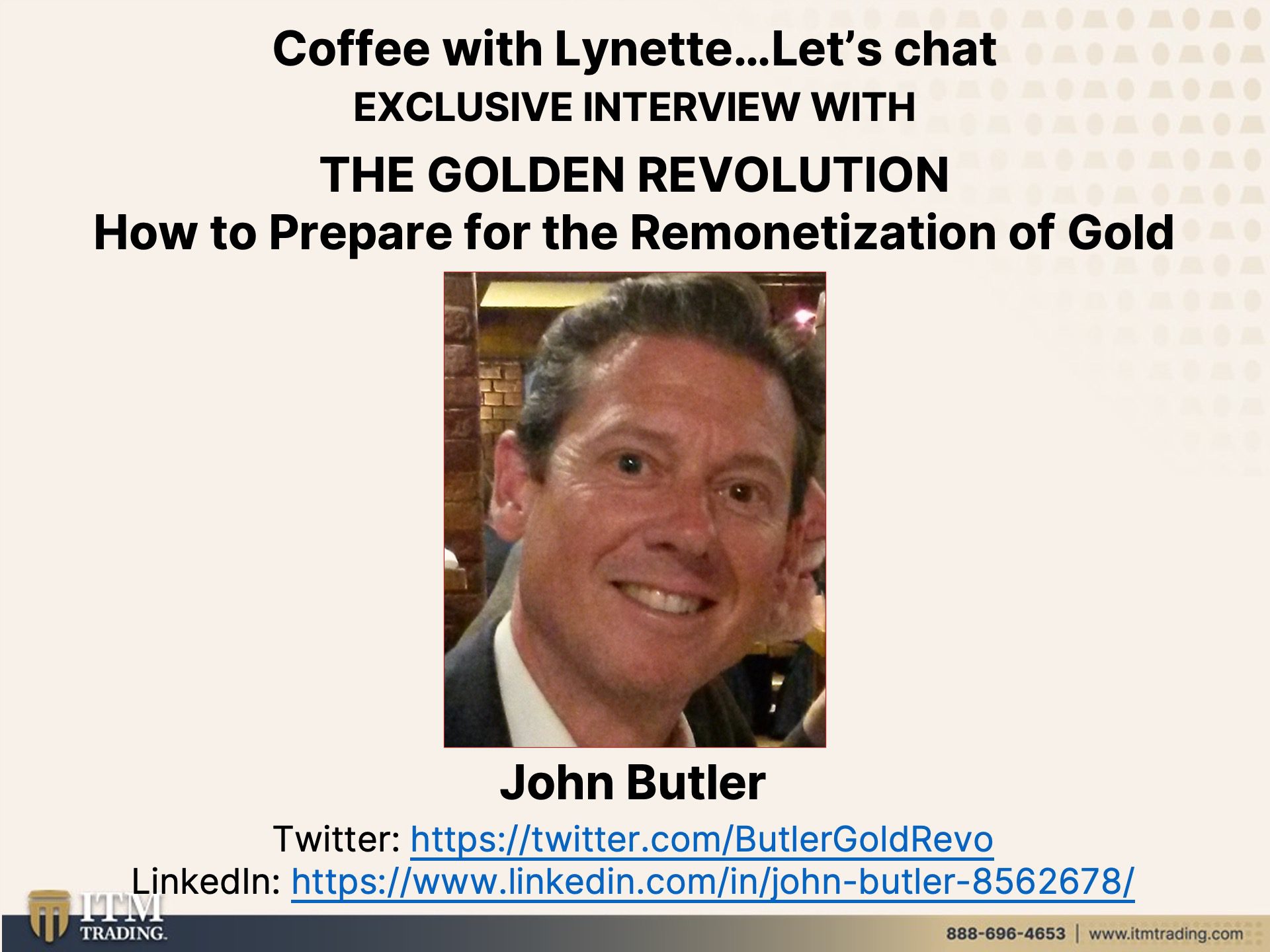

BACK TO GOLD STANDARD: Prepare for the Remonetization of Gold…John Butler & Lynette Zang

TRANSCRIPT FROM VIDEO:

Lynette Zang:

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, a full service, physical gold and silver dealer specializing in custom strategies to help us all survive the reset that it should be clear to everybody we’re already walking through, but I am so excited for this edition of Coffee with Lynette and my very special guest John Butler, who has worked as a managing director for global investment banks in New York, London, Germany, including one of our favorites Deutsche bank and my Alma mater Lehman brothers. He’s advised many of the world’s largest institutional and high net worth investors, including central banks. Now he’s in FinTech and John continues to write on a range of economic financial investment topics. In 2012, he wrote the original here’s the original, the golden revolution, but you know, cycles evolve and they’re evolving so quickly these days that he revised it and updated it to include discussion on cryptocurrencies. But mostly this is a roadmap on how to prepare for the remonetization of gold, which, you know, we talk about all the time at ITM because it’s the historic norm. This I’m telling you right now. You want to read this book. I loved how he supports everything with historic facts to come to his very cogent conclusions with all the insanity in the markets and the chaos in the world. This is a keenly important discussion today. John, thank you so much. I really do appreciate you coming here today.

John Butler:

Well, my pleasure and thank you for that very kind introduction Lynette.

Lynette Zang:

Did I say anything that was untrue? Not at all. Well, there you go. So you absolutely earned that. But the first question that I like to ask all of my first time guests is why you do the work that you do. So not just why did you write this very wonderful book, but why do you do the work that you do?

