating because the average rate on the 30-year fixed mortgage asked 5%. So as these interest rates go up, so do your mortgage payments and if the mortgage, I mean, that’s why that’s a big reason why we could see real estate prices going up with interest and debt in lots of debt issued with interest rates anchored at zero because you weren’t having to pay that interest, that hefty interest, but that’s changed my first house. I’ll never forget it. See, I got married in so long ago. It’s hard for me to remember, but I got, I got married, I think in 77 and we bought our first house in wanna say 79 or 80 and it was 12%. Okay. That’s gonna inhibit the rise in prices on real estate as interest rates go up. And the problem is pessimism. If consumer pessimism toward home buying conditions continues, the recent mortgage rate increases are sustained. Then we expect to see an even greater cooling of the housing market than previously forecast. From Fannie Mae. So for those people that we’re wondering that we’re thinking about selling, If you haven’t done it already, you might wanna consider doing it now before the general public realizes what’s happening. That sounds awful. And it really does. And I hate that, but you know, what’s going on. It’s all about educated choices.

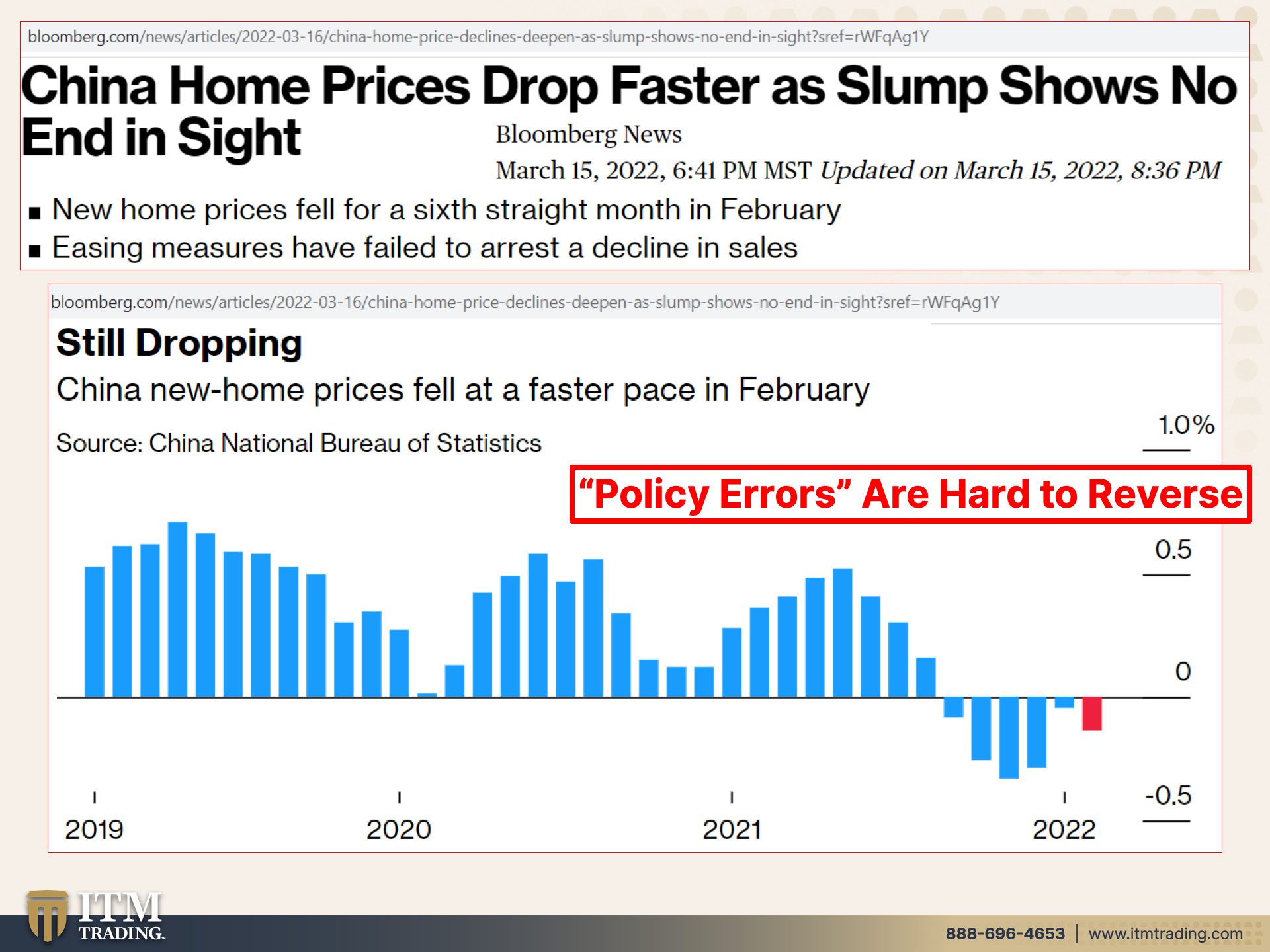

I wanna show you, you know, because in China, I mean just this big, huge boom, big, huge boom, then boom, the government clamped down on mortgages and on real estate because they wanted to try and control what was happening and what they did was they created this huge slump and I’d like to point out easing measures. So now they’ve done it about phase, but easing measures have failed to arrest a decline in sales. I mean, do they think that we are just these puppets and they go, boop, and you’re gonna move this way. And boop, you’re gonna move the other way because, that works for a while. It’s called perception management, but at some point it doesn’t work anymore. And we are at that point, I believe that we are at the point where it simply isn’t gonna work anymore. And policy errors are hard to reverse when they’re this big. And as you know, is the Fed making policy errors? Many believe so and I I’m one of them.

