THE 5 DOOM LOOPS OF A CRISIS: What You Need to Know. By Lynette Zang

When we talk about patterns, no discussion would be complete without examining the pattern of a “Doom Loopâ€. In fact, there are five key “Doom Loops†seen during financial crisis’s: The Intermediary, Sovereign, Collateral, Hedging and ultimately, the Real Economy Doom Loop.

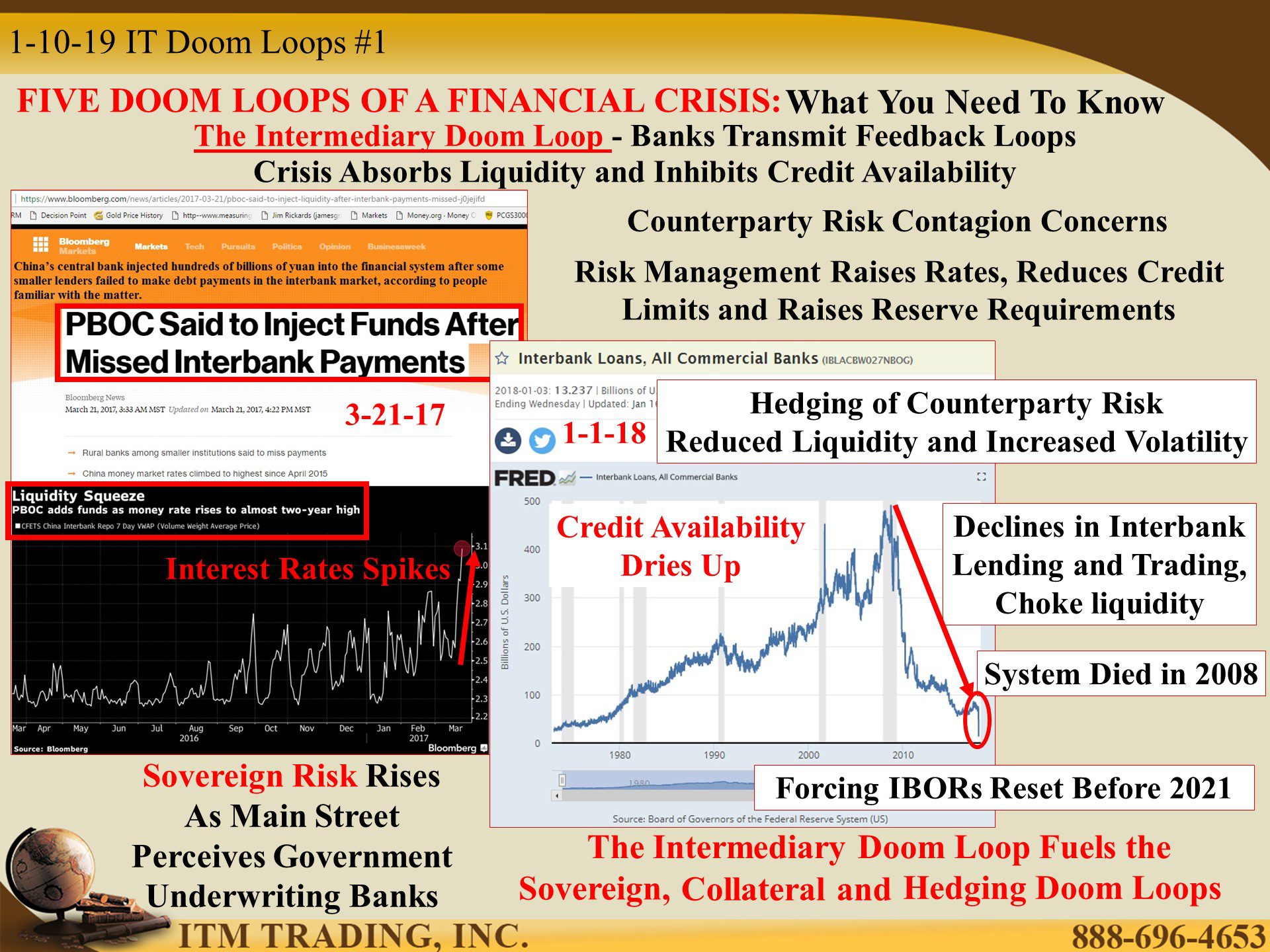

Arguably the king pin of doom loops would be the Intermediary Doom Loop because it occurs inside commercial banks that issue the debt that greases the wheels of economic activity for private corporations and individuals. Banks transmit feedback loops as the crisis absorbs liquidity and inhibit credit availability.