John Butler:

Well, I guess as the years went by and I began to recognize what I felt were very, very deeply rooted problems in the financial and monetary system. I still want it to advance my career, but I wanted to try to realign it with activities that I thought were more part of the solution than the problem. And given the nature of some of these problems, it’s kind of a black and white decision. It’s, it’s very, very hard to make incremental changes. Sometimes you kind of have to really shift gears in order to, to make that, that, that move from being kind of problem oriented. Not that one would choose that willingly, but you just sort of ended up there to, to being very, very willfully and deliberately solution-oriented. And so that process occurred in my own experience from the mid two thousands and when 2008, 2009, and the boom bust and bail out trio sort of came and went that, you know, that was the coup de Gras for me to change my, my orientation in that regard,

Lynette Zang:

I have frequently said that 2008, and I’ve been saying this since then that the system actually died and just went on life support. Right. That is, and do you have any comments about that and, and what they’ve been doing since, because I think you and I both agree that this quantitative easing all this money printing it didn’t solve the issues that arose in 2008, where it became apparent to the globe at that that’s a much better way to put it.

John Butler:

It certainly did not solve them. I mean, it, it bought time and in principle, if you buy time, you can do something intelligent and constructive with that time, but that isn’t what’s happening. You know, they, they bought time, but as you say, you know, the patient was put on life support and they haven’t really taken any meaningful actions that will resuscitate the patient in a sustainable way that has not happened. And indeed, I would argue as someone who has studied so-called Austrian economics in depth, that what has happened is in fact, a continuation of some fundamental, if difficult to see resource misallocations that are distorting the capital stock, moving, productive capital into places where it’s completely unproductive. And therefore we’re not really continuing to build the productive resource base that we need to provide for our own retirement, for our children’s futures and so on and so forth. So, I mean, to summarize, we’re making a bad situation worse.

Lynette Zang:

Well, so many people say well, but can’t, they just keep printing the money. Can’t this just keep going on forever. What do you say to that?

John Butler:

Well, look, I mean, look, if it were that easy, if it were really that easy and don’t you think we would have arrived Nirvana by now? I mean, yeah, every time somebody promises that somehow you’re running a printing press a little bit faster, will somehow get us to the other side. They’re always wrong. Always. I mean, please find me one exception. I would love to believe in, in the magic money tree, as some people call it. But those of us who are inclined towards reason and logic, you know, find that extremely difficult to accept given the lessons of history and the fact that theoretically, it just doesn’t make sense. So it may be fashionable of course, to justify your present policy proclivities with fashionable monetary theories that make all kinds of sense in ivory tower, academic Lala land. But these, these theories in air, I mean, they just invariably fail when they make contact with the real world.

Lynette Zang:

Well, you know, the U.S. Dollar, you know, as the world’s reserve currency, you know, and the U.S. Central bank, at least in the past, and we’ll see where it goes, but arguably the most powerful central bank in the world exporting its policies. So I’m really wondering what you have to say about the ability for the U.S. to retain its position as the world reserve currency, although it’s been declining quite a bit over the years, but you know, what’s the impact. Do you think, what impact do you think it’s going to have on, on the U.S. Public and on the global public too.

John Butler:

Sure, sure. We’ll look, I mean, things like losing reserve currency status are by definition, not the sort of things that happen gradually and over time. That doesn’t mean the underlying deterioration of what supports reserves, currency status isn’t, but, you know, being sort of gradually cheerleading over time, but the actual events tend to be very, very sudden kind of like supposedly unforeseen currency devaluation or financial crises or things of this nature. And so they can’t be predicted in their precise timing, but they can be predicted to some extent in the generalities of what they might look like and what is going to, you know, what the aftermath also is going to look like. And history is, is somewhat instructive in that regard. And so yes, the, the dollars position as the world’s preeminent reserve currency is being undermined in a variety of ways. I would argue that that process really got going in the mid 1960s. So we’re well along this path now, and it’s a path which arguably is accelerating. I think there are clear indications of that, but even then I would not presuppose the, you know, the, the omniscience to know precisely when this is going to reach its end point or transition point, perhaps is a better, is a better term there. So yes, the, the United States economy is a share of the global economy at the end of World War II approach. 50%, literally half the world’s productive capacity was located in the United States today. That’s closer to 20%, that’s a big change. And that doesn’t mean that the United States is not still an extremely important industrial power in, by any measure. However, that power is increasingly reliant on foreign capital. It’s increasingly reliant on multinational supply chains. It’s increasingly reliant on dare I say the benevolence of the rest of the world to continue to accept you know, the state’s monetary and economic policies, which are not necessarily in their own national interest and beyond a certain point, the politics of this take on a very different dynamic where, you know, John Connolly’s famous statement following Nixon’s closing up the gold window, the dollar is our currency. And your problem is going to transition from the dollar is our currency and our problem.

Lynette Zang:

Yeah. But that, well, how do you think that’s going to impact? Because so many people, you know, I was alive in the, I don’t actually know how old you are, but I’m guessing I’m older than you. And I was like a teenager. I was about 17 right around when we transitioned completely off the gold standard. And you know, of course it was supposed to be temporary, which lots of things like QE that was just supposed to be temporary. And those things have a tendency to become permanent. But I can tell you that as a young woman, I didn’t really understand what that meant or how that was going to impact me, frankly, for the rest of my life. So could you go into that a bit more because I think that’s a challenge for a lot of people to really conceptualize what that’s going to be like for them.