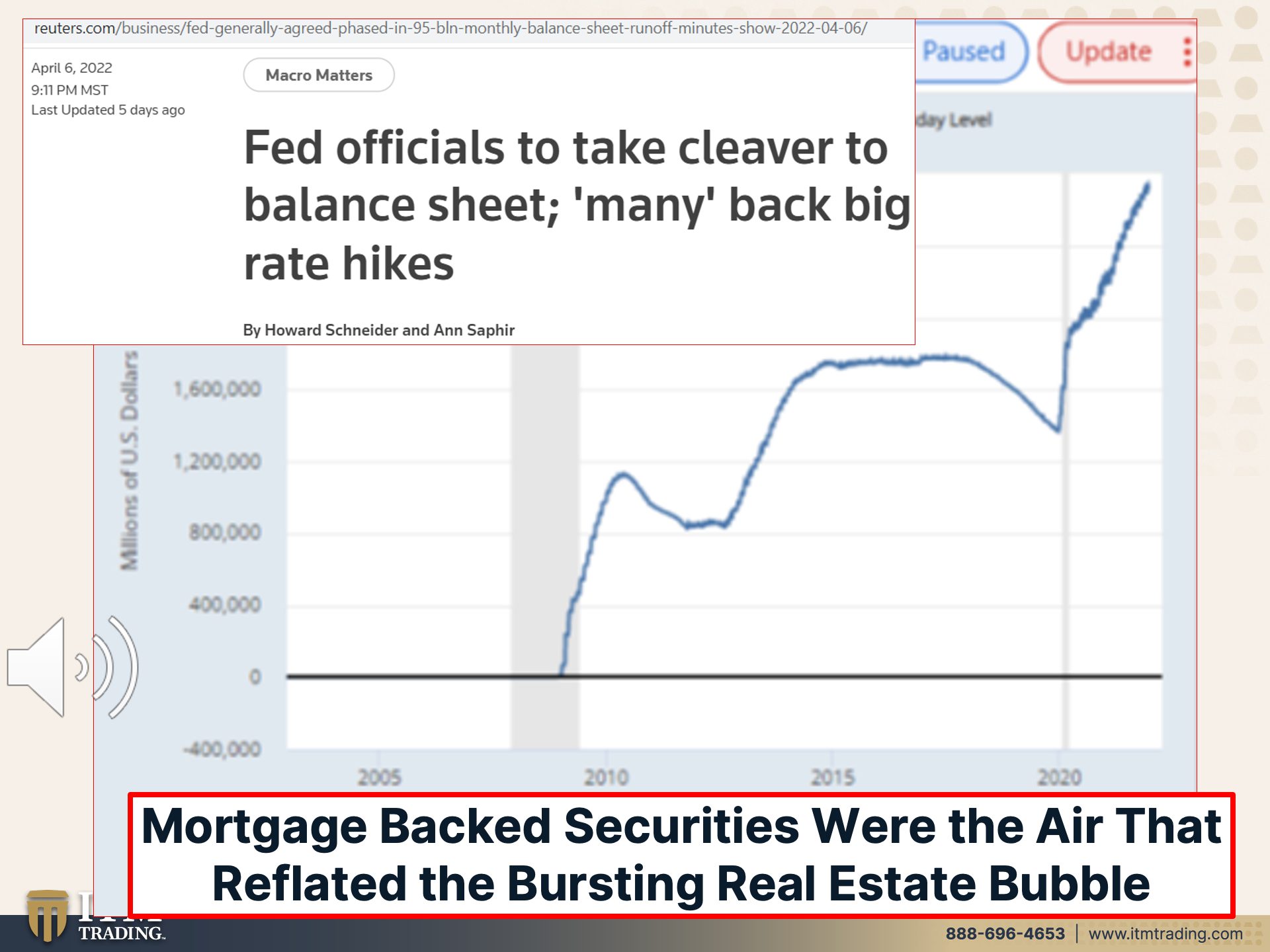

Here’s another big thing. And you need to be aware of this. These are the mortgage backed securities that the federal reserve has bought. And I’d like you to notice that that bot, that buying started in 2009 to reflate that burst bubble. And now they’re talking about reversing it and allowing that balance sheet to run off is not gonna have any big effect? Fed officials to take Cleaver to balance sheet many back big rate hikes. Can they do it? No, they can’t. Do they have to do it? Yes they do. Do you see the circumstance all this time? I’ve been saying they’re between a rock and a hard place and you know, and here’s the thing. Can they tamp down this inflation? In my opinion? No. In my opinion, even though I don’t have all of the technical confirmation, the inflation genie is out of the bottle. People are losing confidence in those controlling it. So the central banks and the governments, And I, you know, I’m sure we’ve started the hyperinflation. I hope I’m wrong, but I don’t think I am, but I hope I am. I honestly do. Because this was the air in that bubble and now they’re talking about letting the air out of that bubble, Big time.

The policy for every segment of the population, we don’t have one for every industry. We have one it’s called the interest rate. The fed funds that’s really it. So it’s a very brute force kind of hammer that we use on the economy. And of course, when you kind of have to use a brute force tool, sometimes there’s some collateral damage that happened. An important voice at the Federal Reserve, Christopher Waller, he’s a research out of St. Louis with some real, real abilities. I will be clear when he speaks experts lean forward and listen carefully there on the hammer of the moment.

So as much talk as there are about all of these tools that they have, that they never really explain because they’re creating all these new things on the fly just to cut. It’s like the Dutch boy with poking his fingers in the hole as the dam is bursting. Well, you got 10 fingers. So once you have all of those, okay, maybe you can even somehow use your toes, but this dam is bursting. Make no mistake of it. And we’re gonna talk more about that as we move through this whole cycle, but make no mistake.