When a financial crisis occurs, liquidity dries up as banks fear contagion to other banks they may have contracts with. Rates and reserve requirements rise, essentially cutting off credit to junk rates creditors, who need credit the most. The outcome is a rise in defaults, which puts further stress on the banking systems liquidity and availability of credit.

Government intervention and support may be interpreted as government underwriting banks and therefore undermines public confidence in governments and central bankers. This in turn could impact public confidence in markets and currencies.

It is this loss of confidence that ushers in first hyperinflation, then the financial system reset that most likely lies in our future.

The Intermediary doom loop fuels the Sovereign, Collateral and Hedging doom loops.

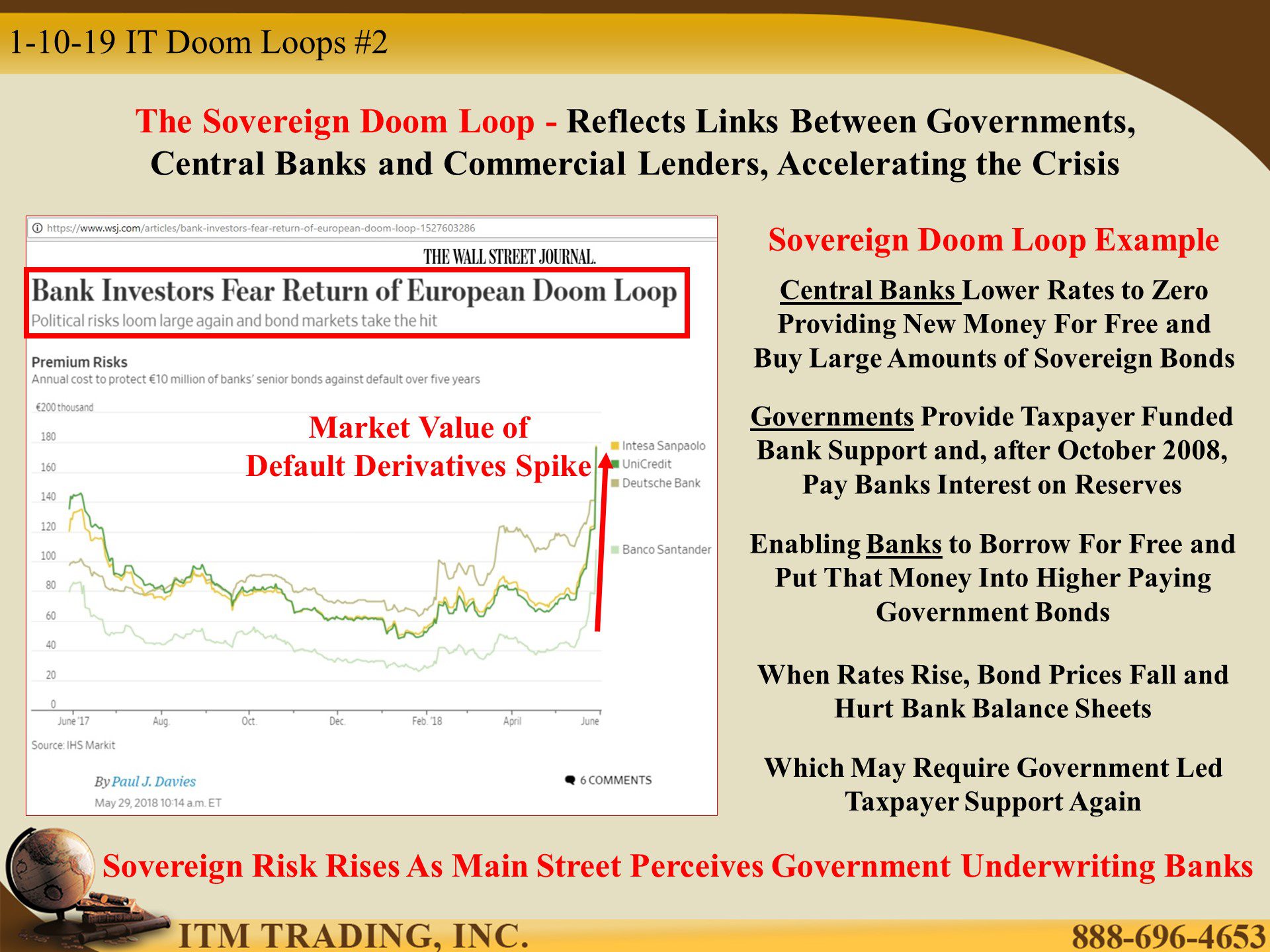

The Sovereign Doom Loop reflects the links between governments, central banks and commercial banks. Looking back to the 2008 crisis, central banks pushed interest rates near zero to inspire borrowing and spending, at the same time governments authorized a taxpayer funded bail-out of the banks.

As one example, QE (Quantitative Easing) provided trillions in new free money for banks, who bought government bonds that paid interest above the banks cost of debt. Essentially risk-free income. But as interest rates have crept higher, the market value of those government bonds declined. This has an impact on bank balance sheets, reserve requirements and possibly, the ability of that bank to borrow. This loss could push a systemically important bank near default, which would then require government led taxpayer support again.

Which leads us to the Collateral Doom Loop. Much of this “collateral†are intangible contracts controlled by algorithms, which creates price herding. Great on the way up, but nasty on the way down. As prices for stocks, bonds, real estate and derivatives decline, margin calls are triggered. If you get a margin call you would need to come up with cash to cover the call or you would be forced to sell assets to meet the margin call.

Enough asset sales will push prices down further, generating additional margin calls, which would then absorb more cash or require additional asset sales…