John Butler:

Well, look, we’re, we’re human, right? And even though we can use logic and reason, we’re nevertheless programmed towards what you would call normalcy bias that is to expect that what we have become accustomed to will remain in place more or less in the future subject to incremental change rather than something sudden and surprising. However, when you, you know, when you study history, you realize that, you know, normalcy bias, okay, fine. I mean, it is normally the case and yet these things do happen and the Nixon shock is, is one of them. I mean, that, that is very significant in terms of economic history and also how it instructs us regarding what the future might look like. And so as you say, you know, you were 17, you didn’t really understand what was going on. I’m not sure anyone who’s 17 understands what’s going on, although they might claim to. But but certainly in my own experience, I mean, look, I, you know, I went through my own process as it were of coming out of Plato’s cave, you know, seeing the light, choose your metaphor. And that said, coincidentally back when I was in high school, I had a very enlightened economics teacher who assigned me as a special project studying Hayak the F.A. Hayak the, the Austrian economist as a special project to present to the class. And I was quite astonished by what I found, because it seemed to so contradict what was already clearly the established economic mainstream back when I was young and which remains still the mainstream today, but on, but on steroids right now, they they’ve taken what was supposedly some form of benign economic cycle management policy and turned it into this chronic, as you, as you’ve said, you know, life support policy. And, and so I kind of felt I had a little bit of a better grounding to understand what was unfolding in the mid two thousands as the housing bubble grew out of control when 2008, 2009 hit, and the whole thing came crashing down and the policy response is thereafter. And, and I do see with each step along the way here, I do see historical precedent and useful historical analogies, one after another. And I suspect more and more people are able to do the same, although it’s difficult without some reference to history, it’s really difficult to connect these sorts of dots simply through your own personal anecdotal experience. That’s true.

Lynette Zang:

Could you share some, you know, like a couple of key anecdotes that you think would help people understand it better?

John Butler:

Well, here are a couple of fun stories. I mean, related to what I just mentioned in the mid two thousands, I was at Lehman brothers and they were making money hand over fist securitizing mortgages in various forms. And indeed, literally they were pulling new ways to securitize them out of their hat every week. And it seemed that every new version of whatever CDO squared it was somehow you know, it was more profitable for the firm. It was, you know, it was, it was a license to print money. And, and yet obviously it was clear that, that all of those securities and the generous fees Lehman was earning by creating these, these Comerica beasts were, nevertheless dependent on rising house prices. There really were because there was leverage behind it and the leverage could only be in the debt and leverage behind it could only be serviced in house prices, continued to rise. And so I got concerned when I began to have increasingly frequent conversations with some very good old friends of mine who went into the California real estate market. I’m from California. And they started telling me already in 2006 that the California real estate market was only slowing down. It was practically seizing up in some places. And by 2007, they said, the properties just weren’t moving at all. And that just made no sense to me. You know, here I am at Lehman brothers, supposedly surrounded by the best and brightest people around and they’re making money. Yes. But they’re, but they’re completely not even seeing this reality on the ground as if they’re in their own ivory tower. And I started an issue where I thought were clear warnings based on this California data and the growth in inventory that is unsold homes on the market. And then, and then it began to show up in the national data and they just refuse to see it. And then sure enough, when it all blows up, it’s oh gee, gosh, no one saw that happening. Well, hold on. You’re actually quite a few people did exactly. That’s one story. Another story is this. I, at one point reported to the head of risk management in London, not in, not in New York in London. And he responded to my concerns one day saying, oh, don’t worry, John, the firm has hedged against a major financial crisis. And I was curious of course, to know the details of what that meant. And so he opened up to me in confidence. Although, you know, that said, as a managing director of the firm, you’d like to think you could trust me. And he said, okay, this is what we’ve done. And he went through in detail what the firm had done to protect itself. And I said, okay. So this is based on the 1998 LTCM long-term capital management experience. He said, yes, absolutely. You know we’re totally hedged against anything like that ever happening again. And I said, okay, now answer me this. What do you think the other firms are doing? What do you think Merrell is doing? What do you think Goldman Sachs is doing? What do you think JP Morgan is doing? And so on? How do you think they’re hedged? And he looked at me and said, well, I suppose in exactly the same way, more or less. And then I just looked at him and I said, so let me get this straight. You think that, by hedging out our risks without with those other counter parties who are the market, you think that we are hedged against everybody going down same time, because they all have the same position on, if you all have the same position on, none of you are hedged and the market cannot hedge itself out to a non-market, it’s got to net out internally.

John Butler:

And he couldn’t see this childlike logic because the equations that were in this, this, this hedging matrix algorithm thingy that he and his rocket scientists team had developed, that you couldn’t, they couldn’t see the forest for the trees and, and, and shore it up. But it all blew up about a year later, he sorta like, gee, John, you were right. But I still don’t understand why, what, whatever. I mean, yeah. Some people are too smart for their own good, I suppose.

New Speaker:

Well, yeah. I mean, you mentioned longterm capital management. They were supposed to be the smartest guys in the room.

John Butler:

Right.

Lynette Zang:

Hey, but how did that work out? Well, they got bailed out and, you know, I think, you know, you kinda, you said a couple of things, but one thing I want to definitely talk about is you mentioned that, you know, you could see what was happening, but here are these really smart guys that couldn’t see it. And I’m wondering if there isn’t a similarity between the public watching the stock market go up and the real estate market go up and watching all these markets go up and thinking everything is fine because that’s the training

John Butler:

Oh absolutely. And this goes back to the normalcy bias, especially look, if normalcy bias is entirely natural and you combine that with making money hand over fist day after day, who in their right mind is going to want to end with that party. I mean, you’ve got to be a, a really, really sort of non-conventional thinker or perhaps just paranoid, who knows. I mean, if you’re skeptical,

Lynette Zang:

at least skeptical.

John Butler:

But, but these people are in the minority as a psychologist. You know, those who study human psychology know that sort of thinking is in the minority. That’s why the so-called herd mentality exists. And that’s why things go in cycles. And that’s very important to understand everything goes in cycles. It comes down to human nature. Human nature in that social way is cyclical. Hence the patterns of history and hence what I call the monetary cycle of history. So the same sort of psychology ultimately helps to explain why we go from good money to bad money and back to good money throughout history, money starts out, okay. People then start printing a bit too much, get away with it for a while. Everyone’s happy because everyone said, everything seems fine. And then yet at some point, things began to go wrong. And ultimately the only way to reset the system is to return to good money. Hence the prediction in my books that we are eventually going to see gold remonetized in some way. I just don’t see another way out of this.