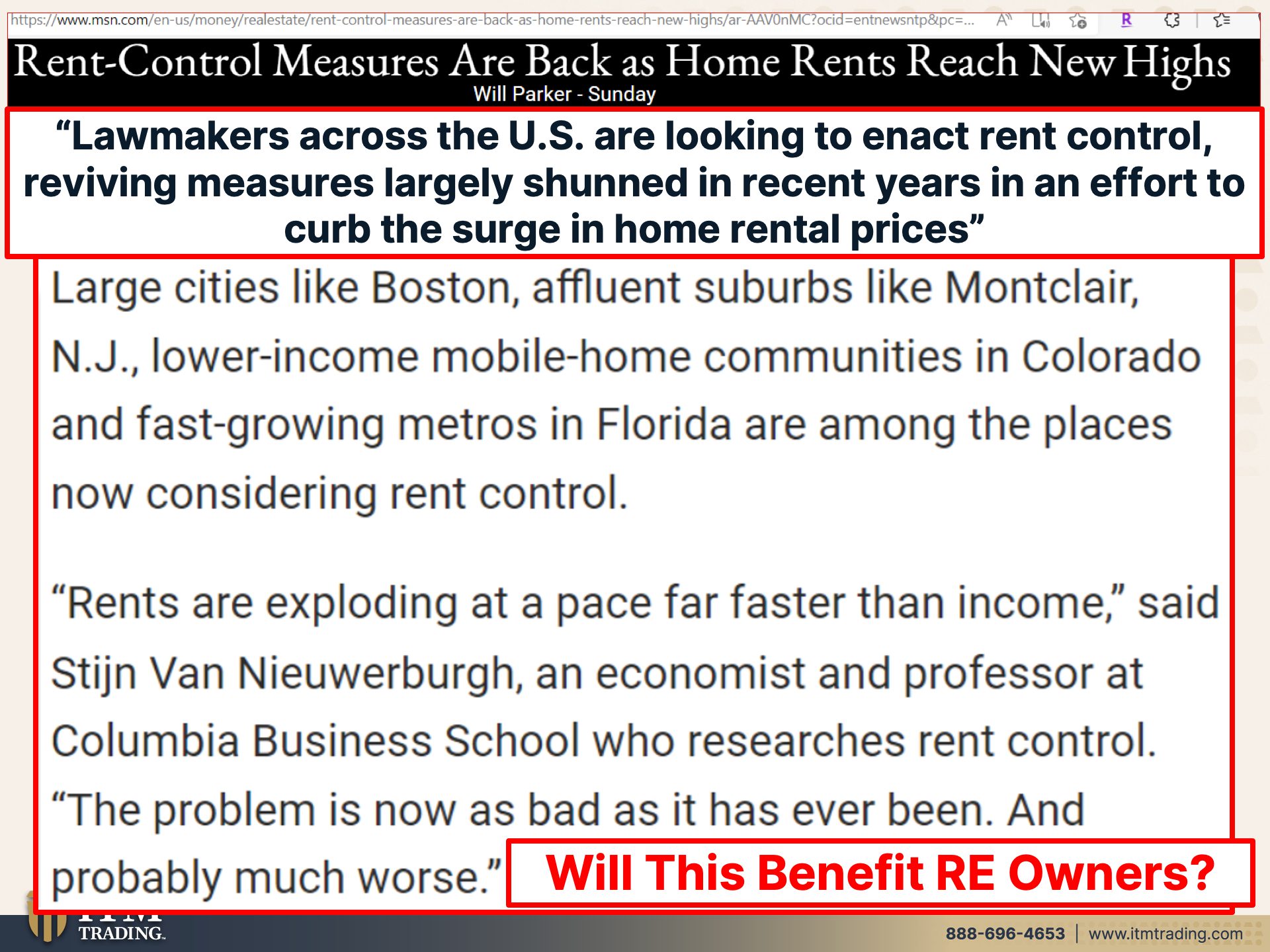

They have one tool. That’s interest rates. Their balance sheet is at nosebleed levels, the interest rates, they need to ratchet it up so that they can lower them down. Are we headed for a recession? Well, worse, look, this next piece has got to be a hyperinflationary depression because they are, they have no more tools. And the new currency that they wanna take us into is still gonna be based upon debt. So they have to burn all of debt off. They have to, there’s really no choice about it. And when we go into that phase, like we saw in 2020 rent moratoriums, mortgage moratoriums. So here, this is a measure that is going through. Lawmakers across the U.S. Are looking to enact rent control, reviving measures, largely shunned in recent years in an effort to curb the surge in home rental prices. I mean, who is gonna get hurt by that? Hmm. We’ll talk about that. Large cities like Boston affluent sub suburbs, like Montclair, New Jersey, lower income, mobile home communities in Colorado and fast growing metros in Florida are among the places now considering rent control rents are exploding at a pace faster than income. The problem is now as bad as it has ever been and probably much worse. Yeah. Ya think? So if you are one of those people that have been buying real estate for income, it kind of depends on what you paid for it. And when you bought it, the fair of missing out, how far can the real estate market drop? I don’t know. I can tell you in Japan that it dropped, residential dropped 85% and commercial dropped 95% and it still hasn’t recovered from it. And that was back in the nineties. How low can it go? I don’t know, but you better, if you’re holding it, you better make sure that you have the ability to boom, pay off that mortgage because it does make it a lot easier to service and maintain your real estate. So you gotta have gold in order to do that. Cause that’s the only undervalued asset, the only one gold and silver physical, and you need to make sure that you can always pay those property taxes, the insurance, all of that. And that’s also where gold comes in. These are the things, these are the dangers of owning real estate. And where did you buy it? Did you buy it somewhere near a high? Ya better. Just make sure that your butt is covered. Oh, I don’t know if I’m supposed to say that, but anyway way, because it won’t be the owners, the real estate owners that are gonna benefit from this.