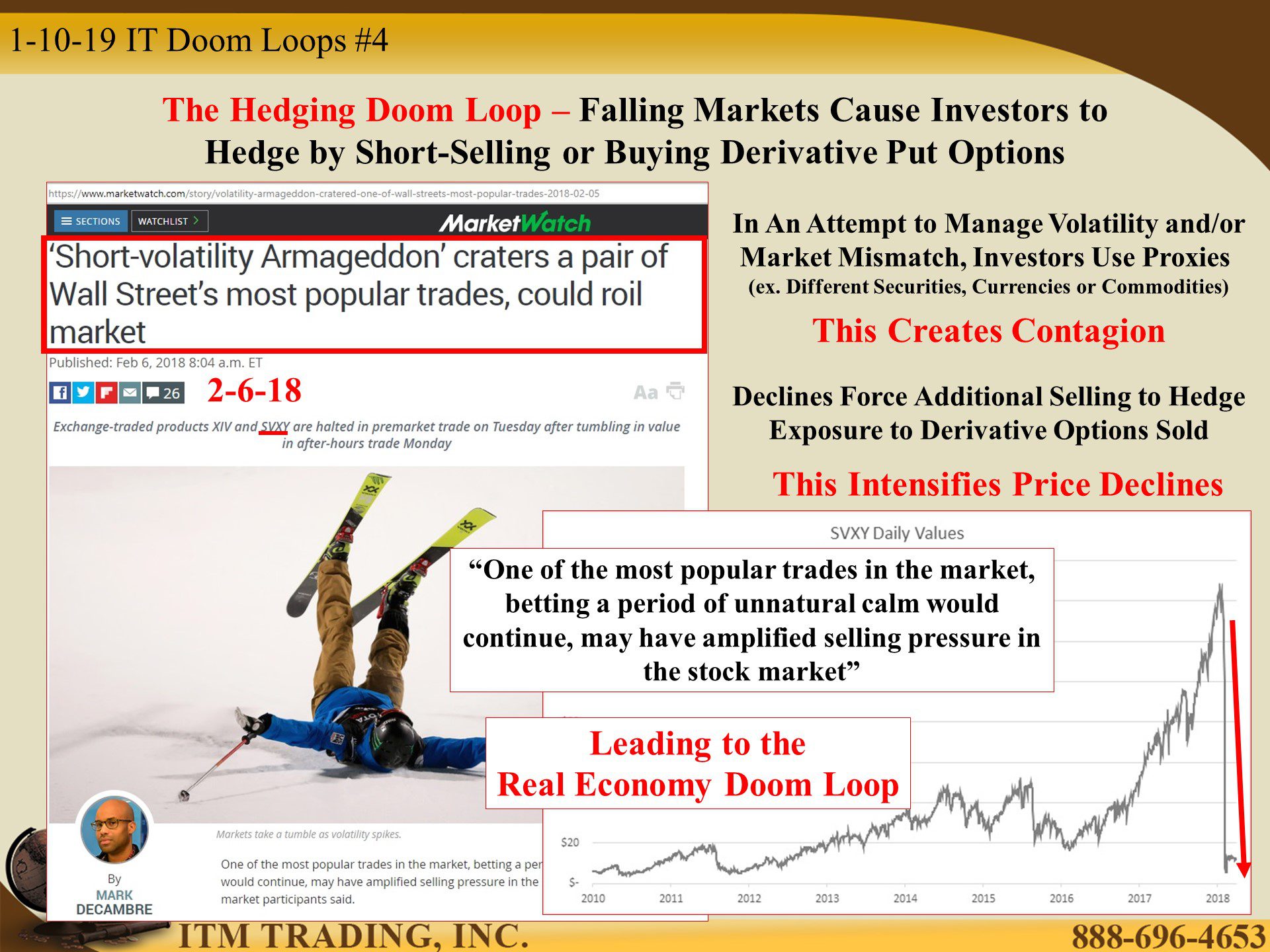

Professional traders like derivatives to hedge market positions, which brings us to the Hedging Doom Loop. This is very precarious because it involves short selling (selling something you do not own, with the hopes you can buy it back later at a lower price) or buying derivative put options (a Put is the right to sell at a specific price by a specific date).

These tools use leverage to create the more shares of stock, REITS, bonds and/or derivatives than there is. This amplifies and intensifies price moves, particularly on the way down.

All of this leads to the Real Economy Doom Loop, which is based upon the ability to constantly compound debt, which in turn takes us back to bank credit availability and especially consumer confidence, which is what drives consumer spending (70% of GDP).

In any Ponzi scheme, confidence is key. What governments, central banks and Wall Street are really afraid of is that public loss of confidence in the financial system. Without that they won’t shop or hold their wealth in Wall Street contracts. They won’t believe in the “stimulus†provided by governments and central bankers. They might even buy physical gold and silver!

If that happened, how would wealth be voluntarily transferred?

So you can see the patterns in doom loops, but there are also clear patterns in real money gold and silver. This lies in our future, though the time to get into position is now.