Lynette Zang:

Well, what about cryptocurrencies? I mean, Bitcoin came out in January of 2009 same year that they started the rapid quantitative easing because rising money supply is, you know, a given over time for inflation. What about, well don’t you think that something like that and the CBDC’s, which is another kind of topic, but let’s talk about that because people think…

John Butler:

Okay, let, yeah, let’s separate the two topics because I actually think it was important to make that distinction. So, okay. So the, the, the whole crypto phenomenon is a fascinating one and I’ve been fascinated by it from the beginning. I read the original Satoshi Nakamoto paper back in 2011 and began to very, very casually on the side follow the development of Bitcoin. And then the other upstart currencies that were launched in particular beginning around 2013, 2014, it really began to go well, somewhat mainstream. I might be exaggerating a bit, but I think that it was in early 2014, that both Newsweek and the New York times ran prominent articles in the business, in their business, ink and economic sections about Bitcoin and the cryptocurrency phenomenon. And at that point, I began to actually put my thoughts to paper and writes on occasion about a cryptocurrency. And indeed some of those thoughts found their way into the second edition of my book and other essays I’ve written along the way. And look, I admire it because crypto as a new technology solving. well Bitcoin, specifically solving the so-called Byzantine generals problem, which allows for independent third party verification of transactions without the necessary recourse to a central authority. I mean, that, that really is in a way, a work of genius. However, it is a work of genius that may provoke a phenomenal discussion about what is money, what should be money is our current money working? Could we do better? That’s all great. But Bitcoin itself, as a practical money requires a colossal electronic infrastructure to maintain one that generates an exponential amount of power to support the growth of that infrastructure. Now, some very clever people are working on solving that problem and trying to reduce the energy costs associated with maintaining the Bitcoin network. However, every attempt to do so necessarily creates a points or nodes of centralization. Those become points of failure. They’re exchanges. They are parallel networks such as lightning or taproot. So the Bitcoin ecosystem and the crypto ecosystem more generally is evolving and I’m pleased to see it evolving, but it has yet to demonstrate that it can offer the myriad benefits of sound money at an acceptable cost. I have yet to see that, now, but all of that, all of that is different than CBDC’s. I look, I’m going to get a bit cynical here. CBDC’s are just a Johnny come lately way for central banks who try to steal crypto’s fire, take advantage of the zeitgeist, come out with their own digital currency, which GE by convenience is easier to print, easier to devalue, easier to manipulate and easier to confer benefits on some privileged groups over others that have easier access to it, or pay lower fees to use it or whatever it is. I, I, I really think CBDC’s is just an extremely, extremely dangerous road to go down. If you’re abusing a printed currency, my God, imagine how you might’ve used a digital one that doesn’t even have the constraint of the printing press. You don’t even need trees or whatever material goes into banknotes nowadays. So, you know, that is great. Cause for concern in my view,

Lynette Zang:

I would agree particularly since the big problem that, well, one of the problems that it solved for central banks is distribution of their policy directly to the public. And they can then see in real time whether or not their experiment is doing what they want it to do. And if not, well, what we’ve seen is insanity because doing the same thing over and over and expecting different results, but, you know, can you comment on, you know, do you think that it’s really gonna take hold? Because even China, who’s further along than anybody has had, you know, basically a lackluster acceptance of the digital Yuan as a payment method versus the others that are already out there in popular?

John Butler:

Well, look, I mean, they may tout CBDC’s as a superior technology and claim. They’re not doing the same thing again, they’re doing something different, but actually in terms of what are the implies for the quantity of money, what are the implies for interest rates? What are the implies for resource allocation, etcetera, etcetera, is all, as you say, pretty much the same. And I do really question whether central bankers are still saying, and indeed, sometimes where I’m asked gee, John, you know, why do you support return to the gold standard? I say, well, it’s because it will put central bankers into a golden straight jacket. They just won’t be able to play these games anymore. They will be severely constrained in their ability to manipulate the money supply. And that will put it in to these attempts to basically take over fiscal policy, which, which is the logical end in a way of what the monetary authorities are doing. Monetary policy already has distributional effects. That is it, it favors some groups over others. It favors those who are asset rich and income over. Those were asset for an income rich and it favors the, the older, over the younger it favors debtors over creditors and, and that’s just not fair. And we see that showing up in the inequality statistics. And so, you know, the sooner we start, we start this out the better.

Lynette Zang:

I love the fact that you’re always hearing, especially these days about how they’re trying to solve the inequality problem. Like that just kind of happened. Can you explain to our viewers how that has happened?

John Butler:

Okay. Here’s a simple way to explain it. Let’s say you take two households going into 2008. One of whom is quite wealthy and has lots of properties, lots of stocks, and the other is younger. And both, both both the parents have an excellent job. They’re very, well-trained, they’re both making six figures, but they have yet to accumulate much in the way of assets, because that’s going to take a couple of decades even at their higher earnings level to get anywhere near, as wealthy as this other family. Well, what happens following 2008, 2009 is that the central bank creates all this money, which largely gets stuck in the banking system and is really only pushed through the banking system, into the real economy, through borrowing against existing assets that isn’t, you already had assets. You could borrow against those assets for very, very low cost and acquire more assets. Whereas that high earning young family, without the assets does not get this benefit, they can only borrow in, in, in, in more or less unsecured fashion, or by putting a lot of money down on a house, which will of course soak up what assets they had managed to scrape together by that early point in their careers. And so as the years go by, and this situation remains in place year after year after year. Now that young couple, they have a couple children, they’ve got to finance those children. They might choose to pay for schooling. They might choose to pay for other you know, things that cost money. And they’ll find now as the asset values of property and stocks, keep going up, up, up as the wealthy, keep borrowing against those assets, that younger couple with income, but not assets. They’re just always behind. They’re always swimming against the tie. And as they try to maybe move into a larger house, they find that even their nice incomes and their ability to save hasn’t kept up with the asset price inflation. Whereas the wealthy family just rides the way, you know, the older woman, family, they just ride it along and they don’t need to liquidate assets. They just keep borrowing against them to add incremental liquidity when and where they need to. And as long as asset markets don’t go down, they’ll never get a margin call and never need to pay it back. Whereas that younger family never gets that benefit. And so you create what is effectively a two tier society between the asset rich and the income rich, of course, there’s the poor, poor, which, you know, are suffering regardless. But the aspiring young middle class, young educated hard-working middle-class are the biggest losers from this. And it’s just so unfair because these people are our future. These are the people that make our society a better place. And I just think it’s sad that we’ve ended up in this sort of situation.

Lynette Zang:

Absolutely. Because they’re really the producers. They’re really the ones that make things happen. And you know, how decimated has that, you know, socioeconomic area been in this case shaped recovery we’re experiencing exactly,

John Butler:

You know. Yeah, it is. I mean, it’s, it’s also politically destabilizing and I think you see evidence of that now, now I’m not looking, I’m not an expert in these things. And I, I would not, I would not presume to be able to claim that the growing trend towards populism, not only in the United States, but in much of the developed world, linking that directly to the inequality trends that really got going big time post 2008, it’s a bit of a stretch. You can’t really do that. Like for like empirically in a robust, you know, mathematical scientific way, but anecdotally, wow. It really looks like it to me, it really, really looks like that’s what’s happening here. And so what is initially economically destabilizing that is creating a K-shape recovery, as you say, ultimately, it becomes politically destabilizing and that’s just bad news all around.

Lynette Zang:

I mean, well, there’s somebody, but how are we going to wash out all the garbage that is in the system now?

John Butler:

Well, an attempt was made in the early eighties. I mean a pretty successful one in some ways by Paul Volcker who had who had the, you know the whole support of Reagan and most of his cabinet. And, and for that matter, Congress, mostly there were, there were some congressmen who were, were very, very angry with what Paul Volcker did in the early eighties raising interest rates. But for the most part, there was a consensus by them that the, the, the, the fallout from the Nixon shock, which really showed up when Carter was president big time that that simply needed to be dealt with. So there was a political, there was a new political consensus beginning in 19 79, 80 corresponding with Reagan’s election to really try and get this under control. And indeed, I mean, that was, that was, that was successful. I mean, no, no one could say that was not successful. Not that anyone would have wanted to have to go through that, but, you know, given the choices that were made in the mid sixties, such as Johnson’s great society programs, and then Nixon breaking the you know, the gold standard Bretton woods arrangements, something had to be done. The problem is this is that the system is so much larger today. There’s way more leverage, way more debt. The workforce is far smaller, real income growth has been far lower. To go through something similar this time around would be so much more painful, so much more difficult. Now that said it could be done, but it’s going to require, and even larger political consensus, even more leadership, and even more willingness to persevere and endure to get through to a better place than was necessary in the early 1980s. And I, I certainly hold out hope that the new American and for that matter other countries that are affected by this, I hope that underlying will to retain our institutions economic and political. I hope that will is there, but sometimes I doubt it.

Lynette Zang:

I don’t know. I would, I would question that and you know, part of it too, when Paul Volcker pushed those overnight rates up all the way, didn’t that give the central banks ramp room because every time we hit a crisis, would they do, they lowered the rates like five and a half to five and three quarters percent to inspire that buying printing lots of money. So we’ve had this 30, some odd year bull market in bonds because of the interest rate hike in the eighties. Now we see this bifurcation as inflation is heated up quite substantially on a global basis. Some countries like the us are maintaining basically their reserve policies, zero interest rate policy. Others like Turkey attempted to raise rates, Mexico, some south American countries, but since 2009 you know, every single country, including the U.S. That has attempted to raise rates that has attempted to run off their balance sheet and reduce that leverage every single one has failed. So do you think we have the moral fortitude and stomach and would that work again, like in the eighties because the financial system was so much

John Butler:

Look, as I say, I would like to think we could pull it off, but I’m not optimistic that that we can. And so ultimately we’re going to have to go through a very, very difficult transition period. And I believe that the best way, the least disruptive way to get to the other side of this is to remonetize gold sooner rather than later, and just get it over with right. You know, learn how to live within your means for a change know, stop, stop it, stop expecting future generations to service the debt, run up by current generations, which is supporting an increasingly bloated welfare state. And don’t get me wrong. I don’t nothing against the people who are receiving or are the beneficiaries of that welfare state, but they need to wake up and realize that, you know, they are they’re going to have to find a way to wean themselves off that if this is going to succeed. So, you know, something’s got to give, then everyone has their part to play. Sadly, I don’t get to see any meaningful, serious political will to make the necessary decisions. But if someone were to have the gravitas, the charisma to get a mandate, to remonetize gold stabilize the money supply and therefore it’s rationalized government finances, because it would be absolutely essential to do so. Actually I think that, you know, following a period of a few years, whatever, there would be an economic Renaissance, but we would have to have the patience and the strength of character, individually and collectively to get to the other side.

Lynette Zang:

So you’re kind of talking here about the difference between an orderly transition or a disorderly transition. So what, so what, you know, since, since it is really, frankly, not likely than any politician or any central bank is going to go for this orderly transition because they just keep reflating and trying to keep these bubbles going. What does a disorderly transition look like for you?