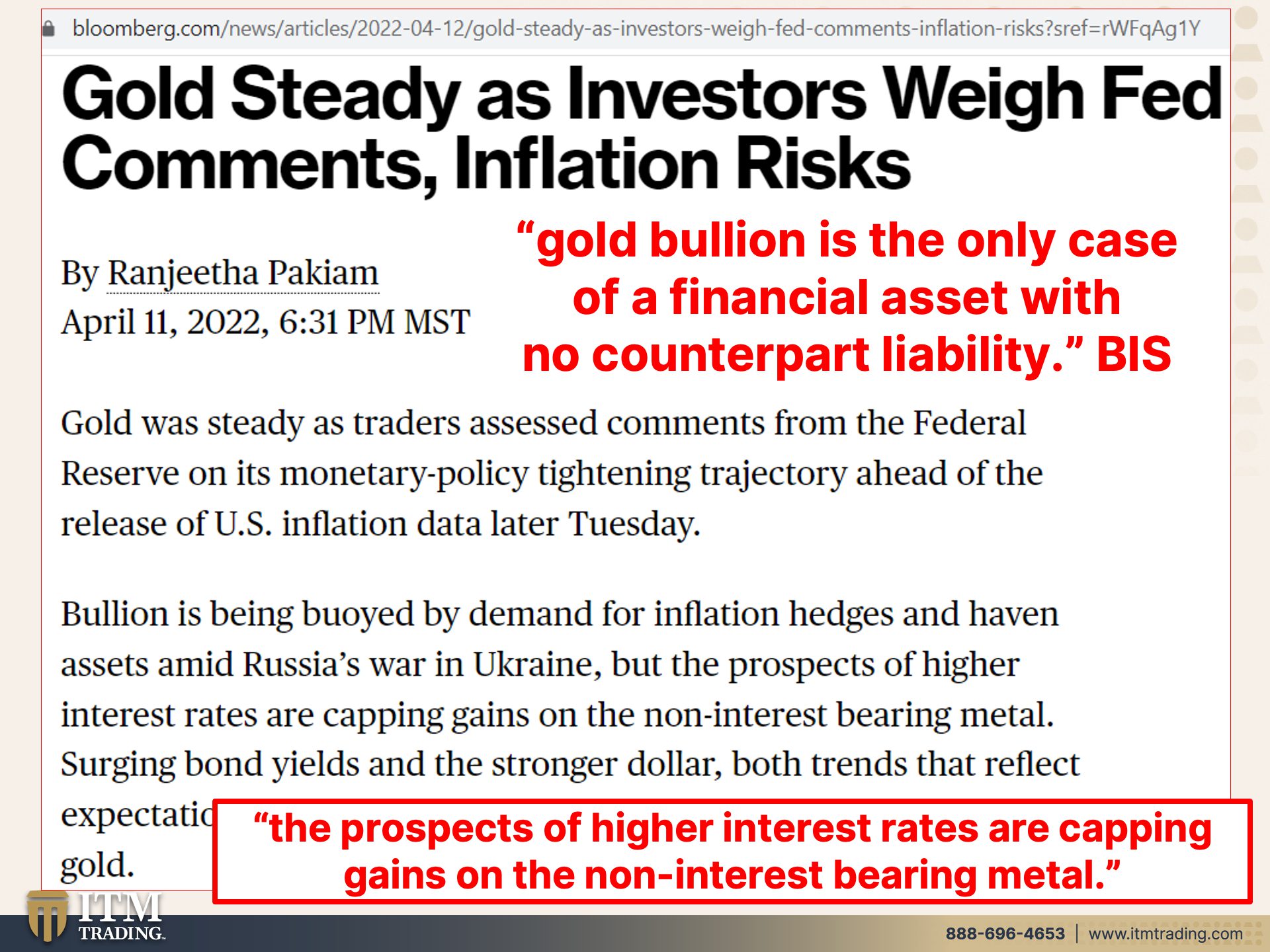

So gold hold steady as investors weigh, Fed comments, inflation risk. But what does the BIS say? Gold bullion is the only case of a financial asset with no counter party liability, everything else we’re talking about today, that’s all debt. That’s all counterpart liability. That means that if your counterpart fails, it’s a contract, right? If your counterpart fails, what happens to you? So that’s where gold really comes in. And a big part of it is that’s why gold is a safe Haven asset. But what I love here is the prospects of higher interest rates are capping gains on the non-interest bearing metal. Ew, why in the world would you wanna hold this? It doesn’t pay you any interest. It maintains my purchasing power. It’s the safest thing that you can possibly do. According to everybody that’s in power. It doesn’t have to pay interest. It doesn’t run any risk. That’s why gold doesn’t pay interest and has the broadest base of buyer. So you’ve got your demand covered.