Slides and Links:

https://www.wsj.com/articles/bank-investors-fear-return-of-European-doom-loop-1527603286

https://www.bloomberg.com/opinion/articles/2019-01-01/five-doom-loops-investors-may-confront-in-2019

https://www.bloomberg.com/opinion/articles/2019-01-01/five-doom-loops-investors-may-confront-in-2019

https://houndstoothcapital.com/2018/05/06/anatomy_of_a_blowup/

https://fred.stlouisfed.org/series/GOLDAMGBD228NLBM

https://www.goldbroker.com/charts/gold-price/vef

YouTube Short Description:

When we talk about patterns, no discussion would be complete without examining the pattern of a “Doom Loopâ€. In fact, there are five key “Doom Loops†seen during financial crisis’s: The Intermediary, Sovereign, Collateral, Hedging and ultimately, the Real Economy Doom Loop.

In any Ponzi scheme, confidence is key. What governments, central banks and Wall Street are really afraid of is that public loss of confidence in the financial system. Without that they won’t shop or hold their wealth in Wall Street contracts. They won’t believe in the “stimulus†provided by governments and central bankers. They might even buy physical gold and silver!

If that happened, how would wealth be voluntarily transferred?

So you can see the patterns in doom loops, but there are also clear patterns in real money gold and silver. This lies in our future, though the time to get into position is now.