John Butler:

Right. A disorderly transition is one that is caused by the United States, not seizing the initiative of its own accord, but allowing itself to be overtaken by events internationally. This is where in my book, I go into a discussion of game theory and I think it’s a very important part of understanding where we are in the monetary cycle of history as discussed earlier, the dollar is the world’s reserve currency that allows the United States to borrow at relatively low cost to the rest of the world in order to finance its government large assets. But that’s only the case. As long as the rest of the world is willing to accept dollar assets indefinitely in exchange for subsidizing us imports from the rest of the world. Now, that sort of policy that is from the perspective of the rest of the world an export led growth policy has been successful successful for Japan in the 1950s and sixties, as well as Germany at the same time, to help them rebuild from the rebel of the second world war more recently, and over the past 30 years or so, it’s been a successful for China as a way to grow out their economic infrastructure by exporting competitive leads to the United States. But all of these countries are now creditors of the United States, which is a huge net debtor to those countries. And when you look at this through the lens of game theory, it actually begins to look a little bit like that card game, old mate, that many of us perhaps played when we were children. And I know it’s not exactly politically correct, but it is a useful metaphor for understanding where we are. There comes a point where no one’s going to want to hold dollar assets anymore. We’re not there yet, but there comes a point where a majority of the United States is former creditors are simply not going to want to continue to accumulate dollar assets in excess of those being accumulated by the other players in the game. And once one country, even a small country makes a small move to slow, stop or reverse their accumulation of dollar assets. All the other players in the game will take notice and adjust their strategies. Accordingly, this will lead to a shifting equilibrium regarding the willingness of foreign creditors in general, to finance dollar assets, dollar borrowing, government deficits, and the U S is ability to service those deficits and debts. And then the game will accelerate and the U S will phase higher interest rates. And it will face higher interest rates at a time when its debt is the highest it’s ever been relative to national income. That’s when the game ends. However, what does it then turn into? The fact is all of these countries will still have economies. The United States will still have an economy if nobody wants to accumulate excess dollars anymore, how does the game continue? It continues by placing another reserve asset at the center of the system, our reserve asset, that nobody can print to their own benefit. Nobody can manipulate to their own benefit. Nobody can force foreign creditors to take or hold excess balances in an asset that is universally voluntarily accepted. And that can not be arbitrarily manipulated or devalued by any player in the game. There’s only one asset that ticks those boxes. That is gold.

Lynette Zang:

Yep, absolutely. Now you also said something that’s pretty inflammatory, and I want to talk about it because you said that on a gold standard, central banks are really not necessary

John Butler:

Now under the classical gold standard system, some of the countries involved in that system back in the 19th century did have central banks, but the role of those central banks was severely circumscribed. Basically they were there to help regulate the system in particular, to help wind down banks that got into trouble through excessive debt and leverage. Okay. And the bank of England in particular was active in that regard. In fact, it was so active that the bank of England was under constant criticism, that it was to really, to bail out banks that got in trouble and that it should actually be a hell of a lot tougher. And Walter Bagehot, a very famous UK economic journalist during the mid 19th century famously said, that the only legitimate role for a central bank in a healthy capitalist economy is to lend freely, but at penalty rates of interest against good collateral. Nowadays, the fed and other central banks, every time anyone gets in trouble or a crisis comes around, oh, sure. They lend freely, but not at penalty rates of interest, maybe zero instead and against and against any collateral central banks are buying everything. They’re buying mortgages, they’re buying corporate debt, they’re buying junk debt. They’re buying equities, they’re buying anything. They can get their hands on. This goes so far from the original mandate that central banks had under the gold standard. It’s like night and day. And as I do argue in my book, you can easily make a case that under a gold standard, you can simply allow the market itself banks themselves. That is commercial banks to set interest rates in a free market and banking can begin to look like an ordinary industry. One that actually competes one that has to set prices for itself and with customers, one in which when a firm gets in trouble, it’s either taken over by competitors, or it goes bankrupt. That is an industry that has to produce the services. It produces at a price that people can reasonably afford and are willing to pay. And if it can’t do that tough, it’s going to suffer. Profits will decline and executives will not receive outsized bonuses for substandard performance banking would look like that again, if we went back on to a gold standard,

Lynette Zang:

That’s kind of a dream, you know, it’s kind of a dream because financialization of the whole industry, I mean, the financial markets are the largest part of GDP. And all of that seems to me to be so artificial because these days it’s based on trading revenues and derivatives and well,

John Butler:

But think about it this way. What is the social purpose of a financial system? What a financial system allows people to borrow today, if they need money or people who have a lot of excess savings to earn some interest on that savings. And then of course at some future point in time, whoever borrowed pays it back and whoever didn’t need the savings back then gets their savings back in future and can spend it on something else or roll it over, whatever it is. So, first of all, you’re doing this time arbitrage as it were, but you’re also doing it between industrial sectors. Perhaps the energy sector is very profitable in generating excess cash, but the automobile sector is not profitable. It is in need of extra cash to perhaps modernize its factories. Well, the financial system can sit in the middle and arrange for money to flow from one to the other. So over time and in space between industries or households and businesses, the financial system can be the intermediary allows capital to flow through time and space, how it should flow to best service society. That is from relatively unproductive uses to more productive uses over time, thereby facilitating the general growth of the economy over time, but really how much should that be worth in terms of value added? That is if the real economy is say a hundred units of productivity, should the financial sector really be more than say, 5% of that 10% of that? How much should they have just to be facilitating the flow of capital rather than actually producing anything themselves. And when the share of the financial economy grows to, you know, 20%, 30%, 50%, you know, something’s wrong, the middleman should not be getting half of national income, right. So outrageous. And yet, sadly, that’s kind of where we’ve ended up.