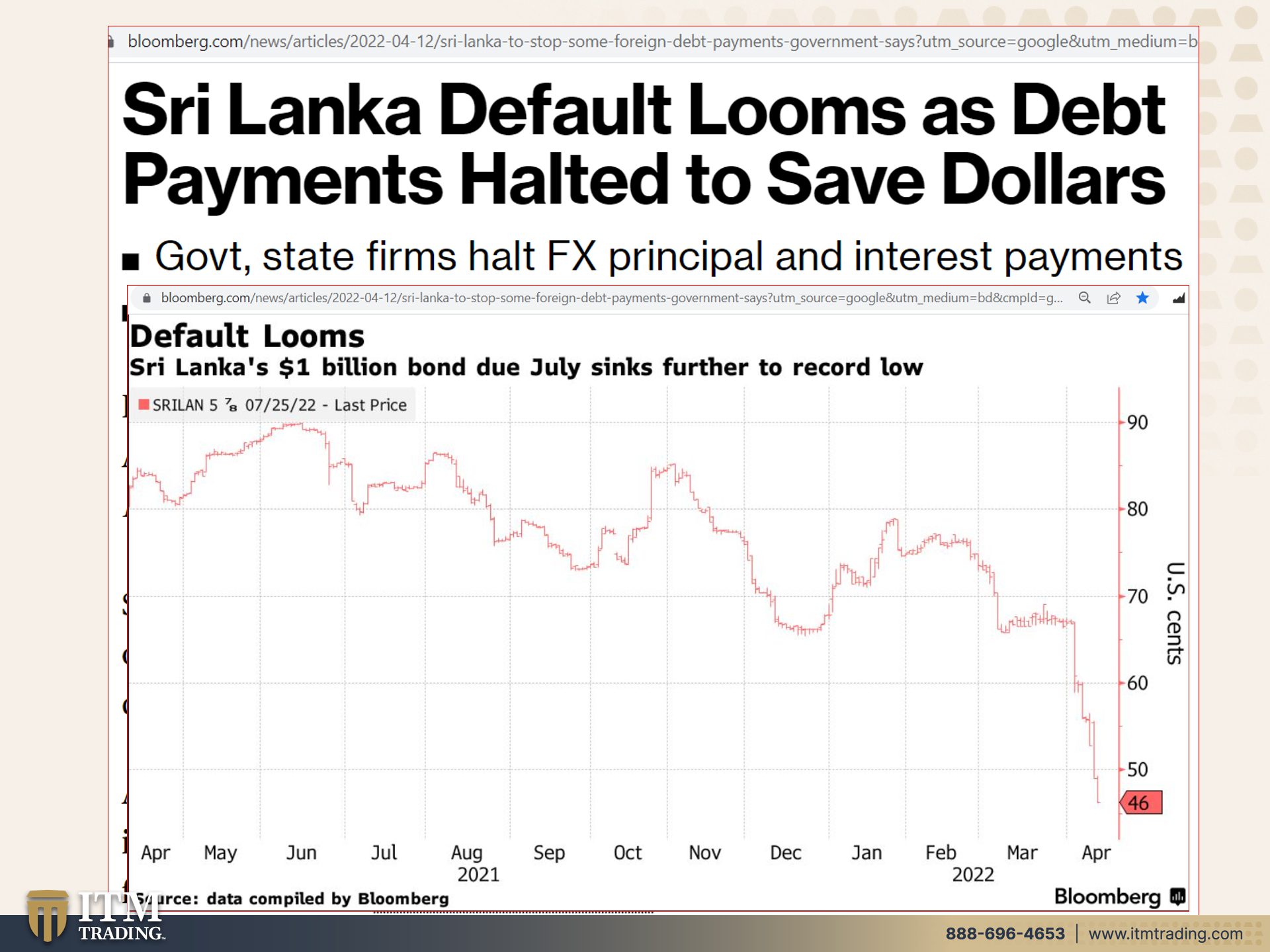

It’s always so annoying because what do you think can happen to government bonds? Hmm. Oh, look at this. In Sri Lanka, default looms as debt payments, halted to save dollars, really for food, for energy, for the public. So if you were holding a Sri Lankan bond, which if you’ve got some of those ETFs or MSCI on emerging markets, etcetera. Yeah, probably do. Let’s see it’s down to 46 cents on the dollar. It’s lost more than 50% of its current market value. At least at the moment that this snapshot was taken, what do you wanna hold? You wanna hold government debt that they are destroying through inflation? Even if it doesn’t do what you’re looking at on the screen. Even if you hold it to maturity and they pay you back in funny money, that has no value? Or do you wanna hold something that’s all that has the broadest base of buyers on a global basis. Doesn’t need a government to say this is money. And it’s why central banks have been accumulating it. I think that we are definite we’re more than beyond between a rock and a hard place. We are in a position that is untenable. They have to raise rates in order to be able to lower them again. That’s why they have to raise rates and to maintain their credibility. Oh, the Fed’s gonna fight this inflation. Oh, this nasty thing that they created. Give me a break would you please? Love to sit down and have a conversation with J.Powell with Janet Yellen with Ben Bernanke with Alan Greenspan. My mother used to say, don’t you think he’s smarter than you Lynn? Don’t you think he’s smarter? And I used to say, I really hope he is because he has a whole lot more influence than I do. But if he actually believes the garbage coming out of his mouth, then no, he is not smarter than me. But he is a whole lot more dangerous. And these central bankers they’re dangerous.

You have to protect yourself. It’s the only way Food, Water, Energy, Security, Barterability, Wealth Preservation, Community, and Shelter. You have to be as independent and self-sufficient, as you can possibly be to survive this mess and community is key because we all bring different skill sets and different things to the table. So maybe you have what I lack and I have what you lack and look at this together we’re a whole, it takes, it’s gonna take a Community to get through this. If you have any variable rate debt, get it paid off ASAP. Because if you think what’s been, the spiking rates have been bad so far, you ain’t seen nothing yet. And I want you to be safe. And because of that, I actually have, oops, I can’t see it. cause I’ve got all the bills in front of it. Here we go. I need a vacation. I’m gonna be honest with you. So I’m going to Hawaii with my family in June and I’m going to take the first day of my vacation for a very small, small group of people. And