Lynette Zang:

So, you know, the, the magic question, and I know timing is, cause people ask me this all the time. I mean, who knows when, but when you look out there at the sheer insanity, it’s hard for me, it really is hard for me to watch these markets go up and Hey, earnings, season earnings are great. And I know we’re running a little bit long here, but, you know, can you just address inflation and corporate earnings and all of that a little bit because people, you know, somebody that doesn’t understand what’s going on, will go, but look at the earnings are great. So the stock market can justify these high price, earnings ratios and all that garbage.

John Butler:

Okay, well look, first of all, modern accounting methods allow for a hell of a lot of focus Pocus. And so earnings are not as hard in terms of their economic data quality as they used to be once upon a time. But, okay, let’s leave that aside for a moment in the early stages of an inflation corporate profits can do just fine. And the reason why is because in the early stages of inflation, you tend to get a general pickup in demand because everyone simply thinks that there is more demand and consumers are willing to spend and borrow and everything else. And everything’s fine. It’s only when you begin to make this transition where inflation begins to ripple its way through the economy. More generally, and workers start to demand higher wages. The corporations realize they have a problem demand. Maybe good, isn’t that nice. So we’ve had good earnings last couple of quarters, but now we’re getting very substantial cost input pressures. To the extent we were buying our commodity inputs under longer-term fixed contracts, those contracts are running out. And when we reset those contracts, our input prices may be substantially higher. Also our workers are demanding higher wages as a result, corporate profit margins begin to shrink. And when corporate profit margins begin to shrink, then of course earnings eventually might get a double whammy. They get a double whammy because corporate margins are shrinking, but the initial demand boost of the early inflation has faded. And you fall into stagflation where inflation remains elevated, but demand is cooling. That’s when corporate profits really get slammed. Now I think we’re just not there yet. Give it another couple of quarters. I don’t think it will take that much longer and we’ll start to see material earnings warnings. Not only, not only because demand is cooling. And I think the leading indicators show us that now pretty clearly in the United States and several other large economies, but, there are also going, whether they say it or not. You’re also going to see margins getting hit and when equity analysts or any intelligent investor for that matter, see not only demand coming off, but margin shrinking, we are going to see a major repricing of the equity market. Pes are going to drop in my opinion, into the low double digits before there is a meaningful stabilization of the market. And it’s possible, I wouldn’t rule it out, that we will see high single digits for PE multiples. The same way we did in the early nineties as Volcker was tightening those screws back then, I believe the Dow Jones PE ratio trough at less than eight. And again, I, I know that sounds like doomsday, and yet it could happen again.

Lynette Zang:

You know, I mean doom’s day. I mean, you know, can insanity stay insanity forever. Of

John Butler:

Course not that which can’t go on won’t.

Lynette Zang:

Exactly, exactly. And you know, we’re in an interesting situation because with the breakdown of the supply chain, what I’m been hearing lately is we have to tamper demand in order to have the time to repair the supply chain at the same time that we need demand to stimulate the economy. So look,

John Butler:

If you keep, if you keep throwing money at a supply side problem, you’re only going to make it worse. History is full of examples like that. You just adding fuel to the fire. You’ve got to let the supply side of the economy sort itself out on its own merits. The downside of globalization. And just in time inventories is that when you do get these sorts of shocks, they are potentially very, very damaging. There’s just no margin for error anymore. And what seemed great on the way up doesn’t necessarily seem great on the way down. And God forbid, we get into a proper trade war over the next few years as one country, after another tries to hold on to its market, share through some bizarre combination of tariffs quotas, you know, this, that the other thing,

Lynette Zang:

and devalutations.

New Speaker:

Exactly well there’s that too, of course it could get very, very messy.

John Butler:

The fact is modern corporations as a result of this multi-decade period of globalization and just-in-time inventory management, they are so geared. And so leveraged to that, that disruptions like these are extremely difficult to deal with. The whole management team has never seen it before. They’re too young. They they’ve never suddenly faced a complete shut off of a supply of a key resource. And God forbid, tariffs and quotas starts showing up economist claimed to be able to model this stuff, but they can only do so in kind of general macro terms, the moment you get into the specifics of a modern multi-national where a given widget needs to pass across 50 borders through for different processes before it finally ends up in Walmart or wherever it is to be sold. I mean, my word try coming to terms with that in real time. I mean, good luck. I couldn’t do it, but that’s where we are. So it’s going to take a long time to sort this out. And if the monetary authorities or fiscal authorities for that matter, just keep throwing more and more money at it. Those distortions of price signals will make it even more difficult to rationalize and come to terms with what’s really going on. They should stay out of it.

Lynette Zang:

Oh, it’s probably a little too late to ask them to do that, but just, you know, one final question, which is going back to the gold standard and an ounce of gold, because right now, I mean a lot and silver too. I mean, silver too, for sure. So right now people are looking at the spot markets and they see silver, like somewhere, a little bit north of 24 bucks an ounce, and they see gold at somewhere north of, at the moment maybe 1800 give or take an ounce. Can we trust that? What we’re looking at is the real value where when we go back on the, as you say, inevitable, and I agree with that a hundred bazillion percent, when we do go back to that gold standard, what can we expect? And in nominal terms, because I know, I don’t really think about it like that, but most people do.

John Butler:

Yes. I mean, look, there are ways to approach this. I used to, in my book, many of your viewers maybe familiar with Jim Rikards does so in his book, the first to con yeah, the, the first economist that I know of who directly attacked this problem of estimating the market clearing price of gold in the event that United States and other countries choose to remonetize it, we’re up Murray Rothbard, and Harry Brown back in the seventies, both of them went through the calculation metrics for how to estimate the market clearing gold price in the event. Gold is re monetized. And basically what you do is this, you basically come up with some sort of estimate for to what extent bank deposits would need to be backed by gold to make such a system viable credible. And one simple way to do that is just to say, Hey, let’s go back to the way things worked under Bretton woods, Bretton woods was not a 100% reserve system. It was still a fractionally reserve system. However, it was fractionally reserved in a way that the world, at least for the first couple of decades of Bretton woods consider as credible. So let’s use that as a benchmark. And basically what that means is that you need to have a meaningful portion of the U.S. Money supply backed by U.S. Gold reserves. And then of course you extend that to other countries they’re respected money supplies need to be to some extent backed by, by their gold reserves and so on and under Bretton woods, the round number that was used, there was 40% that is, you’ve got to be able to back 40% of your narrow and I stress narrow money supply with gold reserves. That is M1 actual demand deposits, actual cash in circulation would need to be 40% backed by gold. That said, if you want to re monetize gold today in a way that is not disruptive, you might need to back 40% of M2 which extends into time deposits and certain other forms of money substitutes. And the reason I say that is because those forms of money substitutes that comprise and to today are so central to the fundamental stability of the financial system. That if you don’t allow M2 to be meaningfully backed by gold reserves, it might not be seen as a credible system. It will bring down too many of the banks too much of the financial system will crumble, but you’re, but when you start doing these calculations today, because of the astronomical amounts of M1 and M2, that have been printed not only in the United States, but elsewhere, you, you start, you start to get into mid five figure numbers for a market clearing gold price in dollars, 30,000, 40,000, 50,000. It’s a huge figure. Now that might seem crazy as you’ve already said, the crazy thing is what central bankers have already done, right? In a way this is baked in the cake. If we’re going back to gold, the least disruptive way to do it is to allow the market clearing price of gold, to rise to a level that reestablishes credibility in the financial system. And based on what I just mentioned, that could be a huge number.

Lynette Zang:

So do you have final thoughts on what people you think people should do in order to get prepared for the inevitable going back? Because that’s all about confidence, right? This whole system is floating because the public still has confidence in this little piece of paper or digits in there, on their phone these days. But,

John Butler:

You know, indeed look I used to advise a big institutional and high net worth investors. I still do on the side from time to time. And what I’ve told them in recent years is, you know, you’d never put all your eggs in one basket. I think there’s tremendous outperformance potential for both gold and silver and other real assets for that matter versus both stocks and bonds. If you look at history and you can look at a lot of history here, you always want to have, and I stress always as kind of a sort of base case throughout history, you always want to have a minimum of about 10 to 15% of a liquid investible portfolio in gold and silver, if you want to best diversify it against all the economic environments. So the rest of it, of course, could be comprised of, of stocks and bonds, but 10 to 15% gold silver, but, but that’s in normal times, if you start to adjust that portfolio for a world of zero interest rates where, where bonds are almost guaranteed to lose money over time and where stocks are overvalued by any meaningful historical comparison, you can easily double the portion of gold and silver that you need in that portfolio to make it truly robust to all economic environments, given the amount of debt and leverage present in the system. So I think you can make a conservative case that holding 20 to 30% of your, of your liquid investible assets in gold and silver or gold and silver linked investments, such as producers, streamers you know, various parts of the value add chain there, I think is a perfectly reasonable position to take. And if you do that and you do that while the price of insurance, if you will, is still relatively cheap you might have to wait a while to realize the value of that insurance, but just like when you purchase a home, you don’t wait and play games before you purchase fire insurance before you purchase you know, other forms of insurance to protect your property. You generally purchase the insurance when you purchase the home. The same is true of building a financial portfolio. You purchase the insurance when building the portfolio, not after and gold and silver is the insurance against financial assets, generally underperforming as a result of what I believe is an inevitable de-leveraging restructuring and a large devaluation of currencies in our future. Wow.

Lynette Zang:

We’ve covered so much, but I could talk to you for hours. You’re brilliant. I’m so glad that you came on, but is there anything else that you think that viewers should be aware of before we sign off today?

John Butler:

Well, look, you know, read the history books. There’s no free lunch, mistakes have been made.

Lynette Zang:

Read your book!

John Butler:

Well, if you like. Yes, absolutely. And, and certainly please any anyone who’s interested in getting into golden silver, there are so many ways to do it. Some are more convenient than others. Some are lower costs than others. And I believe that this is a great place to be involved. Hence my own involvement here in London with a thin tech firm, which is trying to build solutions to allow easier access to gold and silver savings accounts as it were that are nevertheless seamlessly linked to the banking system, such that it just removes the friction that is sometimes involved with acquiring gold and silver. So that’s what I’m doing now, and I’m pleased to be doing it because as we just as we shared in our discussion earlier, I liked being part of what I think is the solution, or at least a part of that solution to to these large problems that we sadly are facing at this time.

Lynette Zang:

Well, I’m glad that you’re part of the solution because you’re definitely brilliant. And I’m going to tell people, you know, this book, well, this is your earlier version, the revised version. It’s excellent. It is a must read and you’ll learn so much. Even I guys, I learned stuff from this book. And so, you know, they know I’ve been a student of, I call it the currency life cycles because when I was at Shearson, I started studying currencies in 87. So it was right around that whole globalization time. I remember all the talk about it. This has been fabulous, and I hope to have you on again, and we can deepen our discussion, but for everybody today, you know, listen to this interview more than once. It’s fantastic and, and read the book because John has done a brilliant job of really making it very easy to understand. I think it’s critically important today that everybody does pay attention to this and do something to protect their purchasing power, their wealth, their future their children’s future and so on. Well, I’d like to thank you all for joining us today. And until next time please be safe out there. Bye-Bye.

Follow John Butler ⬇️

Twitter: https://twitter.com/ButlerGoldRevo

LinkedIn: https://www.linkedin.com/in/john-butler-8562678/