you’re invited to join us and where are we going? Oh, The Grand Wailea. The link is below. And I’m gonna be talking about things that I don’t talk about or can’t talk about on air. So it’s a small, intimate gathering. We’ll go over. What’s going on at that moment, but really we’re gonna have some deep conversations. So I hope you can join us because again, it’s really super limited seating so that you have a lot of one-on-one time and it’s just a small group of people. Now, make sure that you watch my backyard pond tour on the Beyond Gold and Silver channel. And the video is out now. And it features my very dear friend who just recently passed. I’m so sad about this, cause I really loved him. I mean he hand built my backyard pond one stone at a time that he picked out and he also refurbished all of my other ponds on the property. So that’s my water element. And I’m so glad that we captured this when we did. So this is my tribute to Ernie and he is really missed. He is really missed. Excuse me. Don’t forget that we have podcasts on all major podcast platforms. So listen to it while you’re walking and you’re doing whatever else you wanna do and you can’t watch. But if you have not already started your gold and silvers strategy, just click that calendly link below and have a conversation with one of our consultants because honestly do yourself a favor. You gotta have a plan. If you don’t have a plan, you’re really planning to fail. This is not going away. It’s going to get worse. So if you like the us, please give us a thumbs up. Make sure you leave a comment and make sure that you share, this is a really important video for most people who think, oh, okay, well I’ll do real estate because after all, what do they tell you? Real estate always outpaces inflation until you go into hyperinflation and a currency reset.

And you know, it’s really interesting because I may not know everything about a lot of things, right? I mean, I don’t, but what I do know, are currency life cycle shifts, I’ve been studying them since 1987 and I don’t know anybody else that has. And if you listen to Ben Bernanke or any of the other Central Bankers, mm boy do I disagree with their analysis like so much. And I’d love to sit down and have a conversation, but that’s not likely to happen either. Unless maybe it’s an interrogation room. God forbid, boy, boy, boy, at any rate as always, I really, you know, it’s time to cover your assets, all of your assets. And here we use the wealth shield and it’s a strategy that will serve you well during this transition. So until next we meet, please be safe out there. Bye-Bye.

SOURCES:

Real-Time Market Monitoring Finds Signs of Brewing U.S. Housing Bubble

https://www.dallasfed.org/research/economics/2022/0329

International Housing Observatory

https://int.housing-observatory